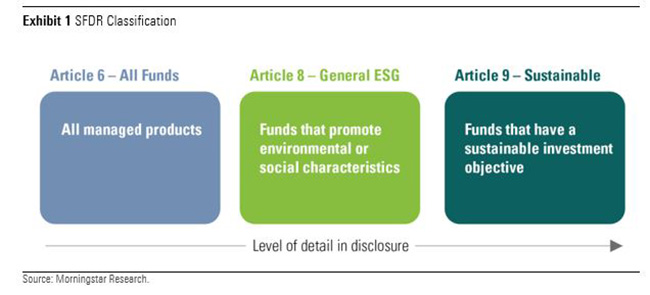

On March 10, the EU Sustainable Finance Disclosures Regulation (SFDR) took effect, requiring for the first time that asset managers provide information about their investments' ESG risks as well as impact on society and the planet. Funds have been classified into one of three categories, Article 6, 8, or 9, based on the sustainability objective. Article 8 and Article 9 funds will be asked to provide more detailed ESG disclosure, as laid out below.

Since March, asset managers have upgraded strategies and launched new ones that meet Article 8 or 9 requirements. For example, in May, JPMorgan uplifted 55 funds from Article 6 to Article 8. Out of 210 funds launched in the second quarter for which we have reviewed SFDR disclosures, 48% were classified as Article 8 or 9. Fund companies feel commercial pressure to have as many funds as possible meeting at a minimum Article 8 requirements. Many distributors and fund buyers across Europe have said they would only consider funds in Article 8 and 9 categories going forward.

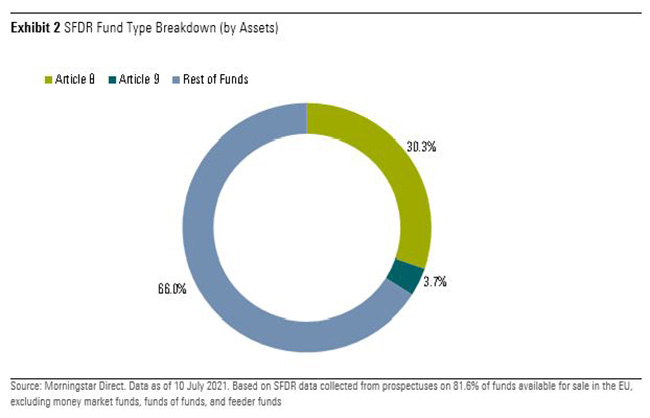

As a result, from 34% today, we predict that Articles 8 and 9 funds could reach 50% of overall EU fund assets within the next 12 months. Several managers are already reporting higher asset ratios, including Amundi (75%), BNP Paribas (80%), AXA (90%), and Robeco, (93%), while others who are currently exhibiting lower numbers plan to catch up. For example, DWS aims to categorise the quasi-totality of its EU fund assets under Article 8 or 9. Schroders targets a 70% ratio by the end of the year.

Different Approaches to Product Classification

Asset managers have taken different approaches to product classification based on their own interpretation of the regulation. This has resulted in a wide range of products labelled Article 8 or Article 9, from very light exclusions-only strategies to dark green impact portfolios. Similar strategies feature in both categories, suggesting that some asset managers may have taken a too prudent approach or others a too generous approach. Managers who parked more funds into Article 9 may be more confident in their ability to demonstrate the “sustainable” nature of their investments in their future disclosures.

Active management largely dominate the post-SFDR ESG fund landscape. Passive funds account for only 11% of assets in Article 8 and 9 funds, half the market share for passive funds in the overall European fund universe.

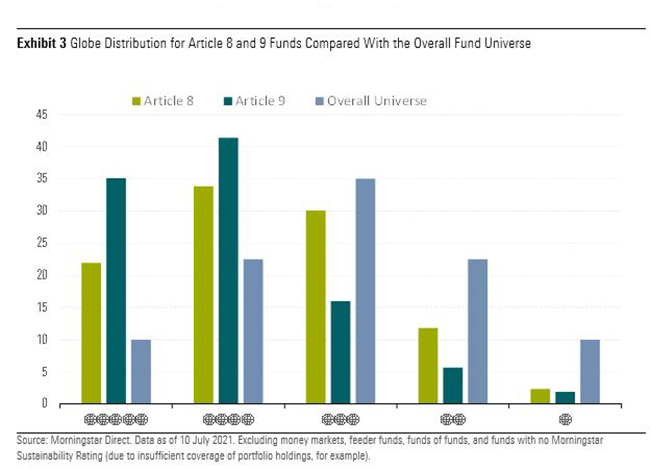

In aggregate, Article 8 and 9 funds perform better on ESG metrics than the rest of the universe, Article 9 portfolios exhibiting higher sustainability credentials, as expected. Three fourths of Article 9 funds carry Morningstar Sustainability Ratings of either 4 or 5 globes, compared with 56% of Article 8.

Article 9 funds also typically have lower involvement in controversial weapons, tobacco, fossil fuel, and severe controversies. They have higher exposure to carbon solutions, but at the same time they also exhibit higher exposure to thermal coal. The latter can be explained by the relatively high number of climate-themed funds in the Article 9 category that invest in traditional utilities companies that have built large renewable energy operations but still operate their highly intensive coal-fired electricity generation activities.