The start of a new tax year is a good time for savers and investors to look at their finances and find areas to improve. Whatever form that my take – using your full Isa allowance or starting a pension – people often feel they need professional help to guide them through the process.

But many people hesitate before taking financial advice because they think they aren’t rich enough to warrant it. Indeed, it's not always cost effective to pay for advice; if you plan to invest £5,000 in an Isa, paying an adviser a one-off £500 fee to tell you what funds to invest in is too much of a chunk of money to justify.

This reluctance to seek face-to-face advice is widespread among those who are starting their investing journey and have limited wealth but still need guidance. To fill that gap, robo-advice has sprung up and become increasingly popular in recent years, with costs all the time as competition intensifies.

Law firm Michelmores interviewed millennials (people born between 1981 and 1996) with investable assets above £25,000 and found that 53% would rather take robo-advice than face-to-face advice; and that percentage is even higher (61%) among individuals with £75,000 or more to invest.

“Affluent millennials are increasingly comfortable using technology to manage their money, believing that it gives them a greater degree of control than using other investment management methods,” says Michelmores private wealth partner, Richard Cobb.

Enter Vanguard

US passive fund giant Vanguard has just received regulatory approval to offer a consumer advice service in the UK. While it has yet to launch the service, judging by the response to its low-cost Sipp - the cheapest pension in UK market - it is likely to set the agenda.

Consultancy the langcat thinks the launch, when it comes, will be significant: "It’s early days but we’re keen to see how this pans out. Two things are sure: one, Vanguard knows how to disrupt the industry (in a good way), and two, it’ll be cheap."

Two high street names offer robo-advice: Santander and HSBC, the latter of which intensified competition in October by lowering the minimum amount customers can invest to £50 a month.

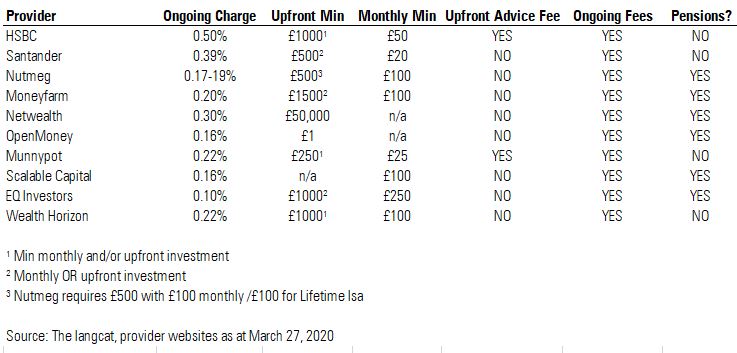

Using data from the langcat, we have put together a table of the main robo advice providers. In order to focus on pure robo-advice rather than other solutions, we have excluded some of the automated investment services on the market, for example, accounts that “round up” your balances and payments and put the remaining money in a savings account or stocks & shares Isa – such as Moneybox, Chip. And we have excluded those who provide ready-made portfolios without advice, such as Wealthify.

All of the companies on the list are protected under the Financial Services Compensation Scheme (FSCS), meaning your money is covered if the provider goes bust.

As with fund platforms, making an exact like-for-like comparison between providers is not always easy even though each of these give a full breakdown of charges online. Every provider has a slightly difference approach to charges and describing them.

Key Findings

1) There are so many different ways to describe ongoing charges: whether they are "platform", "monitoring", "digital advice", "trading", or "fund" fees. These also include custody, admin costs etc, and overall these come in below 1% in most cases. Investors must do their best to read the small print and understand what they are paying.

2) Minimum monthly contributions range from £20 to £250, although most are £100 and below. Some providers stipulate a minimum lump-sum as well as a minimum monthly investment.

3) The minimum lump-sum investment varies more significantly: Open Money sets £1 as the minimum, whereas NetWealth asks for £50,000.

3) HSBC and Munnypot charge their advice fees upfront, whereas the rest bundle the cost of advice into ongoing fees.

4) Most providers offer pensions as well as Isas. Our research focuses on Isas, however.

5) Some providers allow you to cross over into human interaction - Scalable Capital doesn't offer financial advice as a default, but you can apply to speak to an adviser in person or on the phone for a flat fee. Santander allows you to upgrade to a speak to a financial adviser if you have a mnimum of £20,000 to invest.

6) Most offer Isas and non-Isa general investing accounts. These aren't "whole of market" in that you can't pick and choose your funds like you would with an investment platform. For example, Santander offers four multi-index funds and Scalable Capital offers ETFs only. Nutmeg offers three default options, two of which are "proactively managed by experts".

Guidance website Boring Money also points out that the investment propositions often vary greatly across the platforms, as does the performance. It has run a number of "test portfolios" over two years, investing £500 across a number of robo-advice sites to see the effect of charges and performance. One of the companies on our list, Moneyfarm, is the second best performer in Boring Money's analysis - using the site, £500 grew more than 10% to £554 in the two years to the end of January.

"The contributing factors to any relative and short-term underperformance were charging structures, fees and asset allocation," says Boring Money chief executive, Holly Mackay. She says many of these "ready-made portfolios" have very different equity exposures; higher exposure to the stock market would have been better during the bull run of recent years but would have been hit harder in the recent sell-off.

Robo vs Face-to-Face Advice

The argument in favour of robo-advice is that it is “wealth management lite” for those starting out on their investment journey; these customers will then (some providers hope) upgrade to full financial advice once their assets grow or needs become more complex, for example, when they have children, buy a house or receive an inheritance windfall.

The argument against robo-advice is that people’s financial lives often don’t fit into the neat categories offered online and at a certain point it might be better to go and see an adviser. It is also worth bearing in mind, that often it is not all that cheap to use a robo-adviser, with some sites charging upwards of 1%.

Michelmores says the move online hasn’t been driven by a distrust for the advice profession – four-fifths of those surveyed still trusted traditional advisers. Instead it is the sophistication of technology and the convenience factor encouraging more people to use their phone to handle their finances.

Peter Chadborn, director of adviser firm Plan Money, thinks both robo and traditional advice have a role to play in modern financial planning - and that younger people taking automated advice can become the face-to-face customers of the future. One aspect of face-to-face advice that robo can't replicate, he says, is empathy and reassurance, particularly when a client has to make an once-in-a-lifetime decision such as: can I afford to retire? He also understands why some people "go robo" for investments but prefer human contact for financial planning.

The langcat likes robo firms that offer some financial advice, even if it is restricted to a provider’s products, because it opens up the possibility of recourse: “Advice is good, becuause if it ends up being wrong you might be able to claim against the provider.” The firm also recommends investing with a robo-adviser that is covered by the Financial Services Compensation Scheme (FSCS) as that will pay out up to £85,000 if the provider goes under. For those looking to invest with a well-respected brand, the langcat recommends Santander and Nutmeg. And for those looking for a low-cost option, it prefers OpenMoney.