As we enter the last quarter of 2021, let's take a quick look back at key events of the last three months.

Looking at stock market charts, July, August and September appeared largely uneventful for global equities, but there were plenty of individual stories to keep investors awake at night. Inflation remains a central concern across the globe, with natural gas prices soaring in Europe and crude prices rising as Opec holds firm on increasing supply. There is widespread anxiety about shortages, whether of goods or manpower, and rising prices.

The US has been preoccupied with the tough business of government, with the debt ceiling once again raising its ugly head. (My colleague Tom Lauricella has covered the issue in detail). The Morningstar US Market Index climbed higher in July and August on optimism about the US economic recovery. However, shares fell back from their highs amid Covid variant worries, supply chain slowdowns, and worries about China.

"It was a round trip for US stock investors in the third quarter of 2021, with the broad market posting 19 new highs before falling back to end up where it had been three months earlier. Still, major stock markets around the globe are still up strongly over the past year, a contrast to some corners of the bond market where investors are facing losses," says my colleague Katherine Lynch in her round-up of the quarter.

In emerging markets, the China Evergrande story blew up in September and the story is still playing out. There are concerns over contagion to developed markets too, although so far the market volatility has been shortlived. In the UK, there has been plenty to talk about too.

UK Economy - There's a Lot Going On

As we can see from the growth chart for the year to date, the Morningstar UK Index has grown 13.45% so far this year, but only 0.85% from July to the end of September.

While equities have not been very dramatic in this period, there's been a lot of economic news to contend with. The quarter started with the easing of the last coronavirus restrictions and ended with petrol panic. So there's plenty to preoccupy households and policymakers, including: tax rises, the end of the stamp duty holiday, labour shortages, soaring inflation and the timing of Bank of England interest rate rises. Covid cases are still high by some measures, and there are concerns over winter restrictions that could stall the economic recovery.

Ben Yearsley, investment director at Shore Financial Planning, thinks that the UK economy is at a pivotal moment and that the third quarter has not matched the spike in activity seen in Q2 when lockdown lifted. Q3 GDP figures, due in the next few weeks, will shed more light on the UK's climb out of the pandemic slump and whether it can be sustained.

“The ending of the furlough scheme is a big moment for the UK economy as recent labour shortages have been contributing to higher inflation – will the 1 million or so people being furloughed be able to return to work or are those jobs now unviable? There have been more jobs advertised recently than people to fill them so the next few months will be crucial.”

China Unsettles Global Investors Again

The potential collapse of Evergrande could have significant repercussions beyond China’s border. Chinese stocks account for 35% of the Morningstar Emerging Markets Index, and the benchmark tumbled 7.6% in the quarter. In contrast, developed markets fell 0.26%.

Evergrande’s stock price fell by 70.85% over the quarter: from HKD 10.12 on July 1 to HKD 2.95 September 30. However, trading was halted on the Hong Kong stock exchange on Monday October 4 pending a “major transaction”, the developer said in a stock exchange filing. For more on the Evergrande crisis, see our explainer.

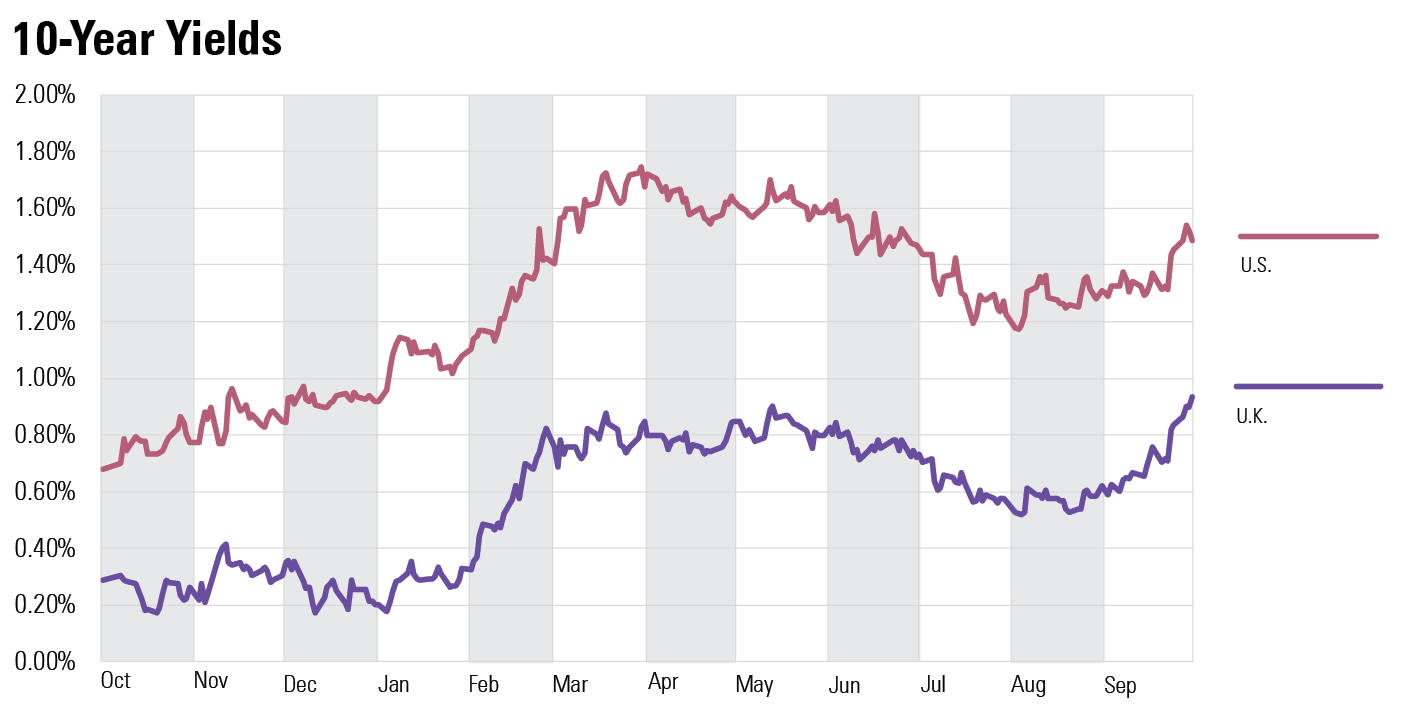

Rising Bond Yields

On the bond side, fears over rate increases amid rising inflation have sent bond yields rising in the US and UK. The fixed-income market now has slightly better visibility over the timing of the Bank of England's interest rate rises; the Bank expects inflation to hit 4% by the end of the year, double its target, and continue at this level into 2022. This rise in yields has hit bond prices, and the gilt sector has been at the bottom of the performance table all year.

Noelle Cazalis, co-manager on the Rathbone Strategic Bond Fund, says Q4 could bring a correction in yields, especially as the first US interest rate rise is some time away, expected between September and November 2022.

“The additional yield of the corporate bonds over government debt is attractive, so for now it is more about fine tuning credit selection than cutting risk significantly,” she says.

So where are we headed? Laith Khalaf, head of investment analysis at AJ Bell, thinks the winter will bring more clarity: “Inflation will remain elevated and that will begin to test the nerve of central banks. November looks like a crunch month, where central bank meetings on both sides of the Atlantic could fire the starting gun for the tightening cycle. Some expectation of tighter monetary policy has already been baked into prices, with both bond yields rising, and the valuations of some growth stocks getting clipped back from lofty levels.”