As the Year of the Tiger begins, China looms larger than ever on the world stage and in investors’ portfolios. The country’s economy has grown to become the second-largest on the globe, and its influence has expanded beyond its borders. But decades of rapid economic expansion haven’t translated to commensurate gains for investors.

The Chinese stock market has evolved. In recent years, it has opened up to the outside world. The inclusion of mainland-listed China A-shares in major index providers’ mainline indices is perhaps the most prominent example of the opening of the Chinese capital market.

The Chinese stock market has also become more dynamic. Some of the world’s largest technology companies, like Tencent (00700) and Alibaba (BABA), call China home. And in 2019, the Shanghai Stock Exchange STAR Market was established as China’s equivalent to the Nasdaq: a hub for China’s most innovative firms to raise equity capital.

But as much has changed in China, much remains the same. The Chinese government continues to exert control over economic activity, as evidenced by its recent efforts to pull the plug on for-profit private tutors. The country’s reliance on debt to fuel its growth was again in focus as property developer Evergrande Group edged toward a potential default. So, while opportunities abound, so do risks – big ones.

As such, investors should be choosy when investing there. They may simply decide the risks aren’t worth it, or that being more selective – investing in a narrower slice of the market or partnering with an active manager – is best.

Where’s the Growth?

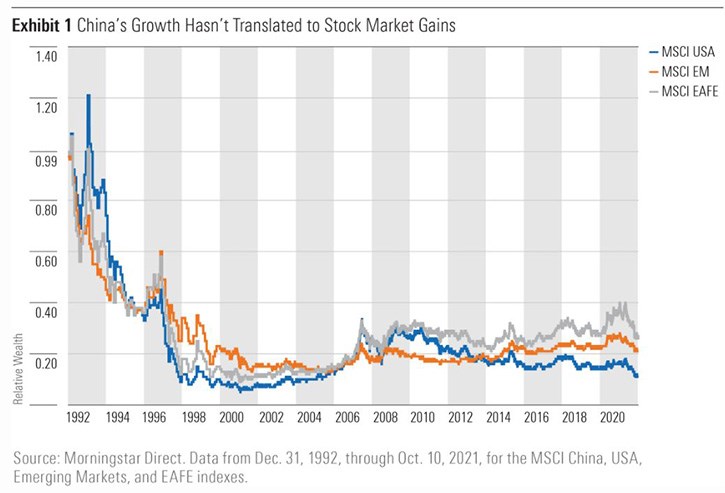

From 1993 through 2020, China’s gross domestic product grew by more than 9% per year. Surely that sort of growth translated to fabulous returns for investors in Chinese stocks, right? Wrong.

Over that same span, the MSCI China Index gained just 2.71% on an annualised basis. Chinese stocks’ returns were equally or even more disappointing relative to other major markets. During this 27-year period, the MSCI USA Index compounded at 10.37% annually, the MSCI Emerging Markets Index 7.95%, and the MSCI EAFE Index 6.65%. Exhibit 1 plots the relative performance of the MSCI China Index to each of these three, and it’s not pretty.

What Do You Mean by China?

It has long been known that the link between economic growth and stock market returns is weak at best and may even be negative. There are a variety of explanations for this. The strongest, in my opinion, is that beginning-of-period valuations are the most meaningful predictor of future returns. But there are other, more fundamental forces at play, too.

One that is particularly relevant to the case of China, cited by finance professor Jay Ritter, is that “a country can grow rapidly by applying more capital and labor without the owners of capital earning higher returns”. Many investors in Chinese stocks can probably relate.

Investing in Chinese stocks is complicated. There are A-shares, B-shares, H-shares, Red-Chips, P-Chips, and some US-listed ADRs, all of which may be members of a litany of different benchmarks. Defining the Chinese stock market isn’t easy, and depending on how you define it, you might come to very different conclusions about its prospects.

Some ETFs track the CSI 300 Index, which consists of China A-shares and is a market-cap weighted index combining the top stocks from the Shanghai Stock Exchange and the Shenzhen Stock Exchange. On the other hand, the S&P China BMI Index invests in the entire alphabet soup of Chinese share classes.

