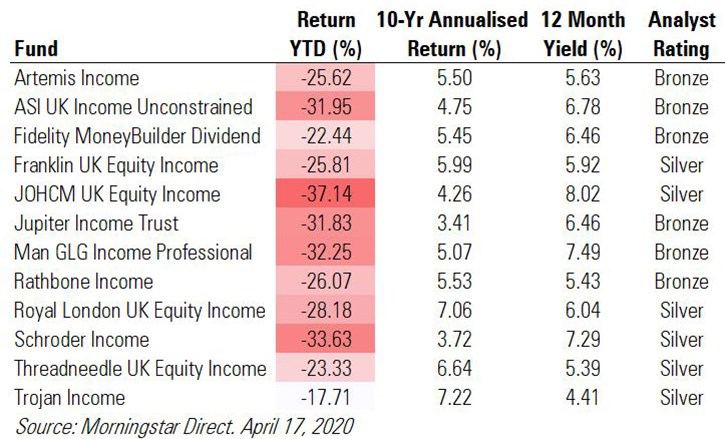

Few fund managers emerged unscathed from the March sell-off and those with an equity income remit are no exception. The sector was the second weakest Morningstar category in the first quarter, with funds in the group down an average of 28%; only UK mid-cap equity put in a worse performance (down 33%).

UK equity income managers have faced the double whammy of falling share prices for the companies they invest in and a loss of dividend income. Estimates by Link suggest total UK dividend income payouts will fall from £100 billion in 2019 to less than £50 billion in 2020. Already, banks have been forced by regulators to scrap their payouts and more companies are expected to cut dividends as the economic impact of the lockdown kicks in over the coming weeks and months.

Such is the extent of the problem, that trade body the Investment Association has relaxed the income requirement rules for these funds, so managers are not forced to take on more risk just to increase their yield.

So how will some of Morningstar’s highest rated fund managers adapt to this changed world, and where else do they find income?

We spoke to three managers of Silver-rated funds - Clive Beagles from JOHCM UK Equity Income, Richard Marwood of Royal London UK Equity Income Franklin and Franklin UK Equity Income's Colin Morton - about how they are tackling the income crisis.

1. Look Beyond Blue-Chips

Many fund managers, especially those with a global mandate, are now looking overseas for income. For those sticking with the UK, the key is to look beyond the obvious FTSE 100 names. Some two-thirds of this year's dividends are currently reliant on just 10 UK companies; investors relying only on these names are at risk of an income shock if they announce any dividend cuts.

Beagles and Marwood argue that it’s best to stick with you know rather than look abroad but impress the importance of diversifying beyond the obvious dividend payers.

“I’d much rather be digging around in some lesser-known UK small caps; we’re more likely to find underpriced stocks there,” says Beagles. Around 15% of the JOHCM UK Equity Income fund has a small-cap allocation and Royal London's Marwood is underweight the FTSE 100 and overweight the FTSE 250.

2. Pick Sectors That Will Re-open Faster

With most European countries still in lockdown, it’s hard for investors to second guess how and when these restrictions will be lifted. Beagles is tilting his portfolio towards companies in industries that he believe will be “first out” when normal life starts to resume.

He owns infrastructure firm Costain (COST); its share price has fallen sharply this year but the business has just signed a £3 billion deal to help build HS2, the UK Government’s flagship rail project.

Beagles also expects construction firms such as Vistry (VTY) – formerly Bovis Homes – to restart quicker than other industries as demand grows for new homes, especially social housing. The faster these companies get back up and running, the sooner dividend payments will resume.

3. Look for Unloved Stocks

The JOHCM fund holds WPP (WPP), the world’s largest ad company and one that has been hit hard by the travel ban and economic slump. WPP’s shares are off nearly 50% so far this year but Beagles is backing the company to make it through the current malaise, because of its dominant position and strong balance sheet. With a yield near 10%, narrow moat WPP is on to our list of top FTSE dividends.

The company has cancelled its share buyback programme and suspended its dividend, but Beagles thinks it will be much faster to restart payouts than, say, banks. Morningstar analysts rate WPP as a five-star stock, which means it is significantly undervalued.

Royal London’s Marwood, meanwhile, likes financial markets broker IG (IGG) because market volatility has been good for the firm; it shares are higher year to date, some feat in the current climate, and it’s currently yielding more than 6%.

4. Be Realistic

Very few dividends are currently considered “safe” at the moment so even a reduced income stream is better than none at all. For Marwood, “anything paid at the moment is reasonably attractive”. He points out that in this environment, a reduction in payout is better than a suspended or cancelled one. Imperial Tobacco (IMB) is one example of this; the company announced changes to its dividend policy last year. Marwood says: “The firm could cut its payout and still be paying a very handsome dividend”.

5. Consider the Reason for the Cut

Morton says it is important to distinguish between companies that have cut because they have to – retailers, banks, housebuilders – and those that are cutting for safety, to gain some breathing space while the crisis plays out.

Marwood points to companies such as Morrisons (MRW) and Sabre Insurance (SBRE), which have suspended special dividends but not touched their ordinary dividends, as examples of those which could easily switch back to normal when the situation improves.

6. Think About the Future

The immediate situation is tough for income fund managers. Morton says this is the most challenging period he’s faced as a fund manager, and the future path of a post-coronavirus recovery is unknown. But investors should take heart that many dividends have been suspended rather than cancelled outright, as it could mean companies can make it up to investors in better years.

Morton believes that some firms could come out the other side of this crisis in a better market position. Next (NXT), for example, will have fewer competitors as companies like Oasis and Debenhams go to the wall. And Marwood argues that the companies that don't cut and ride out this crisis, including big pharma like GlaxoSmithKline (GSK), AstraZeneca (AZN) - and possibly (RDSB) and BP (BP.) - will be more highly prized by investors in the years ahead.

.jpg)