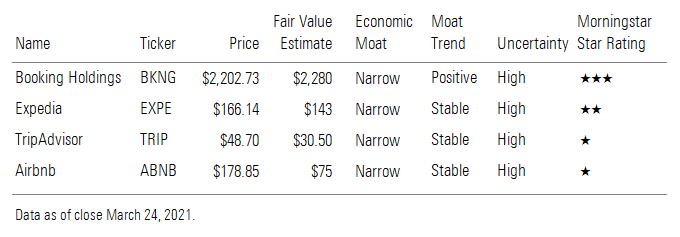

The time has passed when the four major online travel companies - Booking (BKNG), Airbnb (ABNB), Expedia (EXPE) and TripAdvisor (TRIP) - were undervalued on the stock market. While travel is still banned in most countries, the companies have managed to rebound since the share prices of the four stocks plunged a year ago due to the Covid-19 pandemic. Three of the Big Four are now overvalued, according to Morningstar analysts, despite the fact it is likely to take three or four years for travel demand to fully recover.

Does this mean that investors should sell out of the online booking agent sector? Morningstar analyst Dan Wasiolek says the Covid-19 crisis is an opportunity for these companies to strengthen their market position and, therefore, their value. The so-called network effect is key to a competitive advantage in this sector says Wasiolek. Here we look at the outlook for the industry.

Five Key Factors

To determine the strongest players in the online booking market, there are five key factors to consider: the structural influence of the pandemic on the demand for the provider's services; the player's position in the alternative accommodation market (i.e. everything outside of traditional hotels); its offer in the so-called “experience" market compared to his competitors; the benefit from traditional hotels; and the extent to which its business is threatened by tech companies such as Google (GOOG), Amazon (AMZN) and Facebook (FB).

Based on these five factors, Amsterdam-based Booking.com has the strongest network benefits – simply because it has the most complete offering for the traveller. That is, both traditional hotels and alternative accommodation. The same applies to Expedia, but not to Airbnb, whose offer is, of course, does not include traditional hotels. Finally, TripAdvisor is under serious pressure due to competition from Google, as well as a rising threat from Amazon and Facebook.

All four (Booking, Airbnb, TripAdvisor and Expedia), however, have at least 10 golden years ahead of them driven by the highly effective virtuous circle from which all four online providers benefit: their customers post positive messages on their network about transport, accommodation and their personal experiences on location, which attracts more other travellers, thus leading to greater demand. That is the network effect in action and partly why Morningstar assigns all four a Narrow Moat status, indicating limited competitive advantages.

That effect can become even stronger if the demand for travel recovers. For smaller competitors, it's getting harder and harder to compete against this. After all, it requires capital to be able to invest in, for example, the IT and 24/7 customer service needed to retain your customers and attract new ones. Especially after the difficult past year with all Covid restrictions and lockdowns, many smaller players in the travel world will have little financial leeway. The Big Four can benefit from this if they continue to develop their network, improving the user experience and increasing conversion.

Who are the Winners?

Alternative Accommodation

The strongest party in the field of alternative accommodation is Airbnb followed by Booking.com. Morningstar expects this part of the travel market to continue to grow rapidly; until the pandemic broke out, there was an increase in bookings of 20 to 30% a year. This will continue, despite the headwinds.

Sightseeing and Experiences

Experiences give a big boost to a player's network effect and this market is worth a whopping $171 billion per year. TripAdvisor is the market leader here, but booking, Airbnb and Expedia are increasingly gaining on it. It helps that there was still so much ground to be gained online; in 2019, only 20 to 30% of all experience outings were booked online, compared to around 45% for online travel.

Morningstar expects that by 2025, up to 40% of experiences will be booked online with one of the Big Four, at the expense of smaller providers. Market leader TripAdvisor along with Booking.com will benefit most from this development, says Wasiolek. The former strengthened its position as early as 2014 with the acquisition of Viator.

Traditional Hotels

Booking is the market leader in traditional hotels, followed by Expedia and TripAdvisor. But a strong presence in this market segment does not necessarily earn a stock an economic moat. That's because of the sheer size of the traditional hotel industry, with the number of bookings accounting for $548 billion a year. Compare that to the %144 billion that goes into the alternative accommodation, or the %171 billion spent on sightseeing and experiences.

Interestingly, the popularity of alternative accommodation does not seem to have affected the demand online for 'regular' hotels at all, which is still growing albeit at a slower pace than the more immature alternative accommodation market.

The Tech Threat

The biggest danger to these businesses comes from tech platforms such as Google, Amazon and Facebook. The biggest threat of the three is Google, because of its dominant position, with the ubiquitous use of Gmail, Google Maps, or a simple Google search for accommodation. Google’s acquisition of flight information software company ITA in 2010 has only solidified its position.

Still, analyst Wasiolek sees Google as a "manageable risk," including the impact of government regulation. Google's strength as an online search engine lies not in carefully developing a relationship with the customer, or as a service provider. Within the travel industry, the company focuses more on paid advertising on its site.

.jpg)