It's difficult for a fund to top the performance tables year in, year out but some seem to suffer more drastic swings than others.

We have previously looked at funds that went from worst to first - those which managed to turn their performance around from being the weakest performer in their category in 2018 to top of the group the following year.

But Morningstar data shows that just as many funds suffered the reverse - a fall from grace from top of the pile in 2018 to bottom of the pack in 2019. Here we look at three of the funds that went from first to worst:

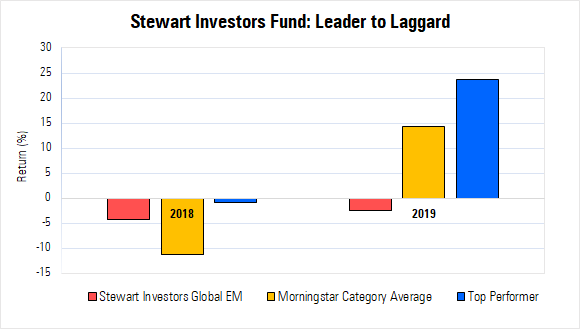

Stewart Investors Global Emerging Markets

Our analysis focused on funds that were in the top decile of performers within their Morningstar category in 2018 and then fell to the bottom decile the following year. One fund that suffered this fate is three-star rated Stewart Investors Global Emerging Markets, which dropped from the top 5% of performers in its Morningstar category, Global Emerging Markets Equity, in 2018 to bottom place in 2019.

While returns in both years were negative, when we compare the fund's performance to its peers the situation becomes clearer. Stewart Investors Global Emerging Markets was down 4.31% in 2018, but it was a bad year for emerging markets as the dollar strengthened and the trade war between the US and China kicked off. The average fund in the category was down 11.31% - meaning this fund actually outperformed by 7 percentage points, putting it in the top 5% of performers in the group for the year.

But 2019 saw a stark turnaround in fortunes. While performance was better in absolute returns - the fund was down 2.51% in the year - it underperformed the category average by a staggering 16.9 percentage points, putting it at the bottom of the group in performance terms for the year.

There are myriad reasons a fund may underperform its peers and one bad year is not necessarily a signal to sell. “Performance can be driven by a number of factors including a manager’s style, skill or luck or a combination of these factors,” says Emma Morgan, portfolio manager at Morningstar.

A major factor for the Stewart fund was a change of management. Manager Ashish Swarup resigned in September 2019 and the fund saw assets under management fall after his departure. Tom Prew took over as lead manager of the fund and performance suffered as he grappled with outflows. Morningstar analyst Andrew Daniels says that while the loss of Swarup was disappointing, he has high confidence in Prew and the broader team, however.

Of the 47 companies in the fund's porfolio the main detractors on performance came from those in the consumer defensive sector, which account for almost half of assets. Investments in Unilever (ULVR), the maker of Dove soap and Ben & Jerry’s ice cream, Marico (MARICO), the Indian leading consumer goods, and Vitasoy (HKD), the producer of popular Asian soy drinks, were among the weakest in the year.

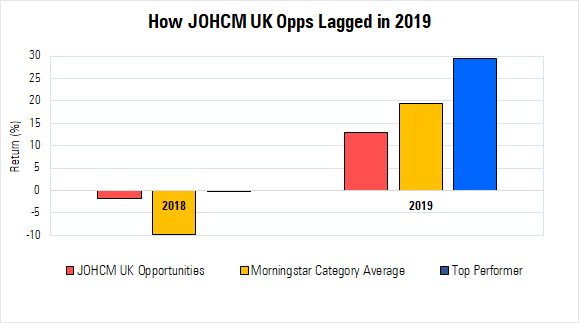

J O Hambro UK Opportunities fund

The four-star rated J O Hambro UK Opportunities fund dropped from the top 2% of performers in the UK Large-Cap Equity category in 2018, to the bottom 4% of performers in 2019.

A major drag on performance was the fact that almost a quarter of the fund's assets are currently held in cash, which meant it missed out on the so-called Boris Bounce following the General Election at the end of the year. Indeed, it was a good year generally for domestic UK companies and value stocks, which came back into favour as investors turned more risk-on having been some clarity over Brexit.

The fund turned in a respectable return of 13% for the year, but it fell way behind many of its peers, underperforming the category by 6.3 percentage points. In comparison, the four-star L&G Ethical fund was up 29.4% in 2019 and the three-star rated Santander UK Equities 24.1%.

It was a stark turnaround from the previous year when, despite being down 1.85%, the JO Hambro UK Opportunities fund outperformed its category by 8 percentage points. But Morningstar's Morgan says performance is only one of the factors investors should assess when choosing a fund.

When it comes to selecting funds, she says investors need to assess the people managing the fund, their philosophy and process, as well as the fees. “This should give you a good understanding of the expected returns over different periods of time," she adds. "If a fund has performed in line with your expectations and nothing has changed regarding the people, process or philosophy, then you should absolutely hold onto it."

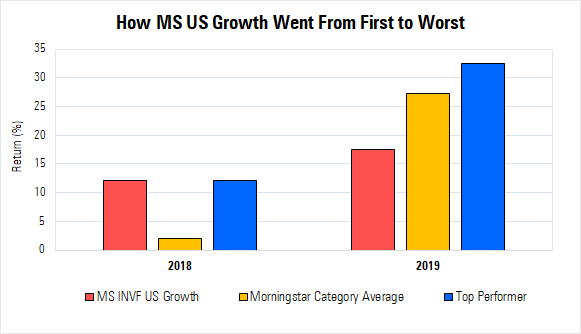

Morgan Stanley US Growth

The four-star rated Morgan Stanley US Growth fund was another which fell from grace in 2019. In 2018, the fund was among the top 3% of performers in the Morningstar US Large-Cap Growth Equity category, but last year found itself among the bottom 4% of the group.

But the fund is another example of the importance of comparing performance to rivals and the category, not just looking at the standalone figure - because few investors would likely be disappointed with the 17.6% return the fund clocked up in 2019, until they looked at what the rest of the category achieved.

Indeed, with an average return of 27.3% the fund underperformed its category by 9.7 percentage points. Among the top performers of the category for the year were the four-star rated UBS US Growth and Brown Advisory US Sustainable Growth, which were up 32.5% and 30.5% respectively.

The fund, which has been managed by Dennis Lynch since 1997, has a fairly concentrated portfolio of 42 holdings. While many technology stocks have soared in recent years, the main detractor to the fund's performance in the year was social media outfit Twitter (TWTR) whose shares tumbled 22.2% in 2019. Accounting for almost 5% of the fund's assets, this proved a major drag on performance.

Meanwhile its rival UBS fund enjoyed gains from its big bets elsewhere in the tech sector. Apple (AAPL) and Microsoft (MSFT) account for 5.9% and 9.6% of its assets respectively and their shares climbed 22.3% and 5.9% during the year. Neither of these stocks feature in the top 10 holdings of the Morgan Stanley fund, by contrast.