Active share is a measure of the difference between a portfolio and a benchmark. It’s an important concept for investors wishing to judge how fund managers’ portfolios deviate from the index, and how that affects performance. It can show clearly when a fund is a "closet index tracker", one that holds shares very similar to the index but charges fees associated with active management. (The higher the active share, the more the fund differs from the benchmark).

Here, we take a look at the results of our recent active share study, Context Is Everything When Using Active Share (authored by William Chow, Mathieu Caquineau, and Matias Mottola), through a UK equity lens. That report is a comprehensive global study of 43 Morningstar categories across developed and emerging markets.

It's evident that active share can be a useful tool in identifying managers' styles and the extent to which their funds differ from their indexes. The context of the market in which the fund invests, however, is key.

Looking at active equity funds across the globe, some invest in narrow markets, such as Danish, Italian, or Singaporean equities, with highly concentrated benchmarks and only a short list of constituents. On the other hand, in global or regional categories, indexes hold a far longer list of names, with the largest stocks carrying lower weights than in narrow-market indexes. In a broadly diversified market like this, an active fund manager can deviate from the index much more easily, without excessively diverging in terms of style or market cap, than in a concentrated market. As a single-country market, the UK is reasonably large in terms of the number of issuers, but it does have a degree of concentration at the upper end, which can potentially limit the active share for large-cap-focused portfolio managers.

In the study, we took a broad look across Morningstar Categories to understand similarities and differences between their levels of active share. This allowed us to show just how different categories are in terms of their active-share profiles, confirming the intuition that top-heavy indexes represent a more difficult investment universe from which to build high-active-share portfolios, at least without taking meaningful off-benchmark positions. The number of securities in a benchmark also plays a role, but to a lesser extent than concentration.

Active Share in Context

The differences between categories demonstrate that a fund's active share is a more useful piece of information when put in the context of the fund's peer group, rather than as a stand-alone absolute measure. Also, drawing a limit between what can be considered an active manager and a closet indexer (a fund that charges active management fees but closely resembles its benchmark) cannot be a one-size-fits-all judgment.

With a UK large-cap equity fund, for example, where the manager is picking from a relatively limited investment universe that is reasonably concentrated at the upper end, one would typically expect a lower active share than in a global small-cap fund, where the choice is much wider and index concentration much lower.

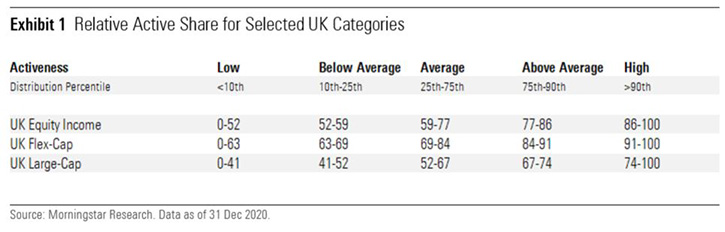

The study therefore proposed a relative framework to classify funds based on their level of active share against a relevant peer group¹.

In the UK large-cap equity category, a fund would require an active share of at least 74% to receive a high relative active share mark under the proposed methodology². For UK flex-cap equity funds, which invest more widely across the UK equity market-cap spectrum and therefore allocate to small- and midcap stocks to a greater extent, the figure stands at 91%, reflecting that flex-cap funds typically make use of the wider investment set available to them, taking them further away from the index and thus raising the bar for what can be considered a high active share in that category.

(While we use a 10-year period for active share calculations [2010-20], it's worth remembering that active shares within a category can change through time as markets change and as new managers and strategies come in and others exit. Thus, the limits quoted on the Relative Active Share scales are to be taken as a guide rather than the final truth to the decimal point.)

Bigger Share, Better Returns?

In line with previous Morningstar studies, we failed to find a systematic and consistent link between high active share and superior returns across all the categories assessed. Despite this, there was an interesting dynamic within the three UK categories included in the study (UK large-cap equity, UK flexcap equity, and UK equity income): Over the period of assessment³, higher-active-share funds outperformed lower-active-share funds.

