Global equities investors have enjoyed a long run of success. The Morningstar Global Markets Index, a broad gauge of developed and emerging markets shares, has returned roughly 10% a year in pounds for the trailing 10 years to the end of April 2021.

But not all markets have participated. While US stocks have gained 14% a year over the decade, led by the likes of Amazon.com (AMZN), Apple (AAPL), Microsoft (MSFT), and Tesla (TSLA), the Morningstar UK Index, which includes large, mid, and small cap stocks, has gained just 5.8% a year since May 2011.

Too little technology and too much energy has held the UK back. The fallout from Brexit, both real and perceive, has weighed on the market, while banks like HSBC (HSBA), Standard Chartered (STAN), and Lloyds (LLOY) have struggled. Deliveroo’s (ROO) disappointing recent IPO was yet another setback.

But that’s the past. Today’s valuations imply higher expected returns for UK shares than for many markets around the world, including the US. That’s the conclusion reached when assessing valuations for the Morningstar UK Index's constituent companies.

UK Equities Through a Valuation Lens

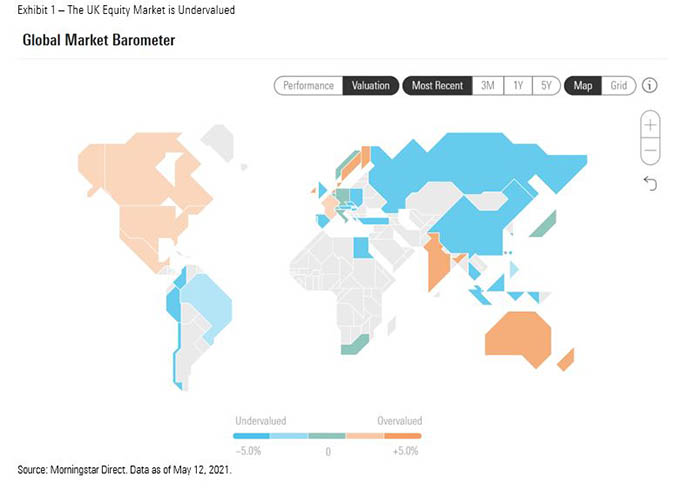

As depicted by the Morningstar Global Market Barometer’s valuation lens (exhibit 1), the Morningstar UK Index trades at a discount to its fair value, in contrast to the US and many global markets.

The weighted average of the Morningstar UK Index's constituents represented a 7% discount to fair value as of May 12, 2021. The US, by contrast, traded at an 5% premium, on average. Other markets that look richly valued include France, the Netherlands, the Nordics, Canada, India, and Australasia. By contrast, Spain and Belgium both traded below estimated fair value, as did Russia, Poland, Turkey, and several emerging markets in Latin America and Southeast Asia.

The valuation lens is formed through bottoms-up, company-level assessments applied to Morningstar’s range of national equity market indices. Index-level valuations are derived from price/fair value ratios assigned by Morningstar equity analysts augmented by a quantitative model. The valuation lens should be viewed as directional in nature.

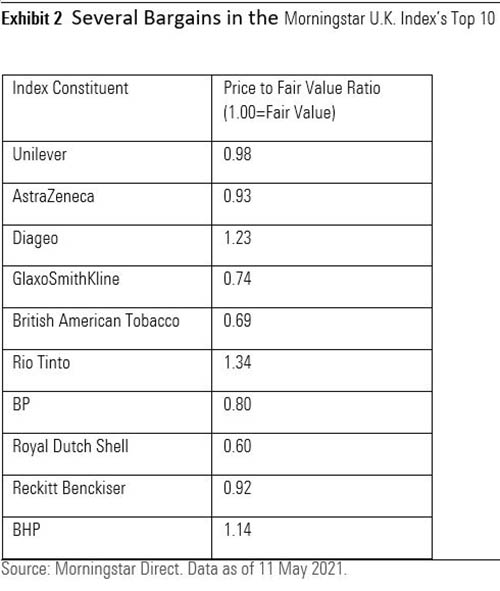

Several of the Morningstar UK Index's top 10 appear attractively valued as of May 2021 in the eyes of Morningstar equity analysts (see exhibit 2).

How Did the UK Get Here?

