Global equities made a staggering comeback in November after October’s lull, with markets pushed higher by a Biden victory in the US Election and positive developments in the race for a coronavirus vaccine. Some European benchmarks put in record gains for the month, while in Japan the Nikkei posted its biggest gains for 26 years. In November, the Dow Jones broke through the 30,000 level for the first time.

UK benchmarks also took part in this wider global rally. The Morningstar UK Index, which covers 302 stocks from £348 million in size (Go-Ahead Group) to £186 billion (Unilever), was up over 13% in November alone, erasing some of the losses in the year to date. Our latest Market Barometer reveals how value, growth and blend stocks have performed after November’s rally.

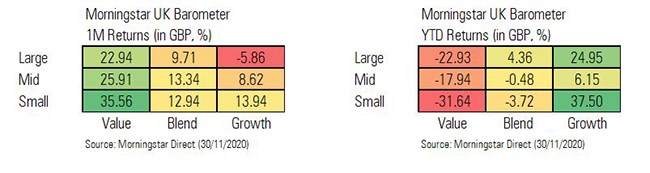

Global large-cap growth stocks have been dominant this year and this trend has also played out in the UK, with this category up by just under 25% so far this year. Large-cap commodity firms have been a big beneficiary of November’s bounce on the grounds that a faster-growing world economy, especially a booming China, will need more natural resources. London-listed copper miner Antofagasta (ANTO) has been one of the stocks that have benefited most in the large-cap growth space, with its shares rising nearly 22% in November – since January the shares are up 37% even after the March slump.

But of the 10 names in the large-cap growth cohort, the majority are in negative territory this month – unlike the 18 stocks in the large-cap value list, which all posted positive returns in November. Big value names like Royal Dutch Shell (RDSB) and Lloyds Banking Group (LLOY), which are nursing hefty losses this year, posted gains of nearly 30% in the month as energy and financial stocks returned dramatically to favour (a trend seen in our best and worst performing funds of the month).

November Gains, 2020 Losses

The extent of this rebound in value is laid bare in the numbers: the November gains for large-cap value stocks are roughly the same as the year-to-date losses at around +23% and -23%. For small-cap value, the difference is even larger: a gain of 35% in November, versus a loss of nearly 32% in the year to date.

While the performance of mid-cap growth names was mixed (27 risers versus 20 fallers), 25 out of 26 the mid-cap value names gained last month. Travel stocks were big winners in November as positive vaccine newsflow encouraged some holidaymakers to envisage an earlier-than-expected trip next year. Package holiday group Tui (TUI) posted gains of nearly 70% in November, followed by easyJet (up 59%) and cruise company Carnival (up 56%).

These travel and leisure companies’ share prices are still sharply down since January – as we’ve written recently, a large share price slump makes it harder for investors to recoup their losses even if there’s a substantial rally. A prime example of this in the small-cap value list is cinema owner Cineworld (CINE), whose shares almost doubled in November from 27.5p to around 27p (they started the year at 220p). Small-cap travel and leisure companies were also among the month’s biggest gainers in percentage terms.

Despite value’s dramatic comeback last month and growth’s stumble, the year-to-date figures are stark: large-cap value is down around 23% while large-cap growth shares have gained by a quarter, while small-cap value is off 32% this year, while small-cap growth has gained an impressive 37.50%.