Individual savings accounts (Isa) are an ideal way for investors to work towards their financial goals. Currently, investors can contribute up to £20,000 each year, invest the money in a range of financial instruments, such as individual stocks, bonds, mutual funds and exchange-traded funds (ETFs) and watch their money grow tax-free.

But how to invest your money? A crucial first step in building a portfolio is to determine your risk tolerance. Riskier investments such as stocks have historically shown better potential for long-term growth but can result in greater drawdowns at times of market volatility. Meanwhile, high-quality government and corporate bonds are better suited to protect during market volatility, but less likely to deliver strong returns over the long-term.

For the average Isa investor with a moderate risk tolerance, using passive funds – also known as tracker funds – to build a portfolio that strike a balance between capital preservation and growth can be a good option. Dividing assets between stock and bond ETFs can protect from unfavourable market movements in the short-term while offering good long-term growth potential.

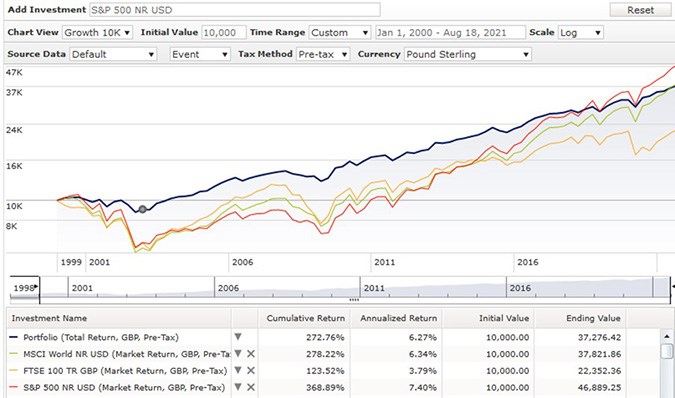

A very simple balanced portfolio split 50/50 between two global stock and bond ETFs has delivered higher returns than key equity market indices such as MSCI World or FTSE 100 over the past twenty years through July 2021. In fact, even the phenomenal bull run of the S&P 500 since 2009 would have only placed the US equity index marginally above the returns delivered by the 50/50 portfolio (see exhibit 1). The real benefit of diversification has been to protect to the downside, something that was particularly evident during the early 2000s tech crash and the financial crisis in 2008.

Exhibit 1: 50/50 equity/bond portfolio

The portfolio’s ability to shelter capital has come to the fore once again during the current market volatility caused by Covid-19. As the FTSE 100 and the S&P 500 plummeted by around 30% and 15% respectively in a matter of weeks, this balanced investment strategy limited the fall to just 10% (see exhibit 2).

Exhibit 2: 50/50 equity/bond portfolio

So here’s a three-step guide to building and monitoring this simple ETF portfolio

Step One: Pick Your Equity ETF

For the equity allocation, investors can consider the Vanguard FTSE Developed World ETF (VEVE) or L&G Global Equity ETF (LGGG). They are broad and diversified ETFs covering nearly every developed country stock. With an ongoing charge of just 0.12% and 0.10%, respectively, they are the lowest amongst passive peers and certainly very competitive relative to the average active fund in the category. Currently, the US accounts for 60-65% of the index, followed by Japan (7-10%), the UK (4-7%), and Canada (3-5%).

They also offer balanced sector exposure. Accounting for a quarter of the total weight, technology is the fund’s largest sector exposure, followed by financials and consumer discretionary (10-15% each) and healthcare (8-12%). Portfolio concentration is very limited, with the top 10 holdings accounting for around 18% of the indexes value.

Step Two: Pick Your Bond ETF

For the bond allocation, investors can opt for the SPDR Global Aggregate Bond ETF (SPFB) or iShares Core Global Aggregate Bond UCITS ETF (AGBP). Both track the Bloomberg Barclays Global Aggregate Bond Index and come with an ongoing charge of 0.10%. Holdings include a broad range of investment-grade government, supranational, corporate and securitised bonds from a large number of developed and emerging economies. Both ETFs also come with the advantage of a hedge to GBP, which can help mitigate the impact of short-term currency movements.

Most holdings are government bonds (55-60%), followed by bonds issued by government-sponsored agencies (10-15%). The remainder is split by the likes of corporate bonds, mortgage-backed securities and local authority bonds. US issuers accounts for around 40% of the index, with a large presence of US Treasuries. Japan follows with just under 15%. France, Germany and the UK account for around 5% each. The combined weight of emerging market issuers is 10%.

Step Three: Rebalance

Rebalancing the portfolio in order to keep the targeted 50/50 allocation is very important because it helps to control risk. This requires selling investments from the ETF that has outperformed and reinvesting the proceeds into the ETF that has underperformed. Typically, in periods of strong market performance, the weight of the equity ETF will grow larger, while in times of crisis its value will drop.

Failing to rebalance is likely to result in increased risk if the equity allocation’s weight increase, or limited returns if the weight of the bond allocation goes too high. However, this must not be done too frequently as you would incur high trading costs. For the average investor, sticking to a simple 10% buffer will likely suffice. This means that once the weight of one ETFs is 10% over the desired 50% allocation, they should be brought back to an equal weight.