The first quarter of 2020 was marked by the rapid escalation and globalisation of Covid-19 and its dramatic and tangibly negative impact on the global economy.

Plunging prices across bond sectors and even unheard-of liquidity strain in US Treasury markets have rattled bond investors’ nerves. In the initial weeks of the sell-off, reports of liquidity stress were everywhere.

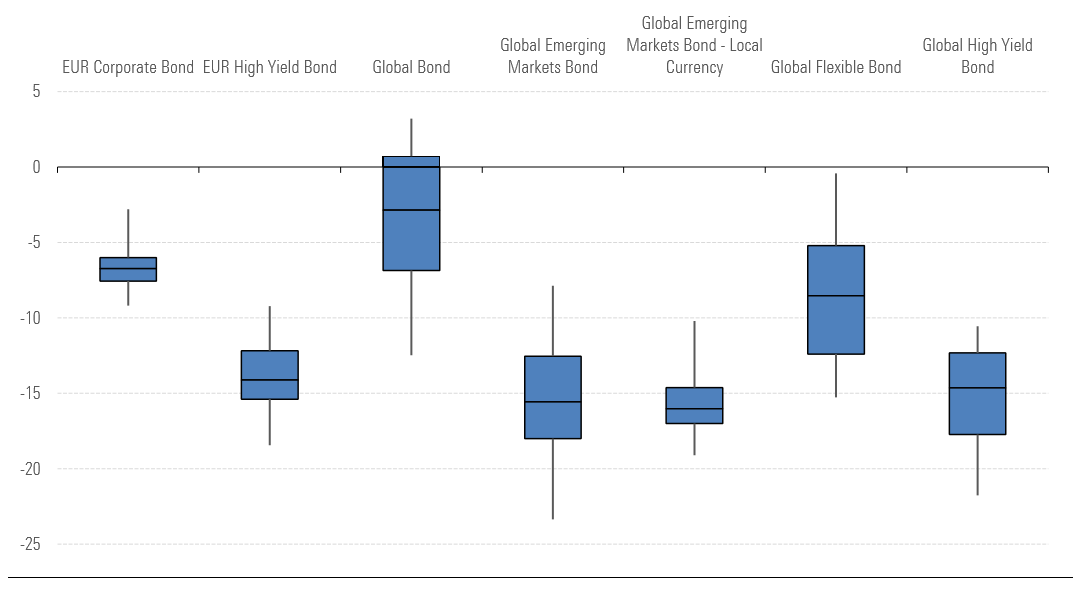

The chart below shows the range of performance across difference Morningstar fixed income categories.

The bond market’s most economically sensitive sectors, such as high-yield corporate bond funds, struggled the most over the first quarter of the year, posting double-digit losses on average. The Bloomberg Barclays Pan Euro High Yield Index was down 15% (in euro terms) in the three months to March 31.

Higher-quality parts of the market have not been spared, either: the investment-grade focused Bloomberg Barclays Euro Aggregate Corporate Bond Index posted a 6.5% loss for the year to date, with most funds in the EUR Corporate Bond Morningstar Category in the red. Sterling Corporate and High Yield bond funds followed suit, with most underperforming their benchmark in the sell-off.

For European investors, US Treasuries provided the safest haven during the turmoil, thanks in part to favourable exchange rates. The US Government Bond Morningstar Category has been by far the best performing group year to date, with double-digit gains (in euro terms).

UK Gilts also provided some relief for sterling investors, as 10-year Gilt yields fell from around 0.8% to 0.23% at their lowest. The average fund in the GBP Government Bond category returned almost 7% in the first three months of the year. Index-linked gilts produced more modest returns (an average of 3.7%) but were still comfortably in positive territory.

There have been some dizzying turns for global fixed income investors, meanwhile. Yields on the traditional safe haven assets of German and Japanese 10-year government bonds fell in tandem with US 10-year Treasuries as the equities sell-off got underway.

The currency market has also seen ample volatility; the Japanese yen and Swiss France have come along for the ride with the US dollar, surging versus most currencies. Conversely, the oil price slide has put pressure on other currencies including the Canadian dollar, Norwegian krone, and Russian ruble.