Of the handful of pure China equity ETFs available to UK investors with a Morningstar Analyst Rating, Xtrackers MSCI China has the highest rating of Bronze. MSCI China targets large and mid-cap stocks, and the index has 789 constituents at time of writing, including China A shares, H shares, B shares, Red chips, P chips and American Depository Receipts (ADRs).

Another ETF from the same company tracks the FTSE China A50 and that is rated Neutral. The FTSE China A50 index draws 50 stocks from the Shanghai and Shenzhen exchanges, and only includes A-shares and not B-shares. And the iShares China Large Cap ETF also tracks the FTSE China 50 as its benchmark.

Looking at the performance figures for 2021 in isolation, returns have a tight range between -19.80% and -22.20%. It's useful to compare these figures with the best-rated active fund under Morningstar coverage, FSSA Greater China Growth, which has a Gold Analyst Rating for the B share class. This fund posted 4.7% gains for 2021, behind the S&P 500 of course, but way ahead of the exchange traded funds, which must follow their respective index as closely as possible. But in 2020, a year of exceptional gains for China index and active funds, FSSA Greater China produced a return close to the benchmark of 27.1%.

Is That It?

Have you ever seen the Mona Lisa in person? Do you remember the anticipation as you walked down that long, cavernous hallway in the Louvre? Then, you turn the corner. Was your first reaction like mine? I remember saying to myself, “is that it?”.

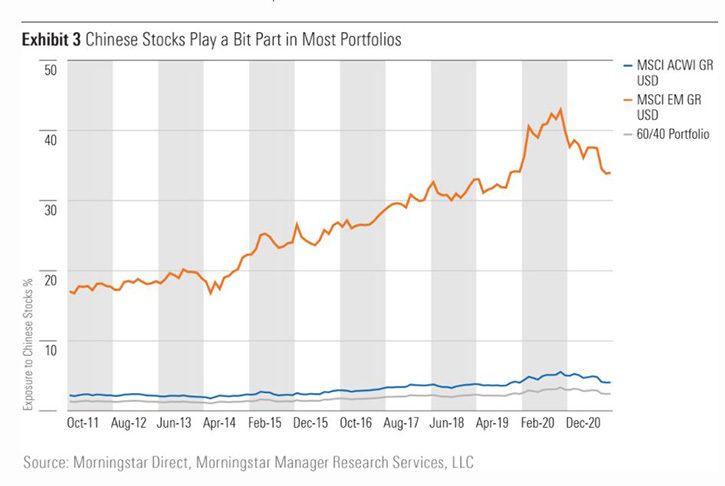

My first impression of what is arguably the most famous painting in the world was that it was much smaller than I’d expected. Similarly, while China looms large in our minds, its footprint in most investors’ portfolios is still fairly small despite its growth.

Exhibit 3 puts the size of the Chinese stock market into perspective. Chinese stocks have grown to represent a larger portion of global markets over the past decade. In October 2011, they made up just over 17% of the MSCI Emerging Markets Index. At the end of September 2021, that figure had grown to nearly 34%. Chinese stocks’ share of the MSCI All Country World Index grew to 4.1% from 2.2% over this same time frame. Their share of a market-cap-weighted 60/40 stock/bond portfolio expanded to 2.4% from 1.3%. So, in the context of a diversified portfolio, stocks that call the world’s second-largest economy home still play a small part. This will be important to remember the next time mainland markets melt down like they did after Chinese retail investors ran for the exits in 2015.

Fish in a Barrel

Fettered access, government interference, and an investor base skewed heavily toward retail traders make the Chinese stock market a target-rich environment for savvy investors. It may well be the only major market where a majority of professional investors regularly beat their benchmarks. In the latest Morningstar China Active/Passive Barometer, my Shenzhen-based manager research colleagues found that three quarters of actively managed diversified Chinese stock funds available to Chinese investors managed to both survive and outperform their average passive peer over the prior decade. Just 19% of actively managed US stock funds can claim the same over the 10 years through June 2021. Clearly, there are ample opportunities for active managers to add value in China.

.jpg)