In countries with large historical home price increases, people tend to see ownership as clearly better. But there are still strong arguments for renting, both for young and old.

Yes, there are many advantages of owning your home. But renting brings other advantages, that to some people are even more important. What argument weighs most heavily for you probably depends a lot on your age.

But first, before discussing the argument for and against owning your home, it is important to be aware of the genuine uncertainty about future home prices. And the risks this creates, depending on how long-term your ownership is. Looking around the world, there are extreme differences in price movement in local housing markets.

A Look at House Prices Across Europe

Some countries have seen real home price more than double in the last 30 years, most notably Australia, Canada, New Zealand and Sweden. But according to the Economist house-price index, in other countries like Germany and Switzerland prices adjusted for inflation have stayed on the same level as 30 years ago. And in Japan they are 32% lower than in 1990.

The development of home prices during and after the financial crisis 2008/09 has also been very different. In Spain and the US, for example, prices fell dramatically and have still not recovered to the pre-crisis level. But in, for example, Canada and Sweden, home prices rebounded quickly and have continued to rise.

People’s expectations on future home prices are strongly influenced by local historical price trends. The question “Is renting throwing money away?” makes more sense in a country with rising prices. In countries with negative ownership returns, people focus more on the financial risk. But looking into the future we all have reasons to be cautious, since low interest rates in recent years have helped increase property valuations.

One of the most well-known experts on long-term home price movements is Robert Shiller, professor at Yale University. His summary of research on home price movements during 100-year time periods using the repeat-sales method (only including price movements of the same properties), show that the very long-term trend is that home prices stay constant in relation to household incomes. And outside dense urban areas, upward price movements are limited by construction costs. Based on this, countries with strong price increases in recent years should expect the supply to increase as well, until prices fall back to the long-term trend.

Arguments for Renting

Young people moving away from their parents, especially students, often have no other choice than renting. And even after gaining a first steady employment, there are other temptations in life.

Freedom is the key advantage of renting; not only avoiding a commitment to monthly bank payments and the cost of maintining your real estate, but also being more flexible when new opportunities appear. Avoiding the financial risk in home ownership means that you can be more flexible in the job market, and that more of your long-term savings can be invested in the equity market, with higher expected returns.

The risks caused by home ownership depends on how long you expect to stay. In the extreme case, where you live in the same house until you die, the limit is what monthly cost you can handle. On the other hand, if you might need to move again in 12 months, adding a price decline to transaction costs could make the experience terribly expensive.

Arguments for Ownership

Many common arguments for ownership centre around the potential for lower average cost. By doing repairs and upgrades yourself, using tax benefits, and hopefully realising capital gains in the end, you can afford a larger home -or downsize to free up money. Also, ownership gives more control and added safety, especially in countries where rent contracts are time limited.

By entering the ownership ladder, committing to investing in your home and paying down the mortgage, and with salary increases gradually moving to larger apartments and houses, it is possible to gradually grow real estate wealth. In some countries this is a dominant lifestyle of high-income families. But it is not necessary, in other countries renting is more common.

Age is clearly a key factor, deciding the strength of the some of the arguments above. Other arguments, like the trade-off between risk and potential returns are general.

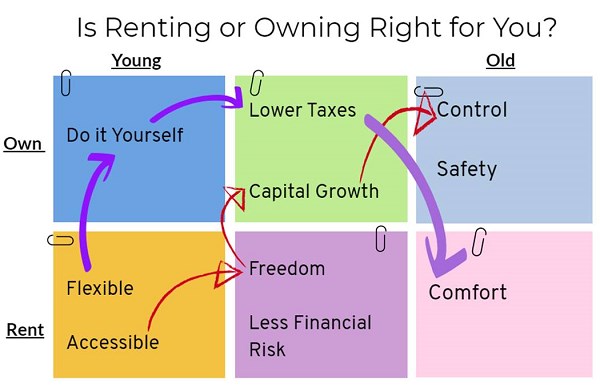

Young people tend to start by renting, both because they lack the financial muscles to buy a home and because they value their freedom. As illustrated in the diagram below, there are many potential paths, with different argument causing people to move.

Let’s look at two potential paths a person might take: Person A (indicated by the red arrows) decides to focus on upgrading a run-down apartment with do-it-yourself, later buys a larger apartment hoping to gain by additional tax advantages, realizing those gains at retirement by moving to a smaller rented flat with no responsibility for maintenance and housekeeping. Then more can be spent on travel and comfort. Oh, the comfort of just calling the landlord when something needs fixing!

Person B (purple arrows), meanwhile, first gives priority to flexibility and freedom. When finding well-payed employment in the capital, a rented flat is ideal to be able to stay career focused. Later, news stories of enormous capital gains in the housing market becomes too tempting, and after retirement the key argument changes to being able to control and decide all aspect of the interior and garden design.

Ultimately, there’s no right or wrong answer when it comes to renting or owning a home. As with any financial decision it’s important to base the decision on your overall goals, risk appetite and a host of other factors to determine which is the right choice for you.