Absolute return funds are designed to perform whatever the market conditions, and are often promoted as “all-weather” solution to market volatility. A year on from the coronavirus market crash, we have crunched the numbers on what has been a turbulent period for world stock and bond markets. How have these funds performed over this period?

Stress Tested

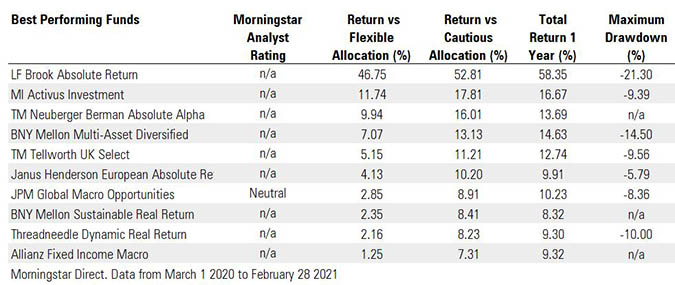

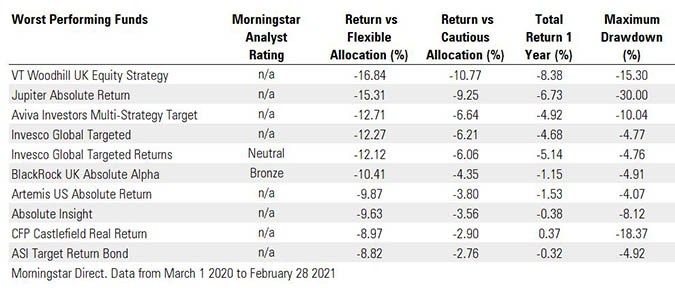

We last looked at absolute return funds in the immediate aftermath of the March sell-off and found that only in one in four managed to produce a positive return in the first quarter of 2020, a period that provided a severe test for even the most experienced and talented managers. A year on, we have looked at the same cohort of funds, those in the Investment Association Targeted Absolute Return category. Over a one-year period, performance has been mixed – 54 funds out of the 66 are in positive territory, while the rest are still down. The best performer on this measure by a long stretch was LF Brook Absolute Return Sterling I Acc with a gain of 58% (the next best fund was up 16%) and the worst was VT Woodhill UK Equity Strat Net Inc GBP with a loss of around 8%.

Excess Return

When we look at the Excess Return these funds have produced, the results start to look different. We’re using the Morningstar EAA GBP Flexible Allocation Category as a benchmark - the category encompasses funds that can invest across asset classes, as Absolute Return funds are able to do. Some 50 of the 65 funds analysed failed to beat this benchmark over the past year, and most of these are single digit gains. Two exceptions are MI Activus Investment and LF Brook Absolute Return with an excess return of 11% and 46% respectively.

What explains LF Brook's overperformance? The fund's holdings are weighted towards small/midcap stocks with an average market cap of around £2 billion, while the category average is around £31 billion. The portfolio also has a much higher weighting towards basic materials, financial services, consumer cyclicals and industrials than the benchmark, areas which have performed strongly in recent months.

Jonathan Miller, head of UK manager research at Morningstar, says that beating the flexible allocation benchmark – where managers are free to roam across cash, bonds and equities – has been a tough test. After the crash, equities were the place to be and US equities in particular. The average equity exposure of the flexible allocation category had moved from 33% in May 2020 to a chunky 40% by January 2021 – and US equity exposure reached 15%.

Funds in the Targeted Absolute Return sector with weightings below this naturally struggled to match the performance of the category - the average weighting of the funds in this sector was 20%. The best performer, LF Brook Absolute Return, had a much higher exposure to equities, at between 80-90% for the period, than the rest of the funds in the sector. Timing was also a factor here: for example, Jupiter Absolute Return, which underperformed the category, had only a 7% exposure to equities in April, the month when markets rebounded strongly.

At the other end of the spectrum, the worst performers were VT Woodhill UK Equity Strategy with an underperformance of -17% and Jupiter Absolute Return, which was 15% below the benchmark. The Jupiter fund is under new management in 2021 after the departure of James Clunie, the manager who bet against Tesla.

Cautious Approach

The results are different again when the funds are benchmarked against the Morningstar Cautious Allocation category. The Bronze-rated BlackRock UK Absolute Alpha delivered an excess return of 6% against this benchmark, compared to underperforming by 10% against the Flexible Allocation category. This pattern of underperforming the tougher-to-beat category and beating the more conservative one is repeated across the fund group. Some 39 funds outperformed the Cautious Allocation category, with 26 failing to beat the benchmark.

Capital losses were a serious concern for investors last year and “how much has my fund fallen?” was a key question at some points in March and April 2020. Maximum Drawdown is a metric that captures this, showing the deepest trough in a fund’s performance over a particular period. Again, there is a substantial difference in this figure across the funds, ranging from a maximum drawdown of 31% for H20 Multireturns to 2.64% from Aegon UK Equity Absolute Return.

Should You Hold an Absolute Return Fund?

Absolute return funds are complex products. Darius McDermott, managing director of Chelsea Financial Services, says it’s important investors do their homework before taking the plunge: “Not all absolute return funds are the same. Some are very defensive, and some are not low risk at all. They all do very different things, so it is important to look under the bonnet and understand exactly what risk you are taking with a fund.”

Still, it’s clear that the majority of these funds failed to outperform against tougher benchmarks over a volatile period for world markets that provided a decent test for absolute return mandates. And with higher fees than traditional active funds and passives, it’s worth keeping a close eye on performance, especially if markets go through more turbulence this year.

- The data tables in this article have been amended to replace out-of-date data