Coronavirus has disrupted many people's plans, from small ones like summer holidays to life-changing decisions like taking retirement.

For those who have saved diligently into a pension scheme for years, the sharp stock market sell-off in March may have derailed decades of planning. Because for those who don't have a final salary pension scheme, the amount in your pension pot is directly linked to how the stock market performs.

The advent of the pension freedoms (which means retirees no longer have to buy an annuity) means the traditional model of working for a set number of years, then retiring for a couple of decades appears to be on the way out. Instead, many people are choosing a hybrid retirement, continuing to work part-time while drawing down some income, perhaps topped up with rent from buy-to-let properties or income from shares.

But to do this, you need to be able to plan: how much will you need to live on, and which investments will deliver the income to sustain you through retirement? There is no right answer to the question “how much do I need in retirement?” but it’s one of the most important financial questions you will ever ask yourself.

Choose Your Retirement Package

Financial advisers have traditionally prompted people to target two-thirds of their salary when they retire. But with interest rates at record lows, this is harder than ever to achieve.

An annuity is a type of insurance product you buy with your pension pot; it promises to pay out an agreed annual income every year until your die. But the level of income you can buy with your savings is linked to interest rates and, as a result, the numbers make for painful reading these days.

Currently, a £100,000 pension pot buys an income of just £4,000 a year. According to the Office for National Statistics, the average salary is now £36,000 - to generate an income equivalent to two-thirds of that in retirement you would need a pension pot of more than £800,000.

Against this backdrop, it's unsurprising that a growing army of savers are opting for the DIY route in retirement, leaving their money invested in the hope it will continue to grow while they withdraw lumps for their income.

How Much do you Need to Retire?

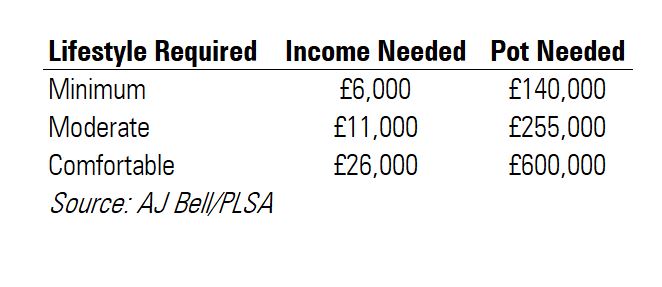

Tom Selby, senior analyst at AJ Bell, argues that a better way of looking at the problem is to target the minimum, moderate and comfortable retirements defined by Pension and Lifetime Savings Association (PLSA). These assume that a lot of discretionary spending goes on cars, holidays, clothes and eating out. Stripping out this type of spending, or reducing it, helps in setting more realistic goals.

“Work out how much you need to spend on essentials and how much you want to spend having fun,” says Kay Ingram, public policy director at financial planners LEBC. “Ideally essential spending should be guaranteed with flexibility around discretionary spending,” she adds. Selby also points out that the cost of care is increasingly a consideration for people as they get older, too.

Assuming that the State Pension pays you around £9,000 a year (if you’ve worked for long enough), AJ Bell analysis suggests a 66-year old with no underlying health conditions needs to generate an additional £6,000 a year to achieve the minimal retirement lifestyle laid out by the PLSA. AJ Bell calculates that a pension pot of £140,000 should be enough to achieve this income for life, assuming you leave the money invested and it grows at 4% a year - it's a far more achieveable savings goal than £800,000.

Those aiming for the PLSA's comfortable retirement lifestyle, which includes overseas holidays and home renovations, will naturally need to squirrel away more money. It suggests an income of £35,000 is needed in retirement for this type of living, which means retirees need to come up with £26,000 a year out of their own savings after taking the State Pension into account.

Of course, it's worth pointing out that these figures assume that your pension pot will dwindle down to nothing by the time you die, leaving nothing for loved ones to inherit. Those looking to leave a legacy behind will need to save more or spend less.

Getting Closer

Many workers may be closer to reaching the target for moderate and even comfortable retirement than others. According to a report by investment bank Close Brothers, the average pension pot of those working for firms with more than 200 employees is £120,000, up from £89,000 in 2017. Those aged 55 and over have an average pot of nearly £200,000, the report finds. So in this case a few more years saving could help someone upgrade from a minimal to moderate retirement. These figures are even higher in London and the south-east and for workers in areas like financial services.

Ultimately, though, only you can decide what is the right amount. “Everyone is so different. It’s important to ask the question, ‘how much do you need based on your circumstances’,” says Morningstar’s head of retirement research, David Blanchett.