However, there are many factors at play underneath the headline figures. For example, most of the 10 largest UK companies underperformed the wider UK market over that period, including the likes of HSBC, British American Tobacco, BP, and Royal Dutch Shell. With the most-active managers more likely to invest away from index heavyweights, this benefitted them. Style and sector dynamics also come into play here. We can see the opposite phenomenon in global categories, where the most-active funds have been hurt by the outperformance of the largest index constituents – Apple, Microsoft, Facebook, and Alphabet.

Across the range of UK equity funds rated by Morningstar manager research, we can see examples of both high- and low-active-share funds that have built strong long-term performance track records. Within the UK equity-income category, Franklin UK Equity Income, whose clean share class has a Morningstar Analyst Rating of Gold, typically has an active share of around 50%, which is considered low in both absolute terms and relative to the wider UK equity-income category.

Over the course of long tenured lead manager Colin Morton's stewardship of the fund, it has never trailed its benchmark on a rolling 10-year basis. Morton builds a core of large-cap companies with low portfolio turnover. He looks for steady companies where cash flow, earnings, and dividends can compound over time, incrementally building performance. Around the edges of the portfolio, he may seek to take advantage of valuation anomalies slightly lower down the market-cap scale when appropriate opportunities present themselves.

JOHCM UK Equity Income, which has an Analyst Rating of Silver on all share classes, has delivered topquartile performance within the category over the past 10 years (to the end of August 2021) using a different approach. While the portfolio still includes some of the traditional large-cap dividend-payers at the top end of the market, it also typically features a significant allocation to small- and mid-cap stocks. With its active share having increased over the past couple of years, it is above average in this regard within the category at present. Clive Beagles and James Lowen have managed the fund since launch in 2004, and they have been consistent in implementing an investment process that can lead the portfolio to diverge from the index and peers at the sector and market-cap levels.

Within the UK large-cap equity category, funds with notable style biases tend to feature at the higher end of the active-share scale. One such fund is Gold-rated (clean share class) Jupiter UK Special Situations, which has been managed by Ben Whitmore since November 2006 using a genuinely contrarian and value-orientated investment philosophy. His overall track record has been strong during this period. With an active share of around 80% as of second-quarter 2021, it is at the higher end of the category. Whitmore has continually shown the courage of his convictions in building the portfolio, which can look quite different from the benchmark at the sector and market-cap levels. His process means he can be early into names or avoid popular areas of the market, which can result in short-term relative underperformance, but investors have been well-served over the longer term.

Due Diligence Matters

Context is important when considering active share. A category's median active share goes hand in hand with index concentration, so the figure for a UK large-cap fund is not directly comparable to that of a UK small-cap fund, for example. The Relative Active Share metric allows investors to better understand how high or low a fund's active share is in the context of a category.

The full study found no consistent link between the level of active share and propensity to outperform. While it has tended to be a good choice to have exposure to active stock-picking risk over the past 10 years in the UK market specifically, there are many factors at play, from the landscape of funds in each category to the differences in returns by industry, style, and market capitalisation. Indeed, in other markets, such as global equity for example, the opposite has been true given the meteoric rise of the tech giants leading the growth charge.

When appraising funds, it is key to account for the risks involved with a high-active-share product. As active share grows, the dispersion of returns starts to grow: outperformers can do very well against the index, while highly active losers could experience horrendous losses. This again reinforces the importance of thorough due diligence when selecting active equity managers, especially those who aim for a higher active share.

1. For detailed methodology, please refer to the full-length study. Under this new classification method, funds that reach the top 10% of the distribution within the Morningstar Category receive a High active share mark; the next 15% of funds receive an Above Average; the middle 50% earns an Average; the next 15% receive a Below Average; and the bottom 10% get a Low.

2. The active share of all UK equity categories and funds discussed here is calculated using the Aviva Investors UK Index Tracking Fund.

3. Performance was assessed over three-year rolling periods from January 2010 to the end of 2020.