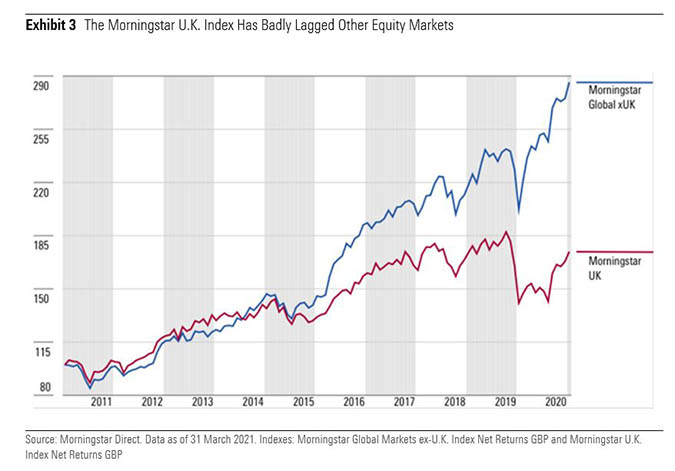

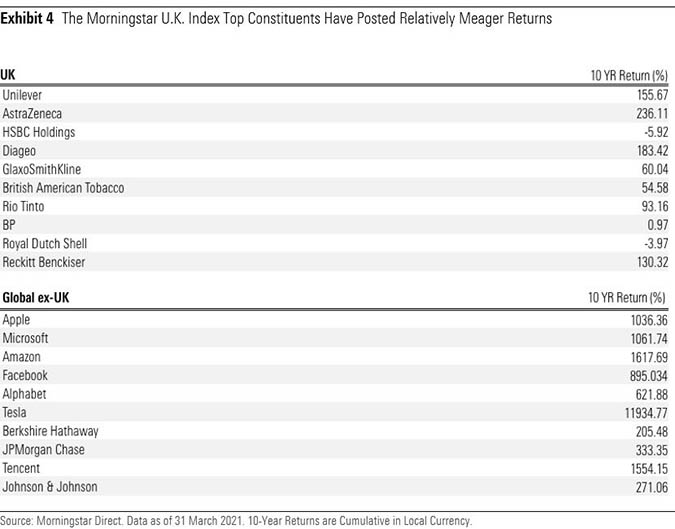

Consider the 10-year performance of the Morningstar UK Index relative to global equities (exhibit 3). The UK market posted relatively strong returns for a few years following the financial crisis, then faltered.

What accounts for this return gap? For one thing, sector and style biases have disadvantaged the UK. Technology has been the best performing global sector over the past 10 years, driven by ongoing digital transformation, but energy has been the worst. Tech stocks represent less than 2% of the UK market, compared to nearly 20% for Global ex-UK. Energy is 8.5% of the UK market (and was nearly 15% at the end of 2016), but just 3% of global equities outside the UK. With its generous helpings of financials, materials, consumer defensive, and energy stocks, the Morningstar UK Index leans to the value side of the market, which left it out of step during a growth-dominated period.

Brexit was another drag on the market. Uncertainty, depressed business investment, and currency volatility reigned for years. No sooner was an agreement signed, than the pandemic arrived to shave 11.5% off UK equities in 2020, while global equities outside the UK gained 13.8%. The economically sensitive sectors that dominate the UK market plummeted as tech companies benefited from the "new normal" of work-from-home, shop-from-home. According to Morningstar data, 157 of the UK Index’s 329 constituents cut dividends in 2020 – the most since 2008.

Finally, several prominent UK stocks have faced idiosyncratic challenges. Unilever is adapting to changing consumer tastes. GlaxoSmithKline (GSK) has wrestled with litigation and will see its business split. HSBC and Natwest (NWG) have been undertaking complicated restructuring of their banking operations.

Sunnier Days Ahead for Blighty?

But the Morningstar UK Market Index would not carry the upside potential implied by its forward-looking valuation were it not for several growth catalysts.

- Brexit is over for better or worse, and even as the UK sorts out its place in the world, uncertainty has lifted. The UK remains a competitive economy with many advantages, including its time zone.

- The UK stands out as a global success story for Covid-19 vaccination, which positions the country for a strong economic recovery. In fact, the Bank of England has raised its growth forecast to 7.5% in 2021, on the back of rebounding consumer spending and lower than expected unemployment.

- Regardless of the UK economic picture, investors should remember that less than 30% of the Morningstar UK Index's aggregate revenue is sourced from the UK, according to Morningstar estimates from 2019 corporate disclosures. The UK equity market is dominated by global players.

- UK banks are recovering. Morningstar financial services analyst Niklas Kammer reports that the banks weathered the pandemic "unscathed" with far lower loan losses than feared. Interest rates, whose dip into negative territory hurt banks, are likely to normalise. Dividends are coming back. This bodes well for companies like Barclays (BARC), Lloyds, and Natwest. HSBC is also rebounding nicely, and Morningstar analyst Michael Wu sees the company as well positioned to profit from growth in China.

- Dividends are coming back across the board. Banks, energy companies, and miners look well positioned to resume shareholder payouts. Rising commodities prices will help several UK market constituents.

- While the energy sector faces secular challenges as the urgency to combat climate change intensifies, there are reasons for investor optimism regarding large UK market constituents BP (BP.) and Shell (RDSB). Both are moving aggressively into renewables and low-carbon energy sources, such as hydrogen and biofuels.

- Unilever's (ULVR) management is taking "the right steps to optimise investments in its business" in Morningstar's eyes and has competitive advantages built around its supply chain.

- AstraZeneca (AZN) will not benefit directly from its Covid-19 vaccine, which carries not-for-profit pricing, but its "pipeline is emerging as one of the strongest in the drug group" according to Morningstar healthcare analyst Damien Conover, who also sees GlaxoSmithKline as benefiting from long-term demand for its shingles vaccine.

- Low valuations and a depressed currency make UK corporates attractive targets for overseas buyers and private equity.

Boring Can Be Beautiful

The UK equity market is not the world's most dynamic. The top 10 constituents of the Morningstar UK Index – all prominent market players one decade ago – have lost lustre compared with the US and China, where current champions like Facebook (FB), Tesla, Alibaba (BABA), and Tencent (00700) have experienced meteoric rises. But valuations for the global technology darlings of recent years look stretched. Growth stocks have been in favor since the financial crisis of 2008 and could well pass the baton to their underperforming counterparts on the value side of the market. Ultimately, valuation is a critical driver of long-term investment returns. At current prices, UK equities represent good value for money.

.jpg)