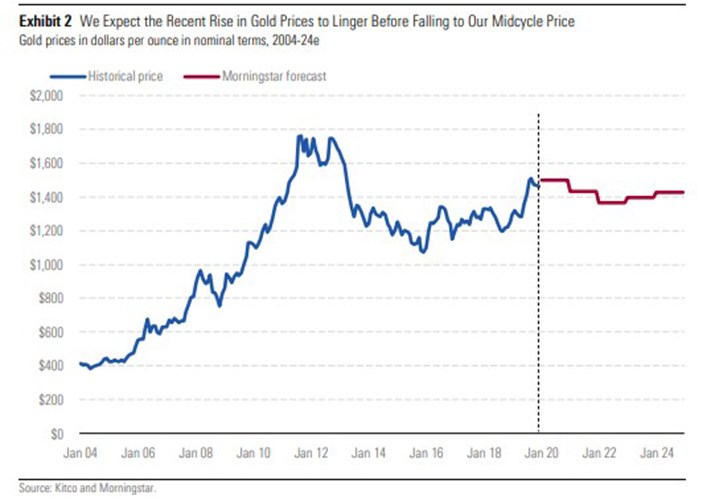

2019 saw a resurgence of demand for gold, and the price of the precious metal climbed nearly 20% in the third quarter of the year to about $1,550 per ounce. But will the upward trajectory continue, or will gold lose its lustre? Here we look at the outlook for the yellow metal in 5 charts.

Why Investors are Rushing to Gold

With the Federal Reserve cutting rates three times in the 2019, gold’s investment case has strengthened. From June to September 2019, gold rapidly rose about $250 per ounce to roughly $1,550 per ounce.

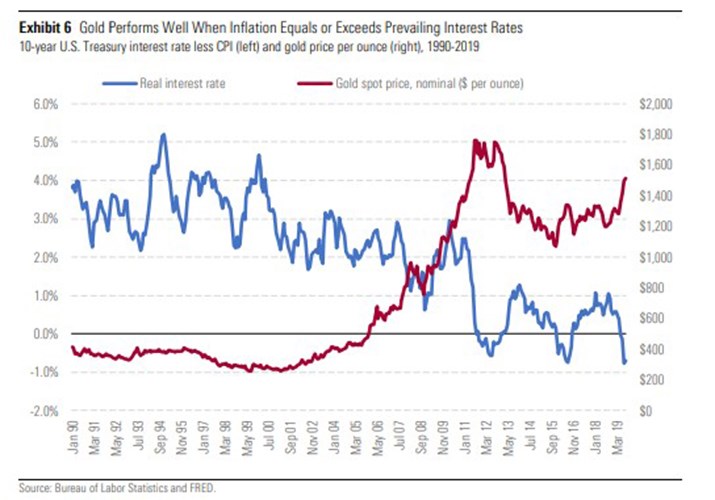

The chart below shows how the price of gold has moved with long-term real interest rates. When inflation equals or exceeds interest rates, gold's investment attractiveness increases. This is because gold is seen as a safe, physical store of value, protecting investors’ money in times of uncertainty. Conversely, when investors are more risk-on and interest rates are high, gold effectively loses money because it cannot pay an income or grow.

When interest rates were meaningfully high in the 1990s and early 2000s, gold didn’t carry the same relative attractiveness as an investment, leading to flat prices. However, when interest rates plummeted to zero and into negative territory during Global Financial Crisis and subsequent recovery, gold’s attractiveness as an investment, and thus the price, soared.

Gold is a Safe Haven

The effect of any surge in investment demand for gold is exacerbated by the slow-moving nature of gold supply – changing mine supply is like turning a tanker ship. New mines can take a decade or more from discovery to full production, and even short-term production increases from bringing back mothballed capacity or opening new mines can take years.

As a result, rapid spikes in demand can only truly be met by recycled demand, or the sale of existing gold by current owners. To encourage current holders to sell, higher prices are needed.

To understand the investment appeal, we look at gold's use as a safe-haven asset. A safe haven is an asset that holds, or even increases, its value during periods of uncertainty and in downturns. It should preserve capital, withstand market volatility, and provide diversification across a portfolio.

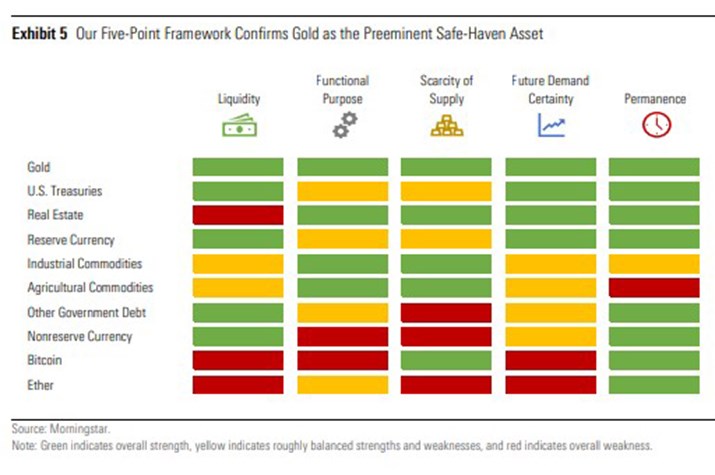

We use a five-point framework that defines the best safe-haven assets as very liquid, serving a functional purpose other than as a store of value, having scarcity of supply, having high certainty of future demand and having long-lasting permanence.

