Stock market volatility is on the rise again and that has meant some wild price moves for a number of companies, especially with the latest earnings season revealing how firms fared during the lockdown.

Some companies have done better than expected such as US tech giants like Facebook (FB) and Apple (AAPL), and Morningstar analysts have upgraded their fair value estimates on these shares. But bad results have also been coming thick and fast, leading to a number of downgrades.

Shares in so many high-quality companies have fallen sharply this year that it’s often hard to distinguish between the companies that are cheap for good reason from those which are genuinely undervalued.

We have screened for stocks that are rated five stars, meaning they are significantly undervalued, and which also have economic moats, meaning they have sustainable competitive advantages to find some potential bargains among heavily sold-off stocks. Most of the companies on our list are trading between 50% and 60% below their fair value.

What is the "fair value estimate" and why does it matter? Morningstar's Sarah Newcomb says: "It's a smart shortcut that can help you determine whether the price of a stock is high or low compared with its fundamental value. It's a much more reasonable estimate of the long-term fair value of a stock than 'whatever people are willing to buy it for today'". The fair estimate is based on analysis of the company's balance sheet rather than on current market sentiment and should not be seen as a price target, she adds.

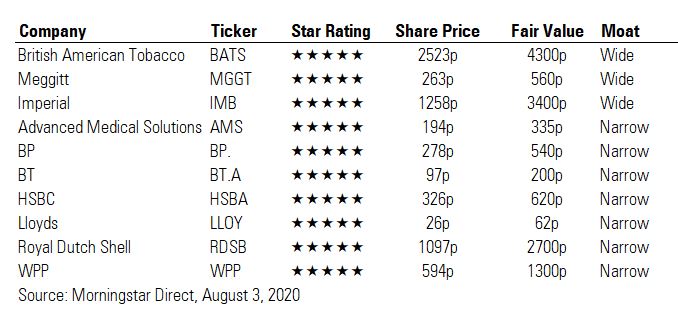

Which UK Stocks are Undervalued?

There are two banks on our list of undervalued stocks, Lloyds Banking Group (LLOY) and HSBC (HSBA). UK banks are unloved by investors for a lot of reasons, not least because this year they are unable to pay dividends. Recent results have shown banks increasing their forecasts for bad debts as the economic crunch hits family finances. Brexit is also a factor weighing on those banks with the biggest domestic focus such as Lloyds and NatWest.

Former four-star stock HSBC has fallen into five-star territory after a rough year including a tangle with the Chinese authorities over Hong Kong. Recent half-year results show a 65% fall in profits to $4.3 billion. Having started the year around 600p, shares are now around 322p, a fall of 46%. But Morningstar analysts maintain their 620p price target for the Asia-focused bank.

Another bank with a narrow economic moat that is trading sharply below its fair value is Lloyds. Morningstar analysts say the company’s fair value is 62p, but its shares are currently around 60% lower than this at 26p, nearly 60%. Morningstar banking analyst Niklas Klammer says that while UK banks are cheaper than they were in the 2008 financial crisis, they are in better financial shape; he also thinks dividends will start up again in 2021.

Oversold Stocks, Long-Term Opportunities

Meggitt (MGGT) supplies components to aerospace, defence and energy companies and has this year joined the elite list of companies with wide economic moats as well as being rated as five stars.

The company’s shares have fallen nearly 60% so far this year to 263p as oil companies and airlines have been hit hard by lockdown measures, but Morningstar analysts think the shares are worth 560p. Analyst Joachim Kotze is optimistic on the firm’s long-term prospects, particularly as countries continue to spend billions on defence and these contracts provide reliable cash flow; its wide moat is based on technical know-how and customer relationships.

Meanwhile, the freeze on live sport during lockdown has hit TV and broadband firm BT (BT.A), leading to a further downgrade in its fair value by Morningstar analysts – from 250p to 200p. Still, with shares falling below 100p after its most recent results, they are now trading at around 50% of their fair value.

“BT’s first quarter results weren’t terrible considering the circumstances, but management’s outlook for the remainder of the year is weaker than we were expecting,” says analyst Michael Hodel.

Elsewhere in our list is oil giant Royal Dutch Shell (RDSB), which made an eye-watering loss of $18 billion in the most recent quarter. Despite these results, Morningstar analyst Allen Good maintained the fair value estimate of £27, on the assumption that oil prices recover to pre-Covid levels of $50 or more - yet shares are currently changing hands at £11. Narrow moat BP (BP.), which has just announced a record Q2 loss and slashed its dividend, is also trading significantly below its fair value.