Investors have traditionally used equities and bonds to serve two different functions in their portfolios: they invest in companies’ equity to capture the growth of the economy, and in bonds to provide a steady income in the form of coupon payments.

Traditional wisdom when investing your pension is to start with your portfolio almost entirely in equities, which will grow in value throughout one’s career. Over the long run, the average return on equities is roughly 10% a year, while bonds return on average 5%.

As you approach retirement, you gradually shift your portfolio from equities to bonds in order to protect the value of your pension pot and ensure a steady income stream once you retire. But while bonds still provide a defensive way to preserve capital value, does the adage that equities are for growth, and bonds for income, hold true in the current economic environment?

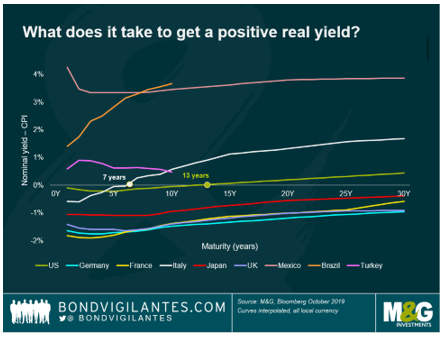

Not in Germany, France, Japan and the UK, where real yields on government bonds (which we’ve calculated as nominal yield minus the CPI rate of inflation – currently 1.7%) are negative even up to 30 years – see the chart below. Years of securities purchases under central banks’ quantitative easing programmes, along with seemingly low growth in the world’s core economies, has led to continued downward pressure on bond yields. We have seen significant yield compression even on government bonds in peripheral European countries such as Italy. Investors must lend to Italy for as many as seven years just to get a positive real yield.

Those who think of bonds as the boring, income-generating part of their portfolio need to think again: some of these bonds come with no income at all.

But fixed income has always been a relative game. Investors must look between cash, government bonds and corporate bonds to find the best relative value. While for some investors, this choice has led to more the decision to hold more cash in their portfolio, others have become tourists into riskier assets.

Faced with negative yields across core government bond curves (with the notable exception of the US), no wonder some investors have decided to look to lower credit quality assets away from their comfort zone in search of yield. Those who invested in government bonds have moved to investment grade, upper investment grade to BBBs, and BBBs to high yield. Many investors are also looking to emerging markets in search of better fundamental value.

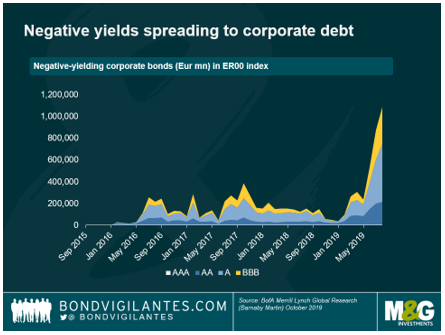

One worry is that when volatility next picks up in fixed income markets, these tourists in unfamiliar asset classes will want out at any price. As investors shift back up the quality spectrum, we may see significant price action in risk assets. Another effect of this tourism into credit is that it means that negative yields spread: as more investors buy credit, risk premia compress and bonds which were once attractive for their income no longer provide any at all. The full extent of this is surprising – see the chart below.

Partly an effect of ECB buying, partly of this credit tourism, now more than €1trillion of corporate bonds in the ER00 European corporates index are negative yielding. In fact, all of the bonds of some issuers now have negative yields: the basic industry sector leads the way, with 25% of issuers having totally negative-yielding curves, followed by capital goods (23%) and banking and autos (both 22%). Most of this negative-yielding corporate debt is actually in the lower end of investment grade, namely A and BBB-rated. Seen in this light, the “equities for growth, bonds for income” adage is reversed. Dividend-yielding equities provide income – indeed, the FTSE 100 currently yields around 4.5% - while these negative-yielding government and corporate bonds do not.

So, how should investors think about fixed income in this previously unknown environment? Even if these bonds provide no income, they can still provide capital growth. With central banks cutting interest rates, owning duration has been the trade of the year so far. Negative real yielding bunds, French OATs and gilts have all posted positive total returns year to date.

What about next year? The current environment of more modest inflation, with few visible green shoots of growth in core developed economies, is supportive for bonds. Aided by central banks’ quantitative easing programmes, continued buying of government and corporate bonds squeezes yields down and boosts their capital value. And bonds love bad news. Any “risk off” sentiment resulting from deterioration in global politics and the economy would further support this downward pressure on bond yields.

On the other hand, one big risk to this trade is the possibility of further government bond issuance by populist leaders – think Jeremy Corbyn and Democrat frontrunner Elizabeth Warren. Their spending promises are unlikely to be funded fully by planned tax increases, so probably mean more bond issuance. As with any resource, an increase in supply pushes prices down.

Whatever happens next year, in this strange new world of low and now negative yields, investors need to take a more active approach and not rely on conventional wisdom which doesn’t hold true in a post-QE world. For many investors in 2019, equities were for income, and bonds for growth.