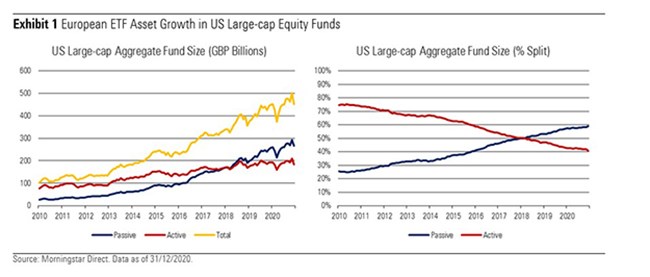

The past 10 years has seen a change in the balance of power between active and passive funds in the US equity space. The amount of money invested in passive US index funds by European investors has ballooned from £26 billion to £266 billion, making them the preferred option for the majority of European investors at nearly 60% of aggregate assets.

While the tremendous growth of mutual fund assets over the past decade is not exactly news, the switch in preference in the US Large-cap space is not something that’s been seen elsewhere in other developed markets. A few explanations come to mind when it comes to thinking about what makes passive strategies so attractive for US equity exposure.

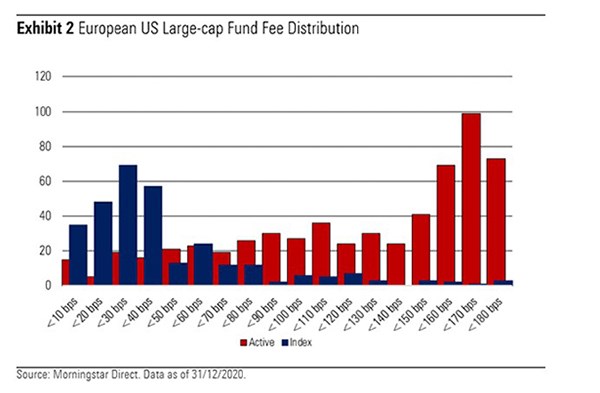

Fees on US Trackers are Low

The first reason for the rise of the US tracker fund is their fees. A well-known advantage of index funds is their competitive cost structure. Owing in part to the high liquidity of the US equity market, funds which mirror the markets, whether physical or synthetic, are relatively inexpensive for asset managers to run. Accordingly, funds in this space are extremely competitive, with annual charges typically less than 0.20%, or 20 basis points (bps) - equivalent to just £2 for every £1,000 invested.

The same can’t be said for active funds, where the vast majority are priced at 0.70% or more. Despite the cost advantages, however, some investors are willing to forego cheaper index strategies if they believe they can select managers who can consistently beat market-weighted strategies such as the S&P 500.

The US Market is Hard to Beat

That brings us to the second reason investors have flocked to tracker funds for US equities.: the odds of beating the benchmarket.

The US equity market is one of the most widely covered in the world. As with all equity research, analysts and fund managers carefully study companies to measure metrics of financial strength to generate better valuation opinions. Any information that can allude to a company’s fair value can lead to profit if a stock is mispriced, and market participants will actively seek out these sorts of opportunities. Given the extensive coverage of major US companies, such information is quickly incorporated into stock prices as shares of overvalued companies are sold and undervalued companies are quickly snapped up.

This phenomenon represents the idea of "market efficiency", where more efficient markets are quick to reflect changes in valuations as new information is made publicly available. It is much harder to gain an edge when investing in an efficient market, because you are less likely to come by information that is not already in the public domain and therefore already priced in.

Together with abundant liquidity, this limits the opportunity for active managers to add meaningful value. As markets are quick to react and erode opportunities, US equity fund managers regularly struggle to outperform passive alternatives.

Evidence over time shows that net active decisions in this market have tended to detract from returns. Using the Morningstar Active/Passive Barometer, for example, approximately 9 in10 active funds fail to beat a passive strategy after fees. This semi-annual report measures the performance of European-domiciled active funds against passive peers in their respective Morningstar Categories, and track records like these make strong cases for our highest Morningstar Analyst RatingsTM of Gold, reflecting our conviction in these fund’s ability to deliver superior risk-adjusted returns.

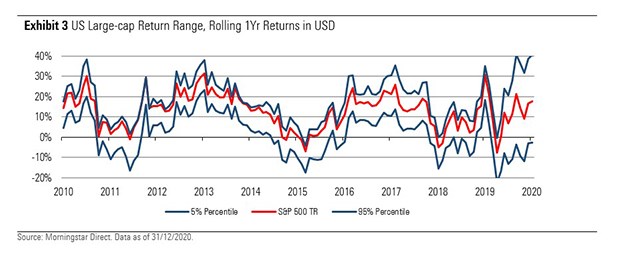

Exhibit 3 shows the range of returns for the universe of actively managed funds in US Large-cap categories over the last 10 years pitted against the S&P 500 index. The extremes of the top and bottom 5% of performers have been removed to better represent the vast majority of performance.

What we see is the S&P 500, a common index for US Large-cap passive funds to track, is consistently performing close to the higher blue line, which represents top end of the universe. For investors to continuously outperform the index strategy, they would have to consistently pick fund managers who are approximately in the top 20% of performers.

ETFs Have Dividend Advantages

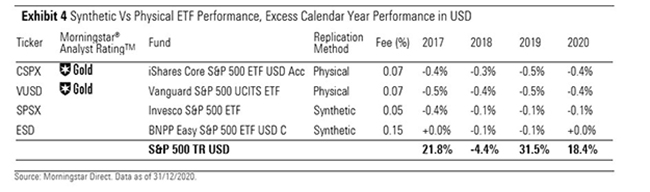

The final reason for the rise in US ETFs is a performance advantage that certain European-domiciled Exchange-traded Funds (ETFs) carry. ETFs that rely on total return swaps present an attractive option for investors, however, US equity funds that are domiciled outside of the US are typically subject to withholding tax of 30% on dividends they receive from their underlying holdings.

This rule also applies to derivative securities that would avoid taxation by replicating total return strategies to receive dividends at reduced rates. However, certain synthetically replicated exchange-traded funds (ETFs) that track qualifying indices such as the S&P 500 are exempt from this withholding tax, and are instead subject to a reduced tax rate of 15%.

Because of this, synthetic ETFs fetch a small premium over their physically-replicated counterparts over time. As shown in the Exhibit 4, this excess performance can range between 0.10-0.40% depending on the success of other factors such as securities lending and fee.

These synthetic ETFs are still gaining traction as investors come to grips with the the unique risks associated with synthetic replication, but their potential to offer consistently superior returns makes them an interesting proposition for investors seeking tax-efficient vehicles.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/347BSP2KJNBCLKVD7DGXSFLDLU.jpg)