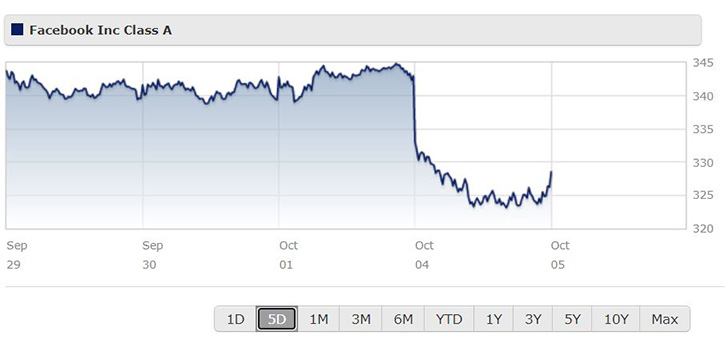

Facebook (FB) shares crashed on Monday after an outage that took down the main social media platform as well as WhatsApp and Instagram. The company is also under pressure after a whistleblower has made allegations about Facebook’s approach to such issues as hate speech and how young people are affected by social media.

But we are maintaining our $407 Facebook fair value estimate and the wide-moat firm is now trading in 4-star territory after yesterday’s decline. The stock has been hit by many negative headlines regarding the firm’s policies, in addition to its main properties not working for a few hours.

While the stock will likely remain under pressure from negative news (the outage impact will likely be negligible), we think Facebook’s network effect remains intact. We remain confident that while the firm’s user growth, engagement, and monetization may weaken somewhat, with nearly 3 billion monthly active users worldwide, a reversal of its platforms’ flywheel effect remains unlikely. In addition, while some large brands may abandon Facebook, we believe small and midsize businesses will continue to find Facebook’s properties one of the most efficient ways to reach consumers.

Experienced in Controversy

We think the firm will continue to face pressure to more closely manage accounts and user-created content, and generate immediate remedies and long-term solutions for some of the issues that have grabbed headlines since The Wall Street Journal began publishing its reports in mid September. While the past is not indicative of the future, we note the firm has faced similar issues previously with a negligible long-term impact on user growth, advertiser demand, and overall financial performance.

In our view, Instagram’s impact on younger girls will likely have the most enduring effect on the firm. Platforms like Instagram, TikTok, and Snap clearly want to increase engagement, which is driven by content that stirs emotions whether positively or negatively. As such, we wouldn’t be surprised to see more control over usage enforced by the firm, parents, lawmakers, or all the above. This would likely reduce user growth and engagement, making the Instagram audience less attractive to advertisers.

However, this could also be partially offset as some large brands may begin toview Instagram and Facebook as safer. We expect the firm to try to address these issues more directly and effectively through the media. Simply highlighting the various steps it plans to take based on itsown interpretation of its internal research to reduce the negative impact of its platforms’ content and how it iscurated would help combat the increase in negative perception around Facebook and Instagram. The firm could further contribute to groups that support mental health, seek to improve public discourse, or remedy other issues critics have raised. In short, we expect Facebook to implement real reforms that improve its platform, even if that results in modest financial losses, while undertaking a public relations campaign to improve its image.

Counting the Cost

We estimate that with the apps being down for approximately seven hours, Facebook may have lost between $110 million and $120 million in advertising revenue, less than 0.10% of our 2021 total revenue estimate for the firm, with no impact on our fair value estimate. From a long-term perspective, the apps being down could modestly affect user growth and engagement on the firm’s platforms as users may have found other social networks on which to spend their time. In addition, the outage mayh ave created some frustration for advertisers that ads on Facebook may not be dependable.

However, we don’t expect the seven-hour outage will have a long-lasting impact on the firm’s network effect. The effect of the Wall Street Journal’s reports, in addition to the whistleblower’s interview on CBS’s 60 Minutes on October 3, and her scheduled testimony in front of some lawmakers on October 5, could be made slightly worse when combined with the outages reported on October 4. While the CambridgeAnalytica ordeal that the firm faced in 2016 and 2017 is not directly comparable with what the firm is facing currently, Facebook user and monetisation growth decelerated shortly after, which is also what we are assuming in this case.

Our slower growth assumptions in users and monetisation (mainly in the US) in such a scenario resulted in a $379 Facebook valuation, 7% lower than our base case. However, our fair value estimate of Facebook remains at $407 as we think the firm is well-experienced on this front to address the latest issues even as it continues to get hit by negative headlines. In addition, we remain confident that advertising by new small and midsize businesses will increase, mostly offsetting the possible short-term impact of the current ordeal. For these reasons, we think the likelihood of a $379 valuation scenario is less than 15%.