Investors are living through an unfortunate piece of market history this year: the worst bear market for US bonds in at least 28 years, if not ever.

The culprits are the usual suspects when bond prices decline. It’s the surge in inflation and the Federal Reserve’s moves to raise interest rates that are to blame. The central bank will be front and centre this week when its policy-setting Federal Open Market Committee meets for the first time since it raised rates in March. The Fed is expected to raise interest rates by another half a percent Wednesday, which would be the first rate hike of that magnitude in 22 years.

While the factors underlying the bond market rout aren't unusual, it is the speed and extent of the losses and the accompanying jump in yields that are unique to the postpandemic economic recovery. That, coupled with the inflationary ripples from Russia’s attack on Ukraine.

Many experts had expected a rough year for the market, but the kind of moves seen in 2022 has left veteran investors reaching for superlatives.

“It’s historic,” says Jurrien Timmer, director of global macro at Fidelity Investments.

“It’s been a real and significant and painful move,” says Steve Lear, US chief investment officer for global fixed income at J.P. Morgan Asset Management.

“For those who haven’t experienced a (bond) bear market, this is what it feels like.”

How much longer will the bond selloff last? It depends on the course followed by those same two factors – the Fed and inflation.

In particular, much is riding on whether inflation falls back by enough of a margin in the next year that the Fed doesn’t have to raise rates even further than is currently expected. Any surprises on inflation – positive or negative – will determine whether the worst is over. But with a high level of uncertainty about inflation, there’s a good chance the bond market will remain volatile.

Just How Bad For Bonds?

For now, investors are seeing a pretty deep shade of red on their bond investments.

