Is there still room for a year-end rally in the markets? A year-end rally is defined as a rise in stocks prices that sometimes occurs on the trading days between Christmas and New Year’s Day.

The phenomenon is thought to occur in anticipation of the January effect (a rise in demand for stocks resulting from the increased liquidity among investors who closed positions prior to the end of the year for tax purposes). But it may be triggered by several factors including optimism about the new year ahead and the fact that trades are occurring at this time of year, meaning the ones that do have a greater impact on market moves.

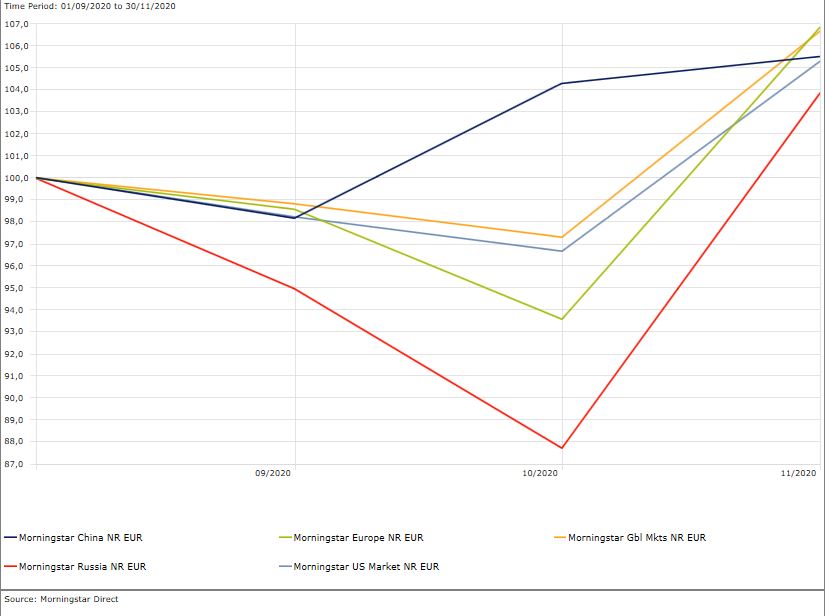

This year, the rally seems to have started early. Over the three months to November 30, 2020 the Morningstar Global Market Index gained 6.7% in euro terms, while the US market climbed 5.33%, Europe 6.7% and China 5.5%.

Has the Rally Already Begun?

One segment usually worth watching at this time of year is the consumer goods sector, which often gets a boost from Christmas shopping and the subsequent sales. Historically, strong equity markets have correlated with increased spending on high-end goods and luxury brands as wealthy investors are more willing to splurge on big ticket items in the festive season.

“A significant amount of spending during this year’s festive season will shift away from holiday travel costs and move toward consumer goods”, says Dave Sekera, Chief US market strategist for Morningstar. “We expect that people will focus their spending on buying items that support the pandemic-driven stay-at-home lifestyle”.

Could Healthcare Lead the Charge?

One sector that has been firmly in the spotlight since the outbreak of the Covid-19 pandemic is healthcare, and this scrutiny has only intensified since the announcement of the discovery of some vaccines shown to be effective in fighting the virus.

But investors hoping that could spark a market rally may be misguided. “The vaccine should engender strong goodwill for the companies, but because of the likely heavy competition, we view it as only moderately helpful for valuation”, says Damien Conover, director of healthcare equity research and equity strategy for Morningstar. With strong competitors like Moderna, Johnson & Johnson, AstraZeneca, Sanofi, GlaxoSmithKline, and many more, he expects the pricing power of the vaccines to be low, especially because several companies are receiving government funding and have a stated commitment to low pricing. Conover adds: “However, we expect the quick development of vaccines to enable the biopharma industry to gain goodwill with governments and help in discussions around any drug pricing reforms.”

Big Returns for Small Caps

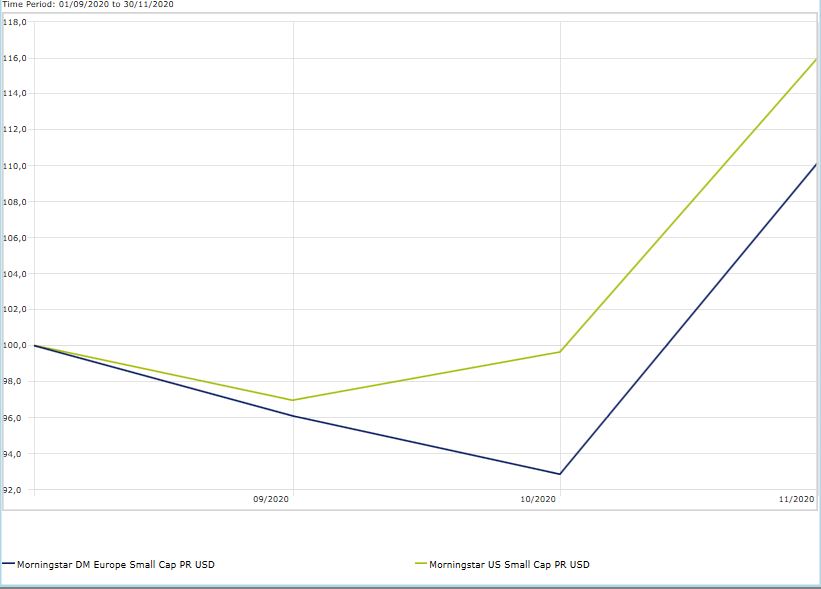

Looking further down the market cap spectrum to smaller companies might be one tactic investors hoping for a flurry of growth might adopt. Here, too, the rally seems to have already begun. The Morningstar Europe Small Cap index, for example, gained 1.4% over the past three months while the US Small Cap basket gained 16.3%.

Will it last? There are intuitive several factors that usually justify a small-cap premium. Fewer analysts cover small-cap stocks. A lack of coverage could lead to informational barriers that may result in mispricing. Moreover, small-cap stocks are less liquid and thus more costly to trade. Scant liquidity could further justify why investors should-in theory-be rewarded for the risks associated with illiquidity.

But there is also another element to consider. Studies have in the past have shown that half of the excess returns of small-cap stocks often comes during the month of January and that half of the January returns were concentrated in the first five trading days of the new year.

This is called the January effect. “This January effect has defied attempts at any rational, risk-based explanation”, says Ben Johnson, Director of global exchange-traded fund research for Morningstar. “Furthermore, this effect has diminished with time. Its dependence on a seasonal peculiarity that has weakened through the years is example of the size effect's shaky footing”.