Here we can see how gold compares to other assets. Based on this framework, gold is the pre-eminent safe haven investment asset, with the only real competitor US Treasuries.

During periods of economic turbulence, then, investors will choose between gold and Treasuries. Understanding which one is more favourable falls to the inherent differences between commodities and bonds.

On one hand, gold is just a shiny piece of metal, but it's rare. Scarcity means its value tends to rise with inflation. During periods of high inflation, the value of cash tends to decline but gold maintains its value in real terms, leading to higher prices. However, it offers no other potential return or payment because it's ultimately just a rock.

On the other hand, bonds can generate returns through coupons, but they're not very scarce. Although a Treasury offers interest returns, it will typically lose value to inflation since terms are agreed upon when the bond is issued and last until maturity. As a result, gold is generally more favourable than a Treasuries in times of negative real interest rates or when inflation exceeds interest rates.

What Drives Demand for Gold?

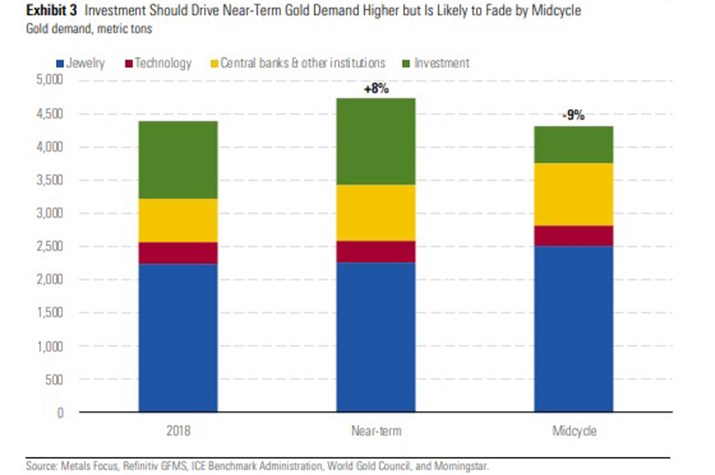

In the short term, investment demand is the main driver of gold demand. It is also the most volatile because most gold investors access the asset through ETFs which are easy to buy and sell. Buyers who go through the trouble of acquiring and keeping physical gold tend to hold for the long-term.

However, as an individual category, jewellery is the single largest source of gold demand, typically accounting for 45% to 60% of total demand in any given year. From 2010 to 2018, it’s the only category, other than central bank purchases, that’s grown. Most gold jewellery purchases come from just two countries: China and India. While constituting less than 40% of the world's population and roughly 16% of the world's GDP, these two countries account for roughly 60% of annual jewellery demand.

Technology is both the smallest and fastest-declining category. Gold is used in a range of applications including electronics and dentistry, but its high cost has seen it substituted in many cases. Use in dentistry fell almost 13% a year between 2010 and 2018, for example, and electronics by 2.5% a year. This decline will likely continue as cheaper substitutes continue to take share.

Central banks tend to be the second smallest demand category after technology, generally representing 10% to 20% of total demand in any given year. Although the category has seen a resurgence in recent years, most purchases have come from just a few countries. Of the 10 countries with the largest gold reserves, only Russia, China, and India have been net purchasers in the last five years. Not all countries have been purchasers, either. From 2014 to 2019, Turkey reduced its gold reserves by 27% and Venezuela sold 56% of its gold reserves.

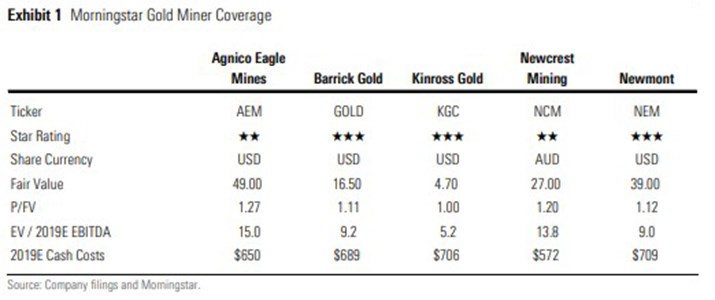

The Outlook for Miners

The current gold price is around 25% higher than Morningstar’s long-term forecast, and that means there are limited investment opportunities in the miners we cover.

Miners can create value, such as synergies from Barrick and Newmont's Nevada joint venture, improved performance from Newmont's legacy Goldcorp assets, continued cost improvement at Newcrest's Lihir mine, or the completion of new projects at Agnico Eagle and Kinross. However, our forecast for declining gold prices outshines any operational upside, leaving shares trading roughly in line with or slightly above our fair value estimates on a risk-adjusted basis.

There have been few major new mines opened in recent years and production has been relatively flat. The miners under our coverage could sustain current production levels for a decade or more, based on proven and probable reserves. Including the most recent measured and indicated resources that could be converted to reserves, production could be sustained beyond 20 years.

None of the miners Morningstar covers has an Economic Moat and all have a High or Very High Uncertainty Rating. And with today's gold price well above our midcycle forecast, it's no surprise that we see little opportunity among the gold miners. Despite opportunities for lower costs or more production at any individual miner, our forecast for a lower real gold price limits any risk-adjusted upside.

Where Will the Gold Price Go From Here?

We think 2020 gold demand will be 8% higher than it was in 2018, driven by stronger investment-related demand, mostly from ETFs and central banks. But investor sentiment can quickly change, and if we see demand for gold ETFs unwind this would weigh heavily on prices and we expect prices to fall to $1,250 by 2022.