Earlier in the week we looked at five FTSE 100 companies that had fallen into five-star territory, which means they are the most undervalued of the stocks Morningstar analysts cover.

Now we cast the net wider to look at European companies that have been caught up in the global sell-off but still have an “economic moat”, or significant competitive advantage. They come from a wide range of industries, from banking to jewellery, and countries including Denmark, Switzerland and Ireland.

While these are highly uncertain times for consumers and investors, the current market turmoil has hit valuations for companies we think could stay the course:

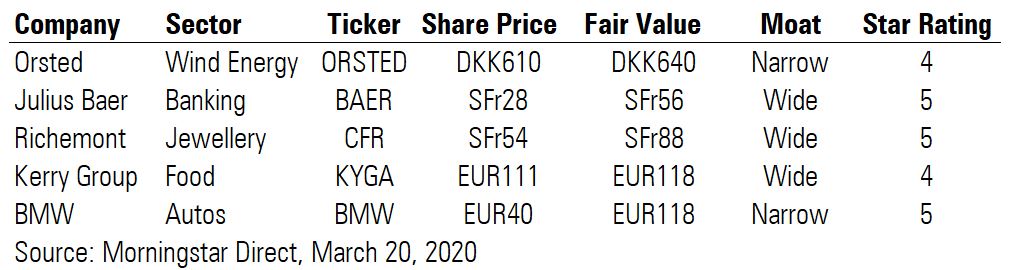

Five Companies to Weather the Storm

Orsted (ORSTED) – 4 Stars – Narrow Moat

Danish wind farm and energy trading company Orsted is trading at 610 Danish krone, below its fair value of DKK640, according to analyst Tancrede Fulop. One of the key criteria for Morningstar analysts is strong company leadership, and on this score, Orsted is “exemplary”. Fulop says the company is a “the undisputed global leader” in wind energy, a market which is expected to increase fifteen-fold to 2040, according to the International Energy Agency.

One great feature of the company, Fulop argues, is that it has gone into this crisis with low debt. He expects the coronavirus outbreak to delay the commissioning of new wind farms, but the upside is that Orsted’s competitors – oil giants that have moved into renewable energy – have a serious cash flow problem at the moment, which will weaken them in the near term. The company has a “unique combination of high earnings growth, sustainable returns, and a low carbon footprint”, Fulop says.

Julius Baer (BAER) – 5 Stars - Wide Moat

Analyst Johann Scholtz thinks Swiss banking firm Julius Baer is less exposed to the financial fallout from coronavirus because it has limited lending and “excellent liquidity”.

“If you look through the downturn, this is a great time to pick up Julius Baer,” he argues, noting that in the 2008 crisis, clients sought out the bank as a safe haven as clients switched away from Swiss banking giants UBS and Credit Suisse.

And longer-term, the trend for wealthy individuals seeking investment advice is in the firm’s favour. “The demand for bespoke financial planning and wealth management services will continue to be strong,” he notes.

Julius Baer is a prized firm from Morningstar’s point of view because it is rated as five stars, meaning it is significantly undervalued, and has a wide economic moat. Just two FTSE 100 firms under Morningstar coverage have a five star rating and wide moat, and they are both tobacco companies.

Richemont (CFR) - 5 Stars - Wide Moat

Luxury stocks have been in the eye of the storm in this crisis for many reasons: their exposure to China, the fear that an economic crisis will crimp disposable income and the drop in demand as people stop going to shopping centres.

But Cartier-owner Richemont is well placed to survive the current malaise, says Morningstar luxury analyst Jelena Sokolova, who thinks the company is highly undervalued and holds significant advantages over rivals.

“Richemont has one of the strongest brands in the industry with high barriers to entry and good growth prospects,” says Sokolova. “Most of the group’s brands are at least a century old, have iconic collections lasting 40 to 80 years, and have historically commanded significant pricing power."

There are very few recession-proof consumer companies but the argument is that people who can afford watches worth £5,000 or more are less exposed to a downturn than most. Demand for luxury goods held up during the last recession, for example, especially as affluent investors put their money into tangible assets such as watches and jewellery rather the stock market.

Sokolova praises Richemont’s strong cash position and 4%-plus dividend yield. The company is trading just below SFr50, against a fair value of SFr88.

Kerry Group (KYGA) – 4 Stars - Wide Moat

Kerry Group is “one of the best-positioned ingredient suppliers in the fragmented food ingredient industry”, says Morningstar analyst Ioannis Pontikis. Like Orsted, analysts rate the company’s stewardship of investor capital as “exemplary”.

The group has strong growth prospects due to its dominant position in emerging markets and Pontikis forecasts annual profit growth of 10% over the next two years, despite the current crisis. Its competitive advantage stems from partnerships with loyal customers and from the strength of its well-known brands such as Wall's sausages and Dairygold butter.

Headquarted in Ireland and listed on the London Stock Exchange, the company is a much sought after "10-bagger" in that its share price has gone from €10 to €100 in around 20 years.

Shares have been turbulent in the recent sell-off but have held up reasonably well over six months, remaining above €100. The food industry isn't a cyclical one (people still need to eat, regardless of the economic environment) so the stock has defensive qualities in current market conditions. Analysts also think its ingredient division will benefit from the "wellness" trend as consumers increasingly demand to know what goes into their food.

BMW (BMW) - 5 Stars - Narrow Moat

The share price of German automotive giant BMW has been caught up in the market sell-off – in the year to date the price is off 45% from €73 to €40. This has pushed the stock, which according to analysts has a narrow moat, into five-star territory. The logic is hard to argue with at this point: a Europe-wide recession could crush demand for high-end cars and put the region’s already stretched automotive industry under severe pressure.

BMW has just reported results for 2019 which were solid, but it is understandably cautious about making 2020 forecasts. Autos analyst Richard Hilgert is more optimistic looking beyond this year: “While we would be hesitant to catch a falling knife, at some point, for long term investors, we view BMW’s reduced valuation from Covid-19 as an opportunity to own shares.”

He thinks the stock market is valuing BMW as if the company is in a permanent economic slump. While the firm has a “high” uncertainty rating, he maintains the €118 fair estimate for the shares for now – the 66% discount to fair value makes BMW one of the most undervalued stocks in Morningstar's European coverage.