There has been a significant growth in thematic investing in recent years. Of late, this has concentrated on the mega trend that is ESG.

Thematic investing is defined by the CFA Institute as selecting companies within various sectors that are relevant to a particular theme. This type of focused investing shows a desire among investors for options that reflect their personal preferences and interests.

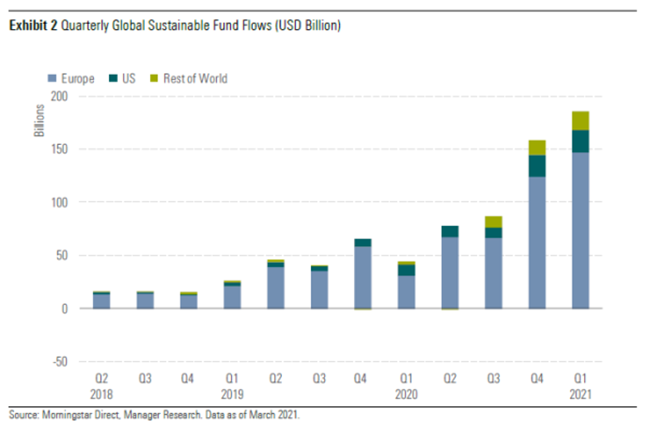

The chart below shows the huge growth in assets for Sustainable funds by quarter over recent years, and we have seen ESG EETFs dominate fund flows in the first quarter of 2021.

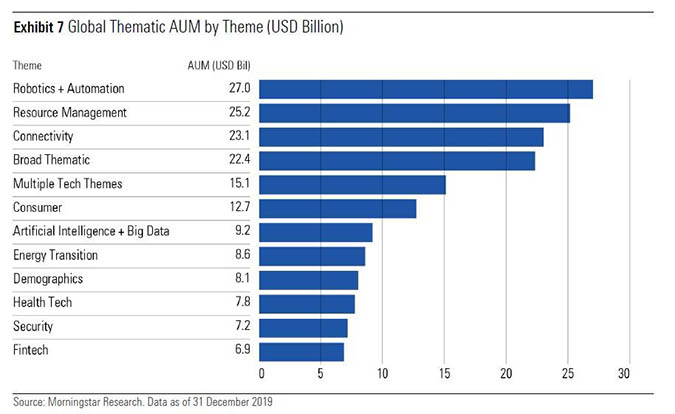

But the growth of thematic funds outside of ESG is also significant. Asset managers are racing to launch thematic fund strategies that are focused on increasingly niche segments of particular themes, enabling investors to get ever more granular in their investments. This is taking money away from more traditional funds and asset classes and the chart below shows how assets under management in thematic funds has grown.

Despite this obvious investor interest, Morningstar’s research shows that thematic investing is fraught with potential risks. Investors are making what in gambling is called a Trifecta bet; one where the investors must pick the right theme, the right investment vehicle to get exposure to that theme, and finally get the timing right. None of these three elements are easy, let alone getting all three right at the same time.

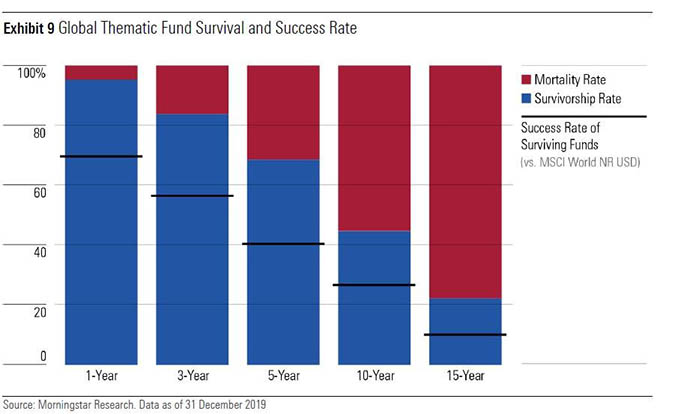

The chart below demonstrates the poor success that thematic focused funds have had over time. Fewer than 10% of funds have outperformed a broader benchmark over the longer term, and more than 50% have actually been closed down.

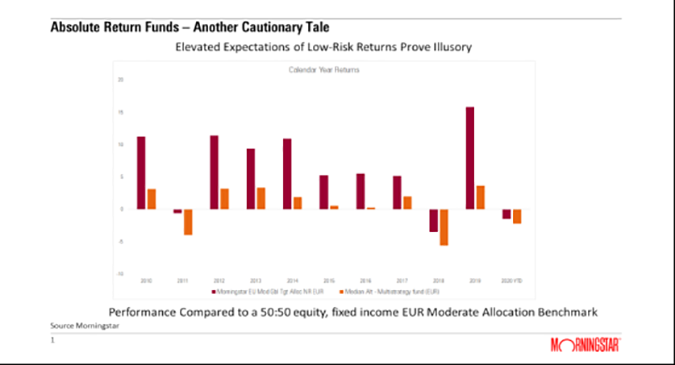

There is a cautionary tale for the industry in what we observed with Absolute Return funds over the past decade. This was an asset category that garnered huge assets in funds such as SLI Global Absolute Return Fund as investors were promised steady, and inflation-busting returns, with lower risk than equity markets. The chart below, however, demonstrates clearly the poor performance outcome of absolute return funds relative to a benchmark 50:50 equity bond index. Unsurprisingly, what followed were huge outflows from such funds.

There is, arguably, a balance needed between investor desire for investments linked to their interests and passions, and the dangers of investing in new, and potentially risky, areas.

Investors will increasingly demand more digital content and information, better optionality and personalisation, and investment platforms that allow them to engage directly with their particular interests. It may no longer be sufficient for financial advisers to advocate that investors invest in a single fund or portfolio for the long-term. The idea that there is a one-stop shop strategy to suitmillions of investors, all profiled in the same risk/return bucket, may not reflect the options available through continued innovation.

As investors become better informed and more engaged, and the number of options continues to expand, traditional funds may increasingly be challenged. Investment platforms and new fintech entrants will observe these trends and develop more innovative solutions and investing options for their customers, who will vote with their feet. We can already see this at play in the US, where the use model portfolios and indexing are growing at an unprecedented rate.

Innovation around digital functionality, research, investment and educational content is key. Investors expect optionality and personalisation with solutions that can suit their individual preferences, interests and risk profiles. In addition, quality research and educational content is essential to help avoid the pitfalls that can be destructive to long term savings and wealth. Moving away from the "one size fits all" product mentality, to one which embraces solutions which accommodate more pluralistic, democratic and modular investor requirements, will put investors in good stead, now and in the future.