Dedicated emerging market bond funds have been among the hardest in the fixed income universe, with an average loss of 14.1% year to date, because of steep price declines on both rates and currencies.

So how have fixed income funds against this backdrop? We look at some of the best and worst performers.

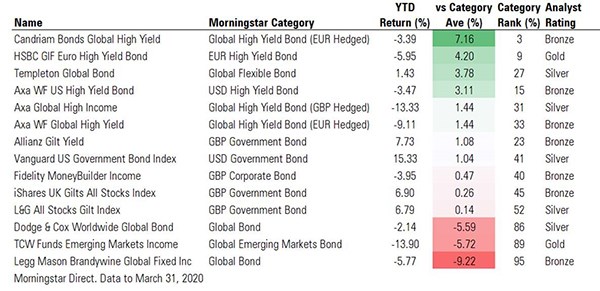

Top Performing Bond Funds

Within European high-yield bond funds, some have weathered the recent storm better than others. The Gold-Rated HSBC GIF Euro High Yield Bond and Bronze-Rated Candriam Bonds Global High Yield funds, whose portfolios have long features companies with better profitability and lower debt compared with peers, significantly limited losses compared with their counterparts.

Meanwhile, the team behind the Axa WF US High Yield Bond, Axa WF Global High Yield and Axa Global High Income funds also protected investors’ capital better than their average peers, thanks to the decision to underweight the energy sector.

Within euro- and sterling-denominated investment grade bonds, a lot of the portfolio managers began 2020 fairly defensively positioned, as valuations had been getting less attractive. Silver-Rated Fidelity MoneyBuilder Income held up better than its peers as its managers came into the crisis with an overweighting to defensive sectors such as utilities.

Elsewhere, global bond managers with the flexibility to deviate from the index also managed to limit losses. Silver-rated Templeton Global Bond, which focuses on global sovereign bonds and currencies, has help up better than most thanks to its investments in the Japanese yen and Swiss franc, a short on the Australian dollar, and double-digit cash stake.

Within US and UK Government Bonds, passive funds have outshone active managers in the downturn. That’s easily explained by their long average duration, compared to most active managers who had taken a more conservative stance on rates. Vanguard US Government Bond Index Fund, rated Silver, tops its category’s ranking over the period, while Bronze-rated L&G All Stocks Gilt Index and iShares UK Gilts All Stocks Index have outperformed their peers. Once exception, is the actively managed Allianz Gilt Yield fund, rated Bronze, which outperformed its category average by more than 2 percentage points.

Worst Performing Bond Funds

Unfortunately, some bond funds are more vulnerable than others in a liquidity crunch. As yields on high-quality bonds had been near historic lows for years following the global financial crisis, some fund managers were tempted to reach for yield by venturing into riskier, less liquid segments of the market.

Neutral-rated GAM Star Credit Opportunities was down 14.3% in the first quarter; it invests exclusively in subordinated debt issued by financial and non-financial companies, an area of the market which sold off by about 30% at its worst point. The managers have stayed the course, however, and argue the global financial sector is more robust than its was during the financial crisis.

Global strategies with higher exposure to emerging market debt have mostly suffered as well. Silver-rated Dodge & Cox Worldwide Global Bond, for example, has a healthy stake in corporates and emerging market bonds , which caused it to trail its category index by more than 8 percentage points in the first quarter.

Legg Mason Brandywine Global Fixed Income fell by 11.8% in dollar terms, underperforming its peer group average by 12.3 percentage points. At the end of February, the managers had maintained a position in Brazil and in Mexican sovereign debt as well as the peso, while having a negative view on the US dollar. The team’s contrarian calls have overall led to a volatile record for the fund, but the approach has rewarded patient investors, warranting its Bronze rating.

Within dedicated emerging markets bond funds, TCW Funds Emerging Markets Income, rated Gold, was one of the starkest underperformers, plunging 16.7% in the first quarter. This was partly due to its focus on Middle Eastern bonds, which have suffered from their oil dependence, as well as an overweight to Ukraine and some hard-hit corporates.