713 Funds Alter SFDR Status in Just Three Months

Hortense Bioy, CFA - 10 August, 2022 | 7:25PM

It's been more than 16 months since the EU introduced its Sustainable Finance Disclosure Regulation (SFDR), requiring asset-management companies to provide information about their investments' environmental, social, and governance (ESG) risks for the first time. They must also assess the impact on society and the planet.

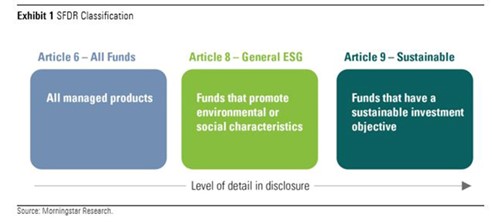

Since 10 March 2021, funds available for sale in the EU have been classified by their managers as Article 6, 8, or 9, depending on their sustainability objectives, as laid out below.

Light Green Flows Go Red, Dark Green Holds Up

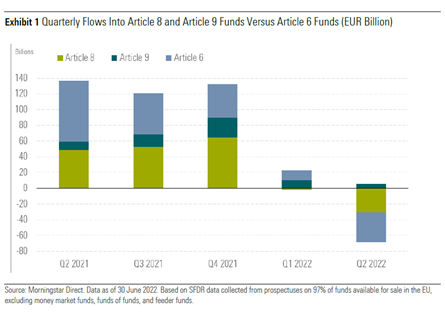

Amid investor concerns over a global recession, inflationary pressures and the conflict in Ukraine, light green (Article 8) funds bled EUR 30.3 billion in the second quarter after shedding a revised EUR 2.1 billion over the previous quarter. However, investors continued to pour money into dark green (Article 9) products, which registered EUR 5.9 billion in net inflows.

Meanwhile, in the second quarter, asset managers continued to upgrade funds by enhancing their ESG integration processes, adding binding ESG criteria to their investment objectives and investment policies, or in some cases completely changing the mandate of the strategy.

Over the last three months, 713 funds altered their SFDR status, including 696 that upgraded and 16 that downgraded. The vast majority (652) that upgraded their status moved from Article 6 to Article 8, while 17 funds upgraded from Article 6 to Article 9. Fund companies are clearly feeling the commercial pressure to have as many funds as possible meeting at least Article 8 requirements.

All 16 downgraded funds, including 10 NN Investment Partners and four PIMCO strategies, reclassified from Article 9 to Article 8. These reclassifications emerged as a result of a more cautious approach taken by the asset managers in light of recent regulatory clarifications.

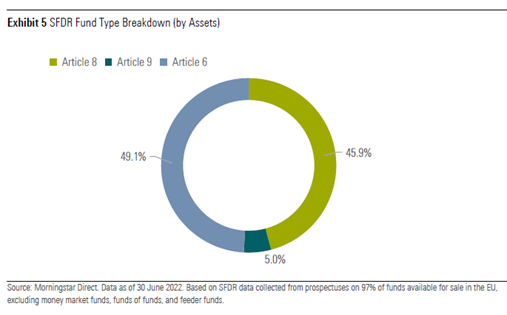

As a result of the large amount of upgrades as well as the new fund launches (183 in the second quarter), Articles 8 and 9 funds now account for more than half of overall EU fund assets, from just one third a year ago.

For example, NN noted that "new clarification offered by the European Commission and [Dutch regulator] AFM made clear that funds making Article 9 disclosures may only invest in sustainable investments based on the definition provided within SFDR.

“This additional clarification was not in place when NN IP initially implemented SFDR, which is why we are now intended to update the disclosures in line with evolving regulatory guidelines." NN added that the reclassification doesn't reflect any changes in the funds' investment process.

As regulators continue to provide further guidance on the implementation of SFDR, we can expect more funds to be reclassified to Article 8 in the future.

Active vs. Passive

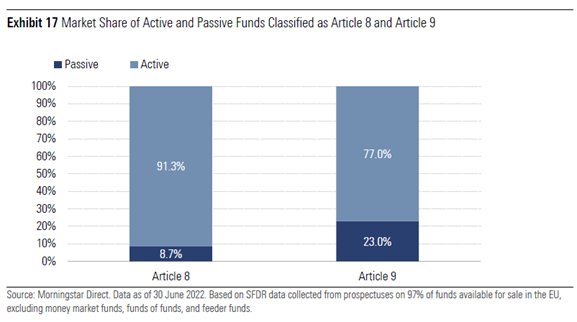

Active funds continue to dominate the SFDR Article 8 and Article 9 product landscape. However, passive funds are gaining ground in the Article 9 category, reaching 23% at the end of June from 17.4% six months ago.

The larger market share for passive Article 9 funds may appear counterintuitive, but it is partly due to the growing number of sizable index funds and exchange traded funds (ETFs) tracking EU climate benchmarks (Paris-aligned and climate transition benchmarks).

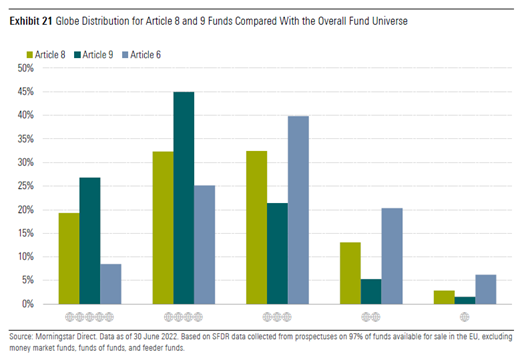

In aggregate, Article 8 and 9 funds perform better on ESG metrics than the rest of the universe. Almost three quarters of Article 9 funds carry Morningstar Sustainability Ratings of either 4 or 5 globes, compared with just over half of Article 8.

Article 9 funds also typically have lower involvement in controversial weapons, tobacco, fossil fuel, and severe controversies.

The majority of Article 8 and Article 9 funds also have zero exposure to controversial weapons, tobacco, thermal coal, and severe controversies. However, fewer than a quarter of Article 8 funds and Article 9 funds have no fossil fuel involvement. These numbers have remained stable over the past six months, despite the energy crisis and continued rally in oil and gas prices this year.

The relatively higher fossil fuel involvement of Article 9 funds, in particular, may still come as a surprise to some investors. But it is largely because many of these funds invest in so-called transitioning companies. These include oil and gas or utilities companies that are increasing their exposure to renewable energy but still operating their legacy fossil fuel businesses.

Similar to fossil fuels, it's a minority of Article 8 and Article 9 funds (46%) that have no nuclear involvement. In light of the inclusion of nuclear in the EU Taxonomy, we may see both types of funds increase their exposure to nuclear.

Hortense Bioy is global director of sustainability research at Morningstar.