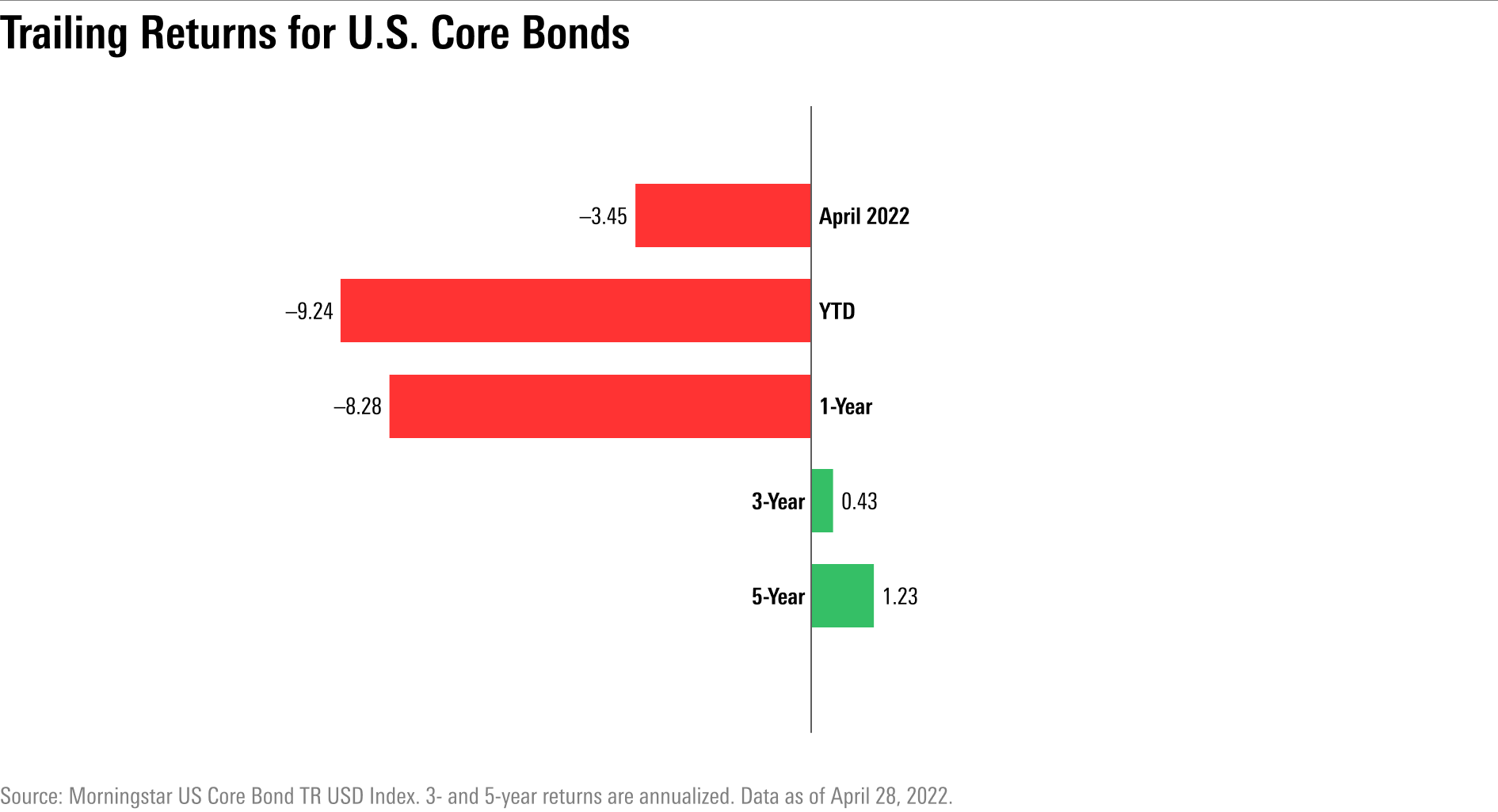

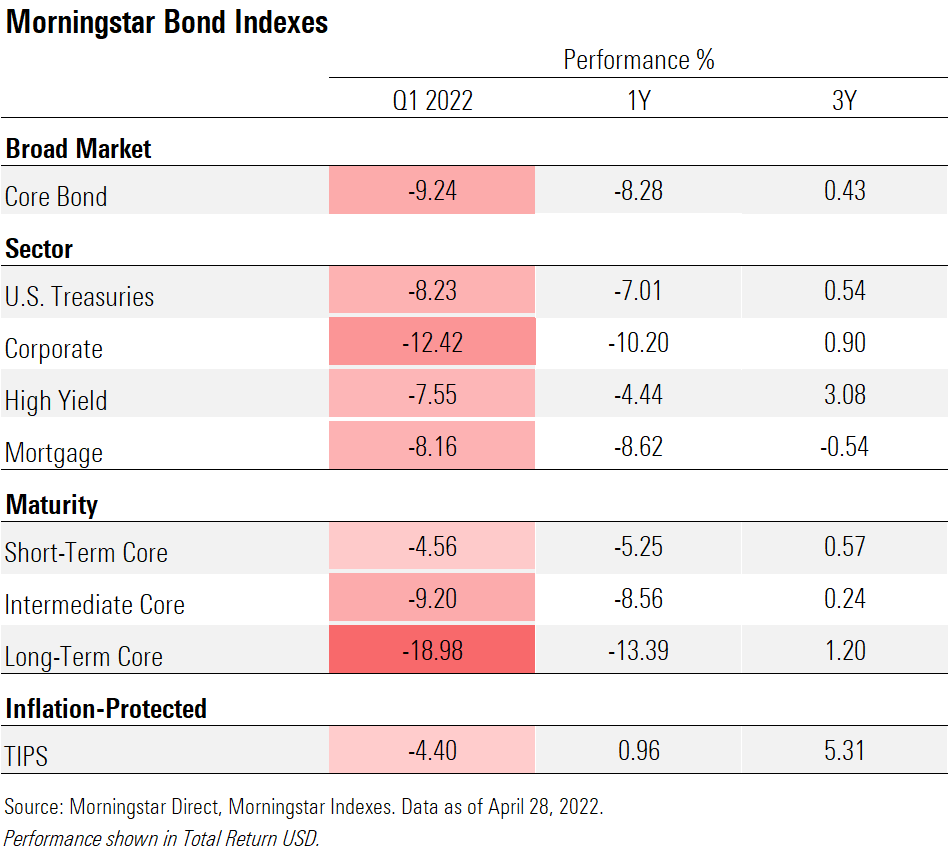

Using the Morningstar US Core Bond Index, which tracks US government bonds and investment-grade corporate debt, April’s losses have made a bad start to the year even worse. A year-to-date loss of 9.2% is by far a bigger decline than the index has suffered for any full year in its 22-year history. The second-largest decline in the Morningstar index came in 2013, at just under 2%.

Longer-term bonds, which are more sensitive to a change in interest rates, have seen the worst of the losses. But even for short-term bonds with declines of 4.6% for 2022 and 5.3% for the past 12 months, those are meaningful losses. Corporate bonds, which tend to be less sensitive to changes in rates, are feeling the pinch from the bond market’s selloff and the decline in stocks.

