As the Covid-19 has spread globally, it has left in its wake acute health concerns compounded by economic devastation. The full effects are still unfolding. The novel coronavirus has shone a spotlight on the “S” in ESG; the social side of businesses’ conduct and how companies interact with their workers, customers, shareholders and the wider community. This may alter the way people look at the investment world and the function of businesses.

According to World Economic Forum’s Global risks report 2021:“Underlying disparities in healthcare, education, financial stability and technology have led the crisis to disproportionately impact certain groups and countries. Not only has Covid-19 caused more than 2 million deaths at the time of writing, but the economic and long-term health impacts will continue to have devastating consequences.”

Three key statistics can explain how Covid-19 is impacting all aspect of our lives.

The New Poor

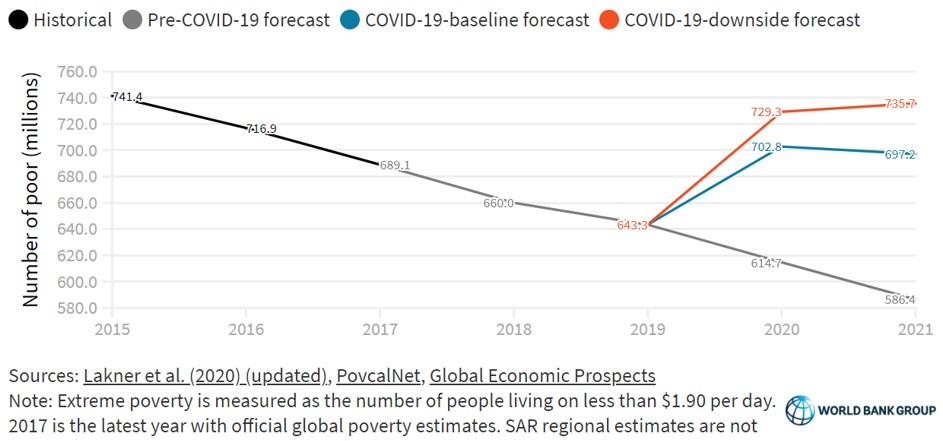

According to the World Bank, in 2020, after decades of steady progress in reducing the number of people living on less than $1.90 a day, the pandemic is expected to produce the first reversal in the fight against extreme poverty in a generation. The latest analysis warns that Covid-19 has pushed an additional 88 million people into extreme poverty in 2020, but in the worst scenario, the figure could be as high as 115 million.

Exhibit 1. Number of People in Extreme Poverty

Impact on Businesses and Employment

The pandemic slowdown has deeply affected companies and jobs. According to the World Bank Covid-19 Business Pulse Surveys conducted between May and August 2020, companies were forced to reduce hours and wages and, to a lesser extent, fire workers. With less money, people will be forced to make trade-off that could harm health and learning for generations.

Inequalities and Gender Gaps

The IMF, World Bank and OECD have all warned that unless something is done, the pandemic will lead to a sharp increase in inequality in almost every country. While the richest will bounce back from this crisis rapidly without help, ordinary families will take years to get back on their feet. Covid-19 has exposed and exacerbated inequalities between countries just as it has within countries.

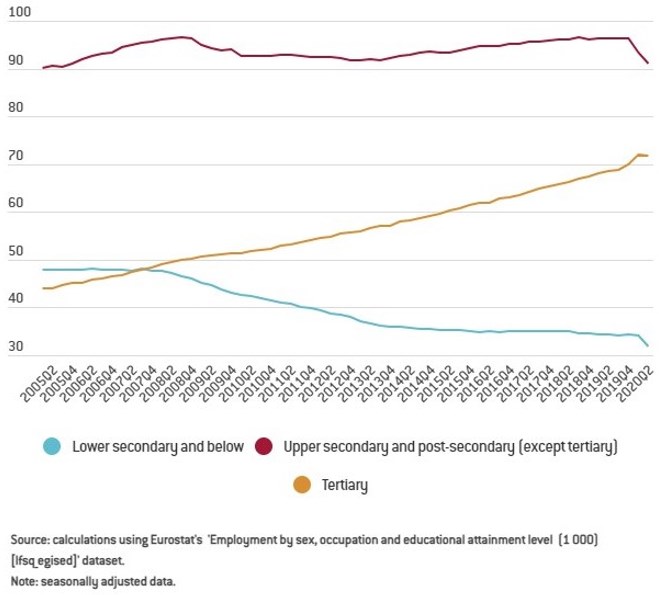

Zsolt Darvas, Senior Fellow, Bruegel Think Tank, said: “In the European Union, 8% of workers educated to lower secondary level or below lost their jobs between the last quarter of 2019 and the second quarter of 2020. Over the same period, the number of jobs for workers with university degrees increased by 3%. Jobs for employees with middle-level qualification declined by 5%”.

Exhibit 2. Employment by Educational Attainment Level in the EU, 2005 Q1 - 2020 Q2 (millions)

Source: Bruegel.

