Chinese real estate developer China Evergrande Group (03333) is on the verge of defaulting on its massive US$ 300 billion bond complex, even as hopes for a bailout program by the central government are muted. Investors are worried, both about the default, and the possible ripple effects on other parts of the economy, such as banks.

In the fixed income market, the overall bond ownership in China Evergrande Group in dollar terms fell, largely because of the fall in the market value of the bond complex. Patrick Ge, manager research analyst at Morningstar, saw a mixed attitude among bond managers to buy the dip.

“We’ve seen a few funds adding to China Evergrande between July and August 2021, given widening spreads and attractive valuations. This is in line with what we have heard from some managers where they said that at its current levels, they believe Evergrande is a buy,” Ge says.

Morningstar Direct data shows that UBS, HSBC and Blackrock have been accumulating Evergrande bonds. Number of shares increased, though the total exposure is on the decline.

Source: Morningstar Direct

Are Opportunities Emerging?

BlackRock’s portfolio saw a net addition of 31.3 million shares in Evergrande issues between January and August 2021. That said, the overall impact on the portfolio is a smaller position due to a fall in the bond’s market value. The fund holds 1% of its portfolio assets in China Evergrande Group, a level higher than the 0.5% weighting in the JP Morgan Asian Credit Index.

Between January and July, HSBC added 40% more in Evergrande bond shares, but total portfolio exposure is down to 1.22%. UBS’ latest available data was as of the end of May. Its Asian high yield bond fund trimmed 0.09 percentage point of exposure to Evergrande, but the number of total shares rose 25% year-to-May.

However, the turnaround story and cheapened valuations aren’t for everyone. Morningstar Direct data shows that Fidelity, PIMCO and Allianz are net-sellers of Evergrande bonds between January and July, owning 3%-47% less bond shares.

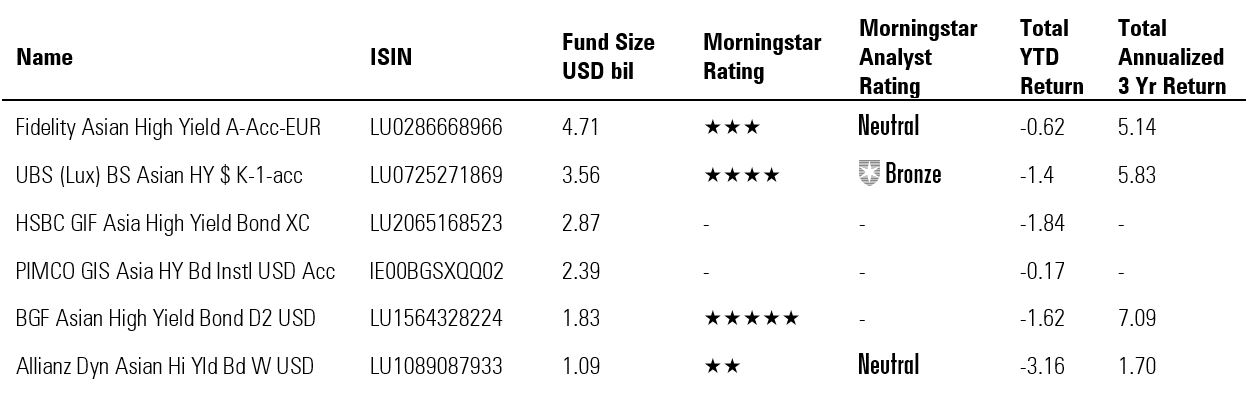

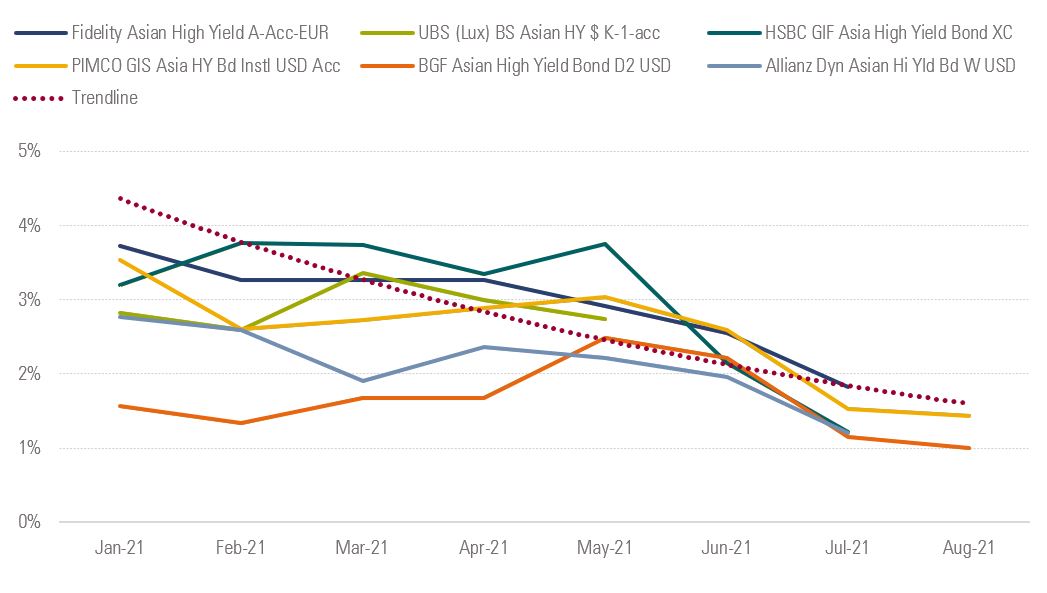

Six Largest Asian High Yield Funds’ Exposure to China Evergrande's Bonds

Total exposure to the indebted developer is on the decline

Source: Morningstar Direct

Ge notes that portfolio managers also look to play with smaller property bond names that have been dragged by the negative sentiment.

Bailout Isn’t a Given

He reminds investors that the situation continues to evolve. Investors should not take for granted that a government rescue package, such as the one granted to Huarong Asset Management, is a given in the case of Evergrande.

It is not an apples-to-apples comparison for two reasons, Ge says: “Evergrande is primarily a property development firm, with small exposures to businesses like electric vehicles. Its bonds are ultimately high yield issues. As comparison, Huarong is a financial institution and issues bonds that were rated investment grade. Due to their innate differences, the government’s reactions to a default scenario may differ, too.”

In the eyes of the Chinese government, Huarong portfolios of non-performing loans is said to carry ‘systemic risks’ that would threaten the wider Chinese financial system. Based on his conversation with bond portfolio managers, Ge notes that in the case of Evergrande’s fallout, the government may not hand out a bail-out program.

Three Red Lines

The Evergrande episode collides with credit tightening measures announced last year. China's ’Three Red Lines’ policy is designed as a state-wide initiative to manage systemic risks stemming from the indebted property development sector, which accounts for almost one-third of the country’s economic output.

The rule, enacted from mid-2020, uses three thresholds to evaluate a real estate developer’s gearing situation to determine its borrowing level for the following year:

- a 70% ceiling on liabilities to assets, excluding advance proceeds from projects sold on contract,

- a 100% cap on net debt to equity,

- a cash to short-term borrowing ratio of at least one.

Even if a firm passes all the requirements, it can only borrow an additional 15% in debt volume the next year.