Another way to look at the extent of 2022’s move in the bond market is to see the changes in yields. Before this year, bond market veterans would point to 1994 as the high water mark for volatility. That year, the Fed surprised investors with a rate hike in February and went on to raise rates six more times, including three half-point funds rate increases and one 0.75-percentage-point increase.

So far in 2022, the yield on the US Treasury 10-year note has risen 1.2 percentage points. That is still shy of the change posted in 1994, when the yield on the 10-year note rose 1.92% over the course of the entire year. However, since 1992, in years where the 10-year note yield rose, the average increase was 0.74%.

Meanwhile, the yield on the two-year note has risen 1.85 percentage points in 2022. That is well below the full-year increase for 1994 of 3.39%, but above the average increase of 0.85 percentage points in those years when rates rose.

Hard Landing

To understand the speed and extent of the current situation requires stepping back into the mindset in the bond market as 2021 drew to a close.

“Six months ago the narrative was that inflation was transitory,” says J.P. Morgan’s Lear. “That narrative has left the market. People no longer believe inflation is going to come down quickly.”

It isn’t just that inflation is running hot at north of 8% on an annual basis, the highest pace in 40 years. It’s not just that the unemployment rate is extremely low.

It’s that the surge in inflation and economic growth came after the Fed had put in place exceptionally low interest rates to support the economy during the recession. The federal-funds rate was at zero and the central bank had purchased more than $4 trillion worth of bonds, keeping market yields artificially low.

As a result, there was a significant mismatch between Fed policy and the economy as 2022 got underway, says Ashish Shah, chief investment officer for public investments at Goldman Sachs Asset Management.

“Part of the problem here is that the starting point for short-term rates, and the size of the balance sheet is completely inconsistent with where the unemployment rate is,” Shah says. “We are past full employment, the economy is growing faster than its potential.”

While the Fed can never be 100% certain of its course for raising rates, “they have come to the conclusion that they are really far from where they need to be,” he says.

And as the calendar rolled into April, the gap between where the Fed was and where it should have been has continued to grow thanks to stubbornly high inflation, strong economic growth, and ripples from Russia’s attack on Ukraine that led to a surge in energy and other commodity prices.

Stephen Bartolini, lead portfolio manager on T Rowe Price’s US Core Bond strategy, notes markets have gone from expecting three rate hikes of a quarter point each for this year to expecting a total of 10 rate hikes.

“If you think back to the last cycle, the Fed only pulled off seven rate hikes and that was over a two-and-a-half-year period,” says Bartolini who runs the $18 billion T. Rowe Price New Income Fund (PRCIX). For the bond market, “it’s the shock of going from zero rates to 3%” that is the problem.

The most recent down-leg in the bond market came after Fed chair Jerome Powell signalled that a half-point increase was in the cards for this week's policy meeting.

"The Fed is going to go big and go fast," says Fidelity's Timmer, who now expects a half-point increase in May, followed by a number of half-point increases and potentially even a 0.75-percentage-point increase.

In recent days, expectations have jumped for a three-quarters-of-a-point rate hike in June, which would be the first since 1994. "The Fed has to put the genie back in the bottle," Timmer says.

From Here

Still, given how far from expectations the bond market’s performance has been this year, it’s understandable for investors to be wary. A significant part of the shock has been that inflation not only moved higher, but faster and well outside the band where it had been.

“The reality is we had stable inflation at 1.5% or so for most of a decade,” says Lear.

“There was good reason why people didn’t think these numbers would change. We had gotten to a point where economic volatility was low, inflation was low, and hence market volatility was low.”

From here, Lear says he will be keeping a close watch on components within the Consumer Price Index report, particularly inflation for core goods, which captures prices on items such as cars, televisions, and furniture. Before the pandemic, it had essentially been zero for 20 years.

“Core goods inflation has gone from zero to 12%,” Lear says. That jump alone has added 2.5 percentage points to the inflation rate.

“Inflation is not staying at 8%, but the question is when will we get back to some sort of equilibrium on inflation, in 2023 or 2024, and what is that equilibrium rate of inflation? If we get back to 1.5%, then bonds are a buy, but if we only settle in at 3.5%, then the Fed isn’t stopping at 3.25% on the funds rate and they have to go to 4% or more.”

That would also mean there are more declines ahead when it comes to bond prices. The big picture is that with this kind of uncertainty around the inflation outlook, volatility is likely to remain high in the bond market.

“People need to get back to factoring in a margin of safety into their investment,” Lear says.