What are an investor's odds of selecting an active Europe equity fund that is likely to outperform its benchmark after fees? Conversely, in which categories is it preferable to go passive?

We explored this question in our recent study, “Should You Go Active in European Equity?” which analysed the performance of funds across the 12 Europe-Equity Morningstar Categories that span the market-cap and style spectrum.

Our study followed a similar approach taken in a fixed-income funds study, “Finding Bond Funds That Can Beat Their Benchmarks After Fees,” in which data from 2002 to 2018 was used to compare funds’ performance against category benchmarks and passive options on a gross and net-of-fees basis. This approach was chosen because of the way historical returns help investors assess how much they should pay for active funds in a specific category without eroding chances of beating the benchmark. Here, we explore examples of what this research uncovered.

4 Things to Know About Europe Equity Funds

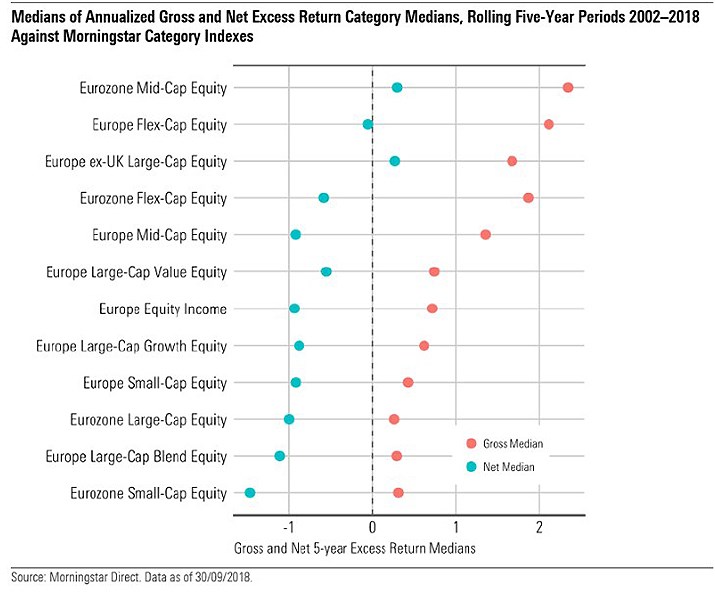

The median active manager outperforms the benchmark in all categories, before fees

Though there are large differences between categories, the median active manager can beat the benchmark in all categories before fees, as indicated by the red dots in the chart below. However, the margin of outperformance has not been sufficient to overcome fees, and all but two categories (Eurozone Mid-Cap and Europe ex-UK Large-Cap) have seen overall negative excess returns against the index.

High full-freight fees make it difficult for active managers to outperform

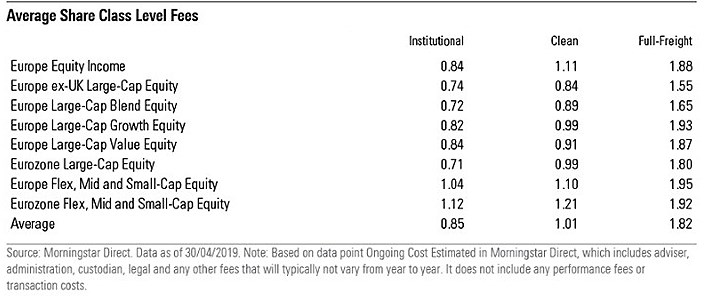

The chart below reflects full-freight fees, which are much higher than the fees associated with institutional share classes or "clean" retail share classes (which do not include distribution fees or commissions). Because of these substantial full retail fees, the hurdle for active managers to outperform the benchmark is high; consequently, investors who can access cheaper share classes have considerably higher odds of outperforming an index. In five out of 12 categories, the median fund has done well enough to overcome institutional or clean-share class fees, which are much lower than full-freight retail fees, as indicated in the table below.

Funds in the best quintile beat the category index in all 12 categories, even after retail-investor fees

These results show that skill in identifying above-average funds can reap particularly strong rewards for investors. The Flex-Cap, Mid-Cap, and Small-Cap categories provided the most lucrative fields for active managers. However, selecting funds that will maintain this level of outperformance in the long term is a challenging task, as the excess returns of the top performers can fluctuate heavily.

Fund mortality also weighs significantly on the odds of outperformance

In addition to fees, lineup churn is an important factor in Europe equity funds. On average, the survival rate of funds over the typical five-year period was 79% across all categories, but it sank as low as 61% in the Large-Cap Value category. Some categories’ long-run success ratio—which measures the percentage of funds that both survived and outperformed an index—is more than two times higher than others.

Overall, our research found that active management in Europe equity funds performed better than expected. However, providing access to competitively priced share classes will be essential to the continuation of this success. Even in categories that appear to be more lucrative for active managers, investors should not turn a blind eye to costs.

.jpg)