As as end of year special, we asked our Twitter followers to choose a stock of the year based on the biggest themes of 2021, which included crypto mania, meme stocks and billionaire space travel. The energy crunch, however, came out on top, with British Gas owner Centrica (CNA) as the favoured stock for this theme.

Apart from coronavirus, soaring energy bills are one of Britons’ biggest preoccupations going into 2021. And they are inextricably linked with another big theme of 2022, inflation, as gas and electricity prices are driving up the cost of living. CPI inflation moved above 5% in November, and the Bank of England expects this to peak at 6% in April. “The further rise in inflation next spring is in large part expected to reflect current developments in wholesale gas and electricity futures prices,” wrote Governor Andrew Bailey, in his letter to the Chancellor explaining why inflation is above the 2% target. Futures are traded instruments that utilities buy and sell depending on where they expect prices to be in the month and the quarter ahead, while spot prices reflect current demand levels, such as during a cold snap.

This is a crisis with a political element too. As much of Europe is not self-sufficient in natural gas, we depend on Russian supplies to meet energy demand. Currently Germany and Russia are locked in talks aimed at resolving this supply crunch, but the sticking point is Russia’s plans for Ukraine.

Price Cap Drama

Whether inflation falls from that 6% peak is hard to predict, but in the same month energy regulator Ofgem is lifting its cap on annual energy prices. Currently set at £1,277, meaning that many customers will not pay more than this amount, it’s being revised upwards in April. Some industry experts are predicting the cap could be lifted to £2,000 (that’s £166 a month, roughly 10% of the average take-home pay), or even as much as £3,000.

Why was the cap introduced in the first place? After many years of lobbying by consumer groups, the Theresa May Government took action in 2017, giving the regulator the green light to impose a price cap on standard variable rate tariffs from the end of 2018 to 2020, when it was extended. Lobbyists argued that for too long UK energy providers have been overcharging customers, especially the poor and vulnerable. But the providers themselves had countered that they are at the mercy of wholesale markets and geopolitical supply shocks, and must pass on these costs to survive as a business.

The price cap was implemented after a period when British consumers had more choice of provider than ever, with disruptors such as Ovo Energy hoovering up disenchanted customers from the likes of British Gas and EDF energy, encouraged by switching websites. For a brief period, UK ministers could argue that we had a reasonably efficient market for energy provision, with the caveat that Britain can’t ultimately control the price of gas or electricity because we have to import a great deal of both. Now, soaring gas prices have forced some of these competitors out of the market, with Bulb Energy being the latest to fall into administration.

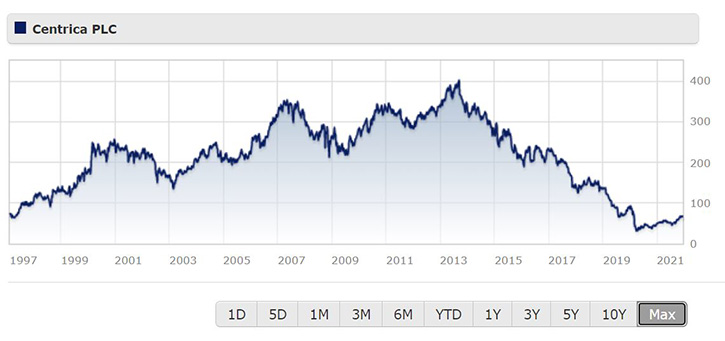

Fat Cat Row

As owner of former monopoly British Gas, Centrica was once the lightning rod for criticism of “greedy” energy companies, especially with generous pay packages for executives thrown into the mix. The political heat has eased off in recent years, but from an investor’s point of view, Centrica has been seriously underwhelming. Shares hit 400p in 2013 but are now below 70p. Still, there has been a strong bounce in the price this year, driven by a rebound from autumn onwards, and the shares are now nearly 50% higher than at the start of the year. Morningstar analyst Tancrede Fulop thinks the shares are close to being fairly valued even taking in the late 2021 surge. Despite soaring gas prices and Centrica’s dominant position in the UK residential energy market, the industry price cap means that profits will remain under pressure for the foreseeable future. And stiff competition and low barriers to entry deprive the company of an economic moat.

“Historically, Centrica was able to deliver higher margins than its competitors thanks to the large scale provided by its leadership position. Therefore, we thought the British Gas brand name and established position provided some economic moat. However, in the current political climate, we believe the value of this moat has materially diminished.” Fulop argues that the price cap could become a permanent fixture of the UK energy market. “The tariff will be revised twice a year and is set to be removed in 2023, but we think it will never be removed, implying a reregulation of a sector that was liberalised in the 1990s,” Fulop says. Centrica used to be a solid dividend stock, but scrapped payouts in last year’s chaos. But, as our latest monthly dividend round-up explains, many FTSE companies will continue to restore payouts in 2022 after an encouraging trend in 2021.