Valentine’s Day is the day to celebrate love, but what about the unloved? Much like finding a perfect partner, there are hidden gems are everywhere in the investment world. We look at funds which have been unloved for s you just need to know where to look.

On the surface, “unloved” funds may seem to be unloved for a reason: a period of underperformance, an out-of-favour investment strategy, challenges to the broader sector, or more appealing options elsewhere. But taking a contrarian approach to fund selection can also yield results.

Fund flow patterns over the past 26 years tell us that investors tend to buy funds that have performed well recently and sell what hasn't. This strategy can become self-reinforcing as strong inflows drive up stock prices, attracting more return-chasing investors, bidding up prices further still.

And just as inflows beget more inflows, outflows beget more outflows. Eventually, popular stocks become too expensive and unpopular ones too cheap, and the process reverses itself.

Investors who target the least popular areas of the market benefit when sentiment turns. Of course, outflows don’t make funds themselves any cheaper, but they might indicate which market sectors are unpopular and ready to recover.

Why You Should Buy the Unloved

For the past 25 years, Morningstar has been testing the results for buying unloved funds, through its "Buy the Unloved" strategy. The approach points investors to cheap or out-of-favour parts of the market that may be due for a rebound, using fund flows as a guide.

This involves investing equal sums in one fund from each of the three long-only equity Morningstar Categories with the largest calendar-year outflows, while avoiding those with the heaviest inflows. After three years, sell the stakes and invest the proceeds equally in that year’s unloved categories. The strategy is best suited for the periphery of your portfolio.

The results from the initial sample of US funds has been stark: the unloved portfolio has beaten the loved one (made up of the 3 most “loved” categories in terms of inflows) by a wide margin.

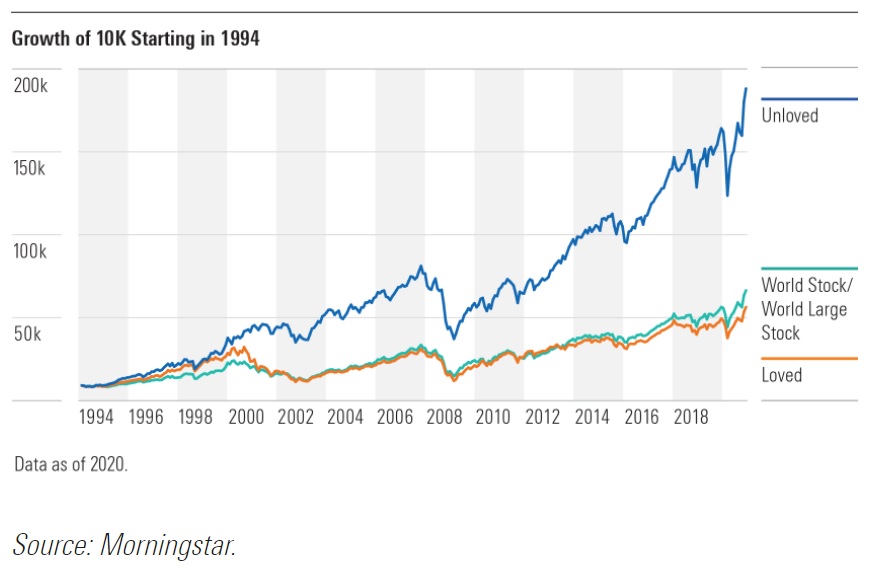

As showed in the chart below, $10,000 invested on January 1, 1994 in the “unloved” portfolio would have grown to $183,155 by December 31, 2020. The same amount invested in the “loved” portfolio would have grown to just $57,708 - considerably less than the $67,710 that an investment in the MSCI ACWI Index would have returned over the same period.

The Most Unloved Funds in Europe

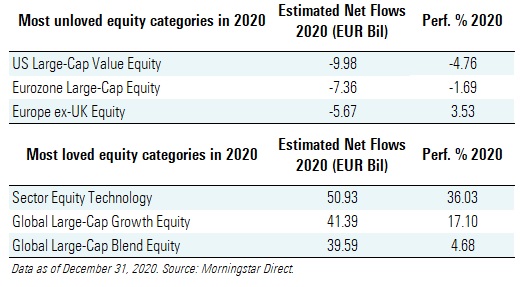

In looking to apply this to the European funds market, US Large-Cap Value Equity, Eurozone Large-Cap Equity, and Europe ex-UK Equity were the most unloved Morningstar equity categories in Europe last year.

