As this week has been about all things income at Morningstar.co.uk, we gave our Twitter followers the choice of four dividend paying stocks that have had a strong share price run in 2021.

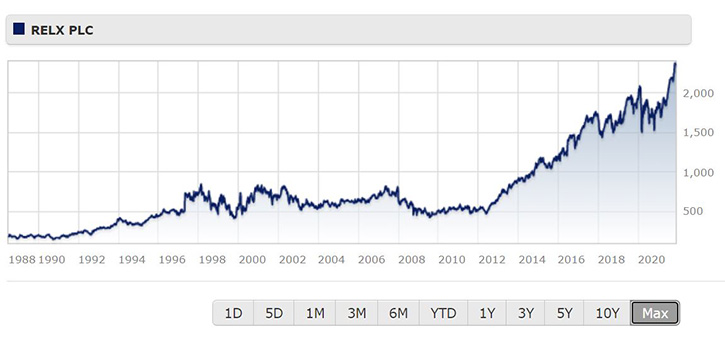

Of those posting gains of 20% or more, information and data company RELX (REL) has come out ahead of Johnson Matthey, CRH and Reckitt Benckiser. All of these shares are on our monthly list of top-yielding FTSE 100 dividends, but RELX is rooted at the bottom of that table because its yield is 2%, compared to around 9% for the Imperial Brands and British American Tobacco. This is no surprise as a rising share price pushes down the yield – RELX’s share price is up 25% this year and nearly 33% since late November 2020, and the yield is around 2%.

RELX (pronounced Rel-ex rather than R-E-L-X) changed its name from the more traditional sounding Reed Elsevier in 2015 and embraced the digital data revolution. Reed Elsevier itself was a merger of the UK’s Reed and Dutch scientific publisher (an Anglo-Dutch divorce is currently going ahead at Royal Dutch Shell). Traditional textbooks and directories are still being printed, but the share of electronic formats produced by the company has gone from 30% to 90% in 10 years.

Clients include companies, governments, and universities, with recurring subscriptions the main payment model. “The vast majority of RELX’s revenue derives from the provision of data and analytics to corporate clients globally. Over a period of many years, RELX has developed sophisticated databases and decision-making tools that many industries and professions now heavily rely on in order to carry out their daily activities,” says Morningstar analyst Michael Field.

RELX is listed in London, Amsterdam and New York, and has four main divisions: scientific, technical, medical (nearly 40% of sales); risk and business analystics; legal; and exhibitions, which makes up 5% of revenue. A quick glance at the profile of share price chart suggests this company is not an ex-growth income journeyman. With online data the new valuable resource for companies, this sort of high growth comes at a steep price, and RELX shares are currently rated a 1 star by Morningstar analysts. Shares currently trade at £23.50 but they have a fair value of £16.50, according to analyst Michael Field. After the latest third-quarter results--which he described as solid--he reiterated the fair value estimate of £16.50, saying “the shares represent little value currently, sitting more than 20% above their pre-pandemic levels”.

Looking in detail at the latest Q3 results, the risk and business division has shown the highest growth, with revenues up 10% on the same period of last year. The company’s exhibition business was affected by lockdown last year, like many others in this field, but the re-opening of the global economy this year has helped provide some relief to RELX, says Field. The turnaround in the exhibitions arm may take longer than expected to get back to close to 2019 levels, Field adds. On the plus side, larger companies in this space will benefit from reduced competition in the coming years. “With a slimmed down cost base, and many competitors having fallen by the wayside, we believe the division will be in good shape going forward,” he says.

RELX has a narrow economic moat because of the strength of its brand and reputation, as well as the cost factor of a company/university switching to a rival data provider. Field says that three out of four of RELX’s divisions are worthy of a moat, apart from exhibitions, which, pandemic aside, is more vulnerable to cyclical swings in the global economy. In a downturn, for example, companies tend to cut spending on advertising and events.