The world is finally starting to look different to 2020. With a reopening economy, booming stock markets and a whole lot of talk about inflation, fund performance has been affected by investors’ appetite for risk.

So, we have taken a look at the funds that have gone from the top of the pile to the bottom in a short period of time.

Data from Morningstar Direct shows that 15 funds from several Morningstar categories have fallen from the top decile of their category in 2020, down to the bottom 10% in 2021 year to date. Of the 15, there were two GBP Corporate Bond funds, two from Global Emerging Markets Equity and two from UK Equity Income – the rest varied from small- to large-cap equities and infrastructure.

When narrowing the data even further, looking at the top and bottom 5%, six UK funds made the dramatic drop. These funds include both equities and bonds, and UK, US and Japan markets.

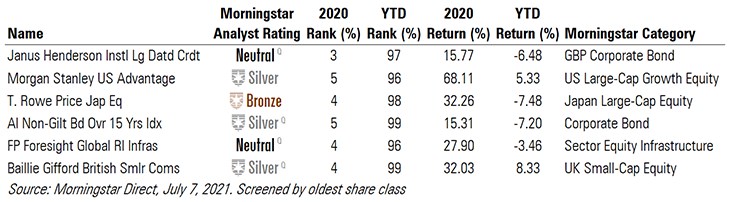

Janus Henderson Institutional Long Dated Credit

The Long Dated Credit fund fell from the top 3% in the GBP Corporate Bond category in 2020 to the bottom 97%. So far this year, it has returned a negative 6.48% - significantly lower than its last annual return of 15.77%.

Despite strong figures last year, and a Morningstar Rating of 5 stars, Janus Henderson’s credit fund has a Morningstar Quantitative Rating (MQR) of Neutral. This is due to a weak portfolio-management team, lower-than-average team retention and below-average processes. An analysis of the portfolio has also revealed a significant overweight position in A-rated bonds and an underweight in debt with a 10- to 15-year maturities when compared with its peers. However, the fund has a strong risk-adjusted track record, and has achieved an annualised return of 7.50% over the past three years.

Morgan Stanley Funds US Advantage

The US Large-Cap Growth Equity fund fell from the fifth percentile in 2020, with an impressive 68.11% return, to the 96th percentile and a muted 5.33% return so far this year. It holds an Analyst Rating of Silver, with a Gold-rated share class available, and has a 4-star rating.

Morningstar’s Katie Rushkewicz Reichart believes US Advantage’s investment team to be best-in-class. Dennis Lynch has led the 16-people team for 22 years, with no departures since 2011, and aims to invest in the best opportunities in the market. It currently holds 38 stocks, although unlike its peers, none of these are the classic Apple, Microsoft or Google. Rather, its holdings include Shopify (SHOP), Twitter (TWTR), Twilio (TWLO) and Square (SQ), and most fall under the growth umbrella.

While its strategy has paid off in 2020, the latest returns, alongside the Morningstar risk model analysis, has hinted that its exposure to momentum and volatility means investors should manage their expectations. Its three-year annualised return is an impressive 25.88% and the fund was the fourth best performing fund covered by Morningstar last year.

T. Rowe Price Funds OEIC Japanese Equity

This Bronze-rated fund saw its returns turn from 32.26% in 2020 to -7.48% year to date. This meant a fall from the fourth percentile in its Japan Large-Cap Equity category, to the 98th, but due to its past performance it is rated as 5 stars. Its annualised returns over the past three years stand at 10.02%.

According to our analyst Ronald van Genderen, fund manager Archibald Ciganer targets companies that can deliver growth in shareholder value, with three fourths of the portfolio consisting of companies able to achieve and sustain above-average, long-term earnings while being on the right side of transformation – holding quality-growth stocks like SoftBank (9434), Hoshizaki (6465) and Suzuki Motor (7269). Genderen says: “The portfolio is constructed from the bottom up and little attention is paid to the benchmark in portfolio construction, aside from ensuring that each position is active.”

AI Non-Gilt Bond Over 15 Years Index

The Aviva fund also sits in the GBP Corporate bond category, together with Janus Henderson’s. It saw a flip from fifth percentile to the 99th, returning 15.31% over 2020. But, six months into 2021, it has lost 7.20%.

According to Morningstar, the fund has a sensible investment process, compensating for having no named managers. It has achieved a MQR rating of Silver by being cheaper than its peers, with an annualised return of 7.71% over three years. It invests in permitted money-market instruments, deposits and units in collective investment schemes, ETFs, and derivatives and forward transactions. Due to its successful 2020, it still holds 5 stars.

FP Foresight Global Real Infrastructure

This infrastructure fund had a very positive 2020 where it ranked in the fourth percentile with a return of 27.90%. Unfortunately, 2021 has been less kind, and the FundRock vehicle dropped to the 96th percentile with a negative return of 3.46%. Moreover, the fund is only a year old, so while it outpaced its rivals last year, any conclusions are yet to be drawn.

The young fund also has a relatively inexperienced management: the longest-tenured manager Nick Scullion has three years of portfolio experience. Compared to its peers, the portfolio is overexposed to real estate and utilities, and underweight in industrials and energy. Some 50% of the fund’s assets is also held in the top 10 of its 50 assets, which includes Easterly Government Properties, Brookfield Infrastructure and Infratil. In aggregate, Morningstar’s analysis has found that the team falls short and will struggle to outperform.

Baillie Gifford British Smaller Companies

The last fund to go from hero to zero is Baillie Gifford’s small-cap equity fund. Investing mainly in growth stocks, the fund went from a 32% return last year to a more moderate 8.33% year to date – equalling a drop from the fourth percentile to the 99th. Despite this, the fund has returned 9.81% over the past three years, holds a MQR Rating of Silver and 2 stars.

The Qualitative Morningstar analysis has found that the fund has a philosophy which is overweight in quality exposure and underweight in yield stocks compared to its category peers. It also has a preference for defensive stocks, meaning they are consistently profitable with solid balance sheets. Its main categories are healthcare and communication services, and holds YouGov (YOU), Genus (GNS) and Boohoo (BOO).