There has only been one story for investors so far in 2020: growth. As tech companies have led the charge in the stock market's recovery from the Covid-19 sell-off, the difference in performance between growth and value funds has been stark to say the least.

This is all too clear when we look at the Morningstar Style Box - a simple chart which indicates a fund's investment biases. Year to date, the performance gap between the average large-cap growth fund and its large-cap value counterpart is a staggering 25 percentage points.

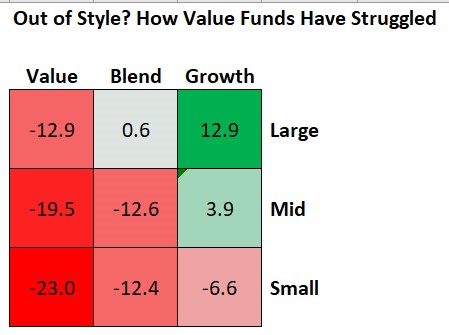

We have examined 1,237 UK-domiciled funds to determine which styles are outperforming.

The gap between funds focused on smaller companies and those investing in large-cap is clear to see. Large-cap funds have outperformed across the board. Undoubtedly, it has been a stellar year for large-cap companies with a growth bias. These businesses often belong to the healthcare and tech sector, which have both benefitted hugely from the coronavirus pandemic and the trends that have emerged in its wake.

“It’s fair to say 2020 has been a bruising year for value investors, especially following a five-year period which could hardly be described as vintage for the style,” says Nick Kirrage, manager of Bronze-Rated Schroder Income. He is acutely aware of the headwinds many value-type businesses face, whether that be structural challenges such as the rise of e-commence over bricks and mortar stores, or the shift from fossil fuels to renewable energy.

The coronavirus sell-off saw cheaper pockets of the market feeling the most pain – namely airlines, banks and autos. Oil and gas companies were also hit, both from the oil price shock in February and then the slowdown in global demand due to the impact of the virus on how we live.

Will the Bubble Burst?

Kirrage believes the only comparable reference point for today's valuation gap between growth and value stocks is the dotcom bubble in the early 2000s.

While the run-up to the bursting of that tech bubble saw growth outperform value, Kirrage says there was a dramatic reversal soon after. “Markets punished stocks priced for perfection and value went on to have its time in the sun,” he says. “Anyone with a concentrated portfolio of growth equities back then would have felt significant pain. The question clients should be asking themselves today is: is this time really that different?”

It's a view shared by Mark Niznick, manager of the Silver-Rated Artemis UK Smaller Companies. “As investors clamour to seek refuge, the elastic of normal valuations has been stretched to extreme levels,” he says. “Investors are fearful of the risk of a second wave and prefer to weather the storm by sticking with companies whose businesses they perceive to be least affected.”

Of course, these reminiscences don't make it any easier to be a value investor in the current market. For now, Kirrage is focusing on companies whose balances sheets are strong enough to weather the forthcoming storm.

Niznick has taken advantage of current low valuations to add to his positions in certain stocks; he expects to benefit when the tide turns. “This pandemic is a severe but temporary issue,” he says. “We do not know if there will be a second or even third wave, but on our usual three-to-five year time horizon we are working on the assumption that the economy can largely return to pre-pandemic levels.”

His fund, which favours more defensive stocks, has underperformed this year, down a hefty 31% year to date compared to an average loss of 20.5% in the UK Small-Cap Equity category. The biggest detractors to performance in the fund this year have been Mears (MER), RPS (RPS) and National Express (NEX). Mears provides local councils and housing associations with day-to-day housing maintenance (such as fixing taps, boilers, windows) under long term contracts. “Normally this would be highly defensive in a recession, but their engineers have been unable to get into tenants houses during lockdown so revenues have been hit,” explains Niznick.

Menawhile, RPS is a global consultancy but many of its staff have been unable to travel to customers sites during the crisis, and National Express derives the majority of its profits from operating school buses in the United States. “Again, this is usually defensive, but with US schools shut, it has also been badly affected,” says Niznick.

While value investors have endured a difficult year, the recent sell-off in tech stocks has perhaps provided a glimmer of hope that the style could yet make a comeback. Kirrage says: “The history of the stock market offers evidence of a long history of humans getting overly optimistic in the good times and overly pessimistic in the bad. Our job, however psychologically uncomfortable, is to exploit that. We try to make good money from bad headlines."

.jpg)