Evidence shows that gender gaps could widen, potentially reversing women’s decade-long gains in human capital and economic empowerment. According to the World Bank, during this crisis, women have lost their jobs at a faster rate than men, due to the fact that they are more likely employed in sectors hardest hit by lockdowns, such as retail and tourism, or in informal jobs that lack access to social protection.

The Social Dimension

There are two ways by which the importance of “social” dimension of ESG increased during the pandemic. The first one is the focus on stakeholders; the second one is impact investing.

Stakeholder-Capitalism Model

“Given the gravity of pandemic, companies had no choices but to prioritise their stakeholders”, says Jon Hale, head of sustainability research at Morningstar. “Researchers at Harvard found that firms generating positive public sentiment about the way they responded to the pandemic and their effects on employees, suppliers, and broader society outperformed their counterparts during the market collapse in the first quarter”.

Using the Covid-19 Corporate response tracker, Just Capital, a non-profit organisation, found that firms it accessed as doing the best job prioritising workers had more resilient stock return than those doing the worse. “This focus on corporate responses to the pandemic created greater awareness among investors for the importance of the "social" dimension of environmental, social, and governance analysis”, adds Hale.

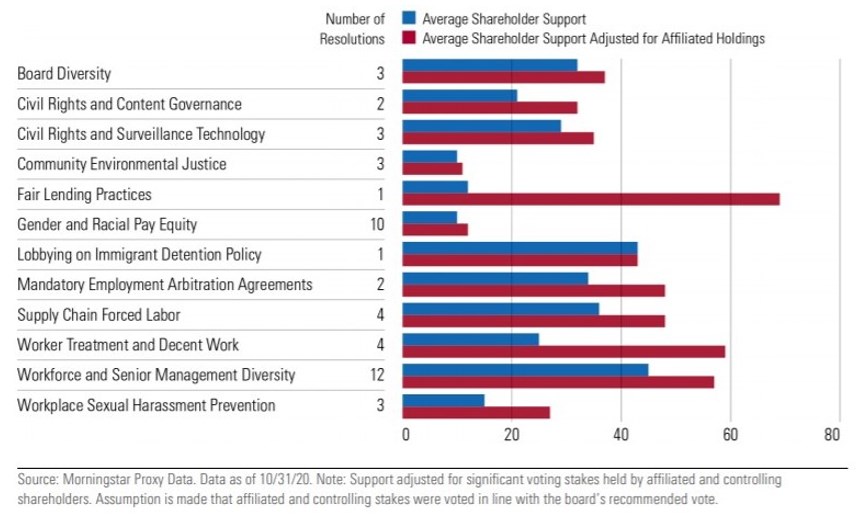

Resolutions raising investor concerns about diversity, equity, inclusion (DEI) and social justice were on the proxy ballot in 2020. After studying resolutions brought to vote at hundreds of companies in the US over the 2020 proxy calendar (July 2019 to June 2020), Morningstar identified 48 key resolutions on investor concerns ranging from workplace diversity, equity and inclusion to human and civil rights impacts on workers, customers and communities throughout a company’s value chain.

Exhibit 3. 48 Key Resolutions Addressing Diversity, Equity, Inclusion and Social Justice in the 2020 Proxy Calendar

Impact Investing

The pandemic has amplified systemic injustices facing minority groups, women, immigrants, and individuals living in poverty. For example, in the US, the Black Lives Matter movement has called new attention to the systemic racism facing Black and minority communities.

According to the Global Impact Investing Network (GIIN), “Many of these injustices are entrenched in political systems and social norms – and many are reflected in the economic structures that influence wealth-generating activities and shape wealth distribution.

"Recognising that investment occurs within the framework of a broader economic system, impact investors – along with policymakers, philanthropic actors, and the business community – have begun to reckon with their role in mitigating and reducing inequality and driving toward social equity."

Impact investing is defined by investors’ intention to generate positive, measurable social or environmental impact alongside a financial return. Using Morningstar Sustainable attributes, we counted about 1,700 impact open-ended funds and ETFs globally, of which 205 are focused on gender & diversity and 386 on community development. Other impact investment instruments include alternative assets like private equity and private debt, as well as closed-end funds.

Impact Investors for Social Equity

In May 2020, prominent impact investing networks, supported by a group of leading foundations, launched the Response, Recover, and Resilience Investment Coalition (R3 Coalition), managed by GIIN, aiming to streamline impact investing efforts that will address the large-scale social and economic consequences of Covid-19.

According to a survey published in September 2020, as the pandemic has emphasised and exacerbated long-standing disparities, more impact investors have sought to reimagine or amplify their efforts to contribute to positive solutions that strengthen both market and societal resilience to future crises. Specifically, investors indicated three critical, intersectional types of inequality: those reflecting poverty, gender, and race or ethnicity.

Strategies to strengthen social equity include:

- Diverse perspectives into investors’ own organisations.

- Review and assess investments’ context and their baseline performance on social equity indicators.

- Develop intentional deal sourcing strategies.

- Incorporate diversity, equity, and inclusion factors into due diligence assessments.

- Target sectors or business models that drive social equity.

- Ensure that investment terms align to investment goals and investee context.

- Drive social equity through ongoing, adaptive post-investment support.