In my previous article on how actively managed funds belonging to the 3 main equity categories (Europe Large Cap Blend Equity, USA Large Cap Blend Equity and Global Large Cap Blend Equity) behaved in a bear market environment, the conclusion I drew was blunt: in the first five months of 2022, the average performance of the funds in these three categories had been lower than a representative exchange-traded fund.

For the individual investor, the lesson could be the following: why waste time selecting an actively managed fund if, even in a bear market (where actively managed funds are supposed to have an advantage over passively managed funds), they fail to beat an ETF (we leave aside any tax considerations in the article).

But, to be honest, the study has a major methodological flaw. It assumes all mutual funds, which make up the average of the categories analysed, are actively managed. This is not true. The universe of funds in any given category is subdivided into three groups: index funds, what we will call miscategorised funds, "true" actively managed funds and "false" actively managed funds.

Index Funds: a Significant Percentage

With regard to index funds, their number is not as insignificant as one might think, especially in view of the great onset of passive management in recent years and especially in the three categories analyzed (index funds tend to be concentrated especially in these 3 categories).

The below graph shows the importance of index funds in the three categories. In the case of the USA Large Cap Blend Equity funds, the percentage of index funds reaches 22% and cannot be considered irrelevant. Therefore, it is advisable to eliminate index funds from the performance analysis.

Funds wrongly categorized?

Within each category, and especially in the categories where the segmentation is made according to the investment style, there are a certain number of funds that do not strictly fit within the parameters of that category.

For example, it is possible to find within the Europe Large Cap Blend Equity category, a fund that has a Style Box (the Style Box is that little box that indicates at a glance the investment style of a fund) marked as Large Value or Large Growth.

This is not a problem per se. Funds are not static. Their portfolio can and does vary over time, especially in times like today where style differences (between value and growth) can be very marked.

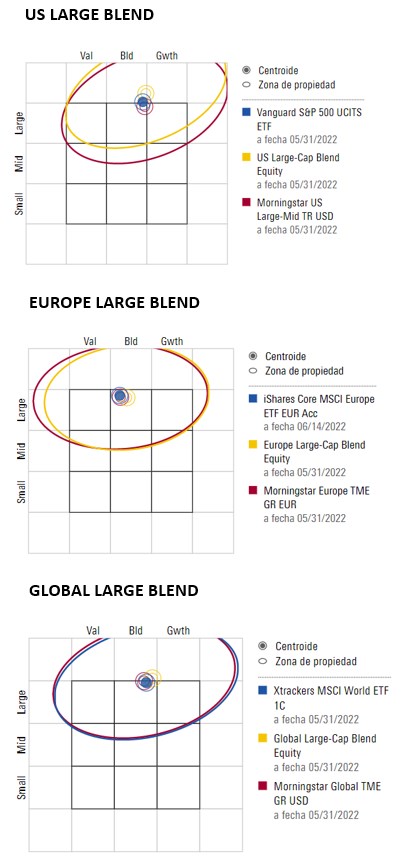

Nor is it a categorization problem. We do not automatically change the fund's category because its Style Box has changed from one month to the next from Large Blend to Large Value or Large Growth. In any case, if we compare the ETFs we chose in the first article (one for the Europe Large Blend Equity category, one for the USA Large Blend Equity category and one for the Global Large Blend Equity category), we see, as the attached illustration shows, that in terms of investment style there are few differences between these ETFs and the average of their respective categories.

Separating the true active funds

The most relevant problem when analyzing the performance of active funds versus passive funds is that within the supposedly active funds there are funds that are very tied to the benchmark, but charge fees as if their management were truly active. These are known as closet indexers.

Now, how do you separate these false active funds from the true active funds? What I have done is to calculate the tracking error of all the funds of the 3 categories. The tracking error simply measures how well the fund tracks the benchmark over a given investment period. It is a measure of the volatility of the return differences between the fund and its benchmark. A small tracking error indicates that the fund is very close to its benchmark, while a large tracking error indicates the opposite.

For the 3 categories analyzed, we have subdivided the funds’ universe (excluding index funds) into 4 quartiles: funds with a high 3-year tracking error (true active funds - Quartile 1), funds with a medium-high 3-year tracking error (Quartile 2), funds with a medium-low 3-year tracking error (Quartile 3) and funds with a low 3-year tracking error (closet indexers - Quartile 4).

We have also included in the comparison the funds that obtain a positive Analyst Rating (Bronze, Silver or Gold) in each of the 3 categories.

For each group we have calculated the average return obtained from January to May. These are the results:

Conclusions

There are several conclusions to be drawn from this study.

First, the fact that a fund is very active (Quartile 1) does not guarantee that it will perform better in market declines. In general, in the 3 categories analyzed, the group of funds with the lowest tracking error has done better than the average of the other funds.

Second, it is striking that the funds with a positive qualitative rating from Morningstar analysts outperformed the average actively managed fund and even the benchmark ETF in the US Large Blend Equity and Global Large Blend Equity categories.

It may be fortuitous, but it should also be noted that our analysts positively value aspects such as a low portfolio turnover, a strong conviction in the strategy’s implementation, the fund’s performance in both up and down markets and low costs, all of which may explain the relative outperformance of this funds’ group in a difficult market environment.