“The biggest mistake I've made” is how Alexander Darwall, manager of the European Opportunities Trust (JEO), described his decision to invest in German payments provider Wirecard (WDI) as he offloaded his stake in the business last week.

Until last week Darwall, who left boutique fund group Jupiter last year to set up his own investment firm, had more than 10% of the EOT portfolio invested in the German company – equivalent to around £80 million. A stock market announcement on Thursday confirmed the manager had sold all of his shares in the business.

Wirecard is currently embroiled in a scandal, as it emerged that £1.7 billion listed in its accounts may not actually exist. Shares in the company plunged 60% in a single day on the news.

The effect of this on a portfolio with such a large stake in the company, such as Darwall’s, is huge. Morningstar data on June 18, as the stock went into freefall, showed the trust – which is listed on the FTSE 250 – was down more than 11.5%.

A Concentrated Approach

Many investors purposely seek out managers with a high-conviction approach, taking big bets on the businesses they believe will thrive over the long-term. Such managers are often notorious for having incredibly concentrated portfolios.

But when these managers get it wrong, the ramifications on returns can be significant. It begs the question: should fund managers be betting big?

Jon Miller, head of manager research at Morningstar, says: “Managers with concentrated portfolios are by nature making key stock specific calls. Clearly, they’ll be doing something different than the index, meaning the potential upside and downside versus the market can be pronounced.”

A number of fund managers are noted for their bold calls on the companies in which they invest. One such manager is Nick Train, manager of the Silver-rated Finsbury Growth & Income Trust (FGT). The £1.8 billion trust has some 12% of its assets in London Stock Exchange Group (LSE), 10.8% in RELX (REL) and 9.7% in Unilever (ULVR). According to Morningstar data, the top 10 holdings in the trust account for more than 80% of its total assets.

For investors, such a setup plays out incredibly well while a manager is making the right calls. LSE’s share price has more than tripled from £24.52 to £82.32 over the past five years, for example. The Finsbury Growth & Income Trust has delivered whopping annualised returns of 14.56% over the past decade.

Open-ended funds are subject to different rule than investment trusts and are only allowed a maximum of 10% of their assets in any single stock. But many still take a concentrated approach. The Gold-rated Morgan Stanley US Advantage fund, for example, has 7.57% of assets in Shopify (SHOP), 6.75% in Amazon (AMZN) and 6.31% in ServiceNow (NOW). The fund is up an incredible 38% year to date and has achieved annualised returns of 24.39% over three years.

The Danger of Getting it Wrong

But when fund managers make a wrong call, these stellar returns can collapse. Darwall has managed the European Opportunities Trust (formerly the Jupiter European Opportunities Trust) since 2000. Over 10 years, it has delivered annualised returns of 14.22% - more than double its benchmark - and over three months it is up 25.44%.

Darwall first invested in Wirecard 13 years ago, when shares were around €9, increasing his stake over time, and started to reduce his position in November 2017, when shares hit €121.

But concerns about Wirecard have been circling for some time, with persistent suggestions that some of the company’s reported revenues and profits were not reliable. While Darwall reduced his holding in the firm from around 15% of assets to 10%, he continued to stick with the stock. Morningstar Direct data shows that as of June 18, the trust was the seventh largest owner of the business, with a 0.93% stake.

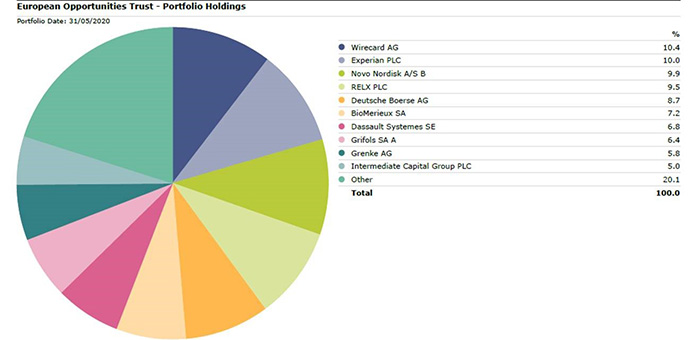

It is not the only big bet in the portfolio. The trust’s top 10 holdings account for almost 80% of assets including 10% in Experian (EXPN), 9.9% in Novo Nordisk (NOVO B) and 9.5% in RELX.

Morningstar analysts downgraded the European Opportunities Trust from a Gold to Silver rating in November 2019. Miller says: “In terms of risk within the portfolio and relating to Wirecard itself, we reflected our view at the last review by downgrading the ‘Process’ pillar from High to Above Average. The move from a Gold to Silver rating was also partly driven by Darwall’s move from Jupiter to running his own firm.”

Certainly, the situation raises again the question of whether fund managers who set up their own investment firms can replicate the robust checks and balances that are in place at the investment giants where they have cut their teeth. It’s an issue which was cast into the spotlight with last year’s Woodford Equity Income collapse, when many questioned whether the fund would have been able to get into such a situation had the manager still had to hand the oversight of his previous firm Invesco.

Ben Yearsley, director at Shore Financial Planning, says: “Fund managers having large positions in their portfolio isn’t an issue as long as they’re clear that that is their style. Many of the best-performing funds have a concentrated portfolio and, unfortunately, occasionally they get something wrong, as in this case. Short-term, that clearly dents performance, but the key is getting it right more than wrong over the longer-term.”

Devon Equity Management did not comment.