Despite this, a number of funds could return to favour if markets are favourable to their categories. Here are some funds in unloved areas, which could prove a perfect portfolio match:

Gold-rated JPMorgan US Value

JPM US Value has a long-tenured lead manager and proven process. The fund’s management changed hands in June 2019 when Jonathan Simon stepped down from managing this offshore version of the strategy. But Morningstar analysts hold new manager Clare Hart in high regard, and rate her long tenure and strong supporting resources.

This portfolio generally sits at the border of the value and blend areas of the Morningstar Style Box. The tilt toward quality is evident in the proportion of holdings with a wide or narrow Morningstar Economic Moat Rating.

Silver-rated Robeco BP US Large Cap Equities

Boston Partners veteran Joshua White has joined Robeco BP US Large Cap Equities' now five-person team. Centred on companies with an attractive relative valuation, positive momentum, and sound business fundamentals, the process begins with the firm's quantitative analyst team ranking the constituents of the Russell 1000 Index and ADRs based on a 13-factor model.

Managers are more benchmark-aware than some and overweight each individual position the fund shares with the Russell 1000 Value Index. Overall, the fund can lag in junk-led rallies, and can also stumble during short-term drops, but actions taken during those volatile periods have typically set the fund up for success.

Gold-rated iShares Core MSCI EMU UCITS ETF

Morningstar Analysts believe iShares Core MSCI EMU ETF is one of the standout options for investors seeking exposure to eurozone large-cap equities, and think it will comfortably outperform its peers over a full market cycle. This is one of the cheapest and most representative index funds in a category in which passive funds have performed well.

The ETF offers broad and representative cap-weighted exposure to eurozone large-cap equities. With around 240 constituents, including a number of mid- and small caps, the MSCI EMU Index stands as a much better proposition for buy-and-hold investors than the more popular but mega-cap-heavy Euro Stoxx 50 Index.The fund has an ongoing charge of 0.12% and has comfortably outperformed its average category peer over three, five, and 10 years.

Gold-rated Uni-Global-Equities Eurozone

Uni-Global Equities Eurozone is a strong core holding thanks to its experienced and committed team and robust low-risk approach. The strategy is focused on reducing risks in a disciplined and replicable manner, firstly filtering the Euro Stoxx Index constituents based on liquidity and financial health and then removing stocks undergoing mergers and acquisitions, fraud charges, or similar material events. As a result, only 30%-50% of the investment universe is retained.

The fund was launched in 2016 but the much longer track record of the Uni-Global Equities Europe fund is a good indicator of what investors should expect. From inception in June 2004 until the end of January 2020, the fund’s RA share class has produced an annualszed return of 8.7%, beating the category average and the MSCI Europe Index.

Gold-rated Comgest Growth Europe ex-UK

Comgest Growth Europe ex UK’s strong and cohesive team and its time-tested growth strategy make it an outstanding choice for investors. The team seeks quality companies capable of growing their earnings independently of the economic cycle. These companies tend to be dominant players, well-managed and financially healthy.

Stocks belonging to the most-cyclical sectors, including financials and energy, are deliberately excluded and the team favours sectors such as consumer, technology, or healthcare in which companies can more easily build a strong competitive advantage and offer durable growth.

The strategy fund is not designed to outperform in all market environments though, and can look dull over the short and medium-term, particularly when markets are favouring lower-quality stocks.

Silver-rated Janus Henderson Continental European

The Janus Henderson Continental European fund combines macro and micro research to be robust and disciplined. Ideas are generated primarily through a combination of screens and fundamental stock research undertaken by John Bennett and his team. The manager pays little heed to the benchmark when constructing the relatively concentrated portfolio of 40-50 names. Country and sector limits are absolute (40% and 30%, respectively), which allows a fair amount of flexibility.

John Bennett has created a solid track record on this strategy and the H EUR Acc share class outperformed MSCI Europe ex UK Index category benchmark and the category average from February 2010 to end-December 2019. Despite a challenging 2016 and 2017, it has never underperformed either benchmark on a rolling five-year